May 1, 2022

by Stephen Stofka

On NBC News this week a reporter mentioned that a living wage was $35.80 an hour for someone with a child. M.I.T.’s Living Wage Calculator (2022) confirmed that approximate amount near where I live. That’s an annual income of $71,000, about $4,000 more than the median household income (MHI) today. In the past few decades incomes have been falling behind by just a little bit in inflation-adjusted income. In 1987, the MHI was $26,600, about $69,000 in today’s money (Series in footnotes). Today’s MHI is just a bit below off that figure. So what’s the problem?

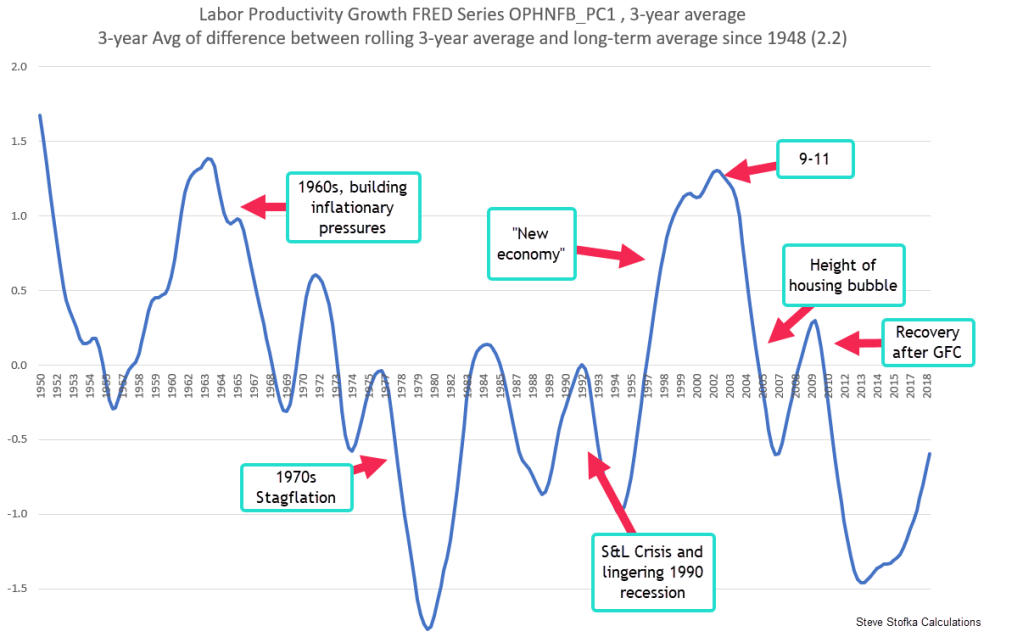

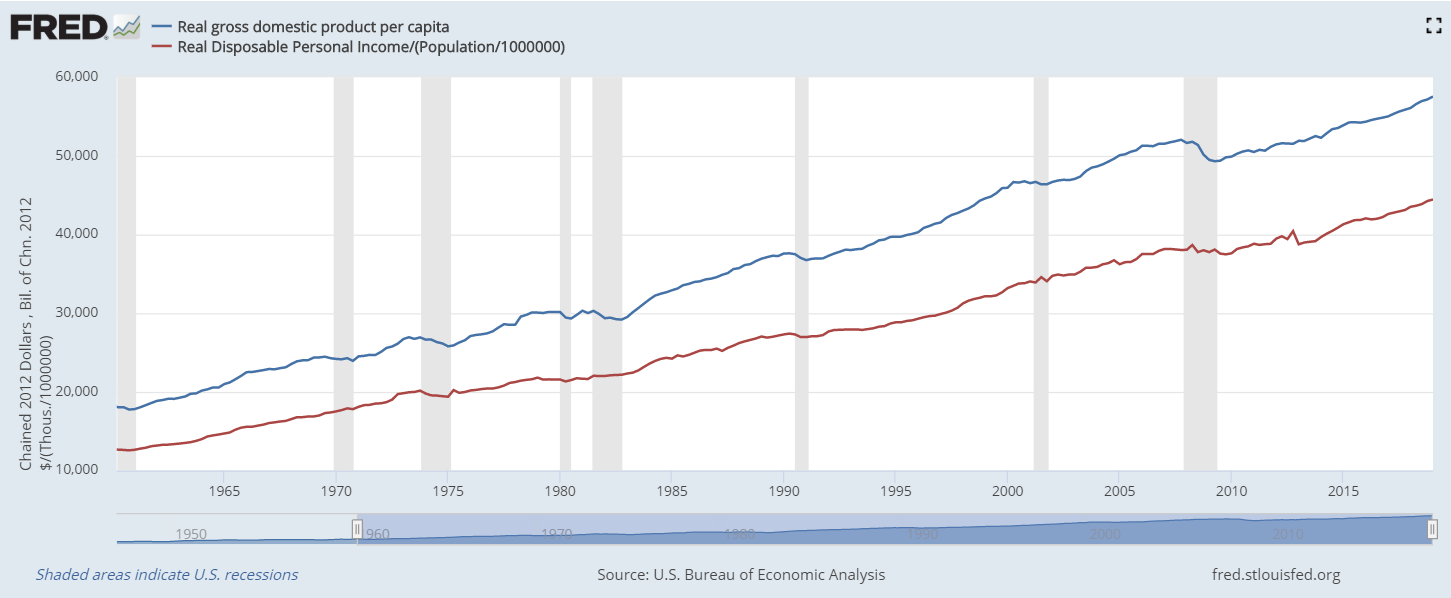

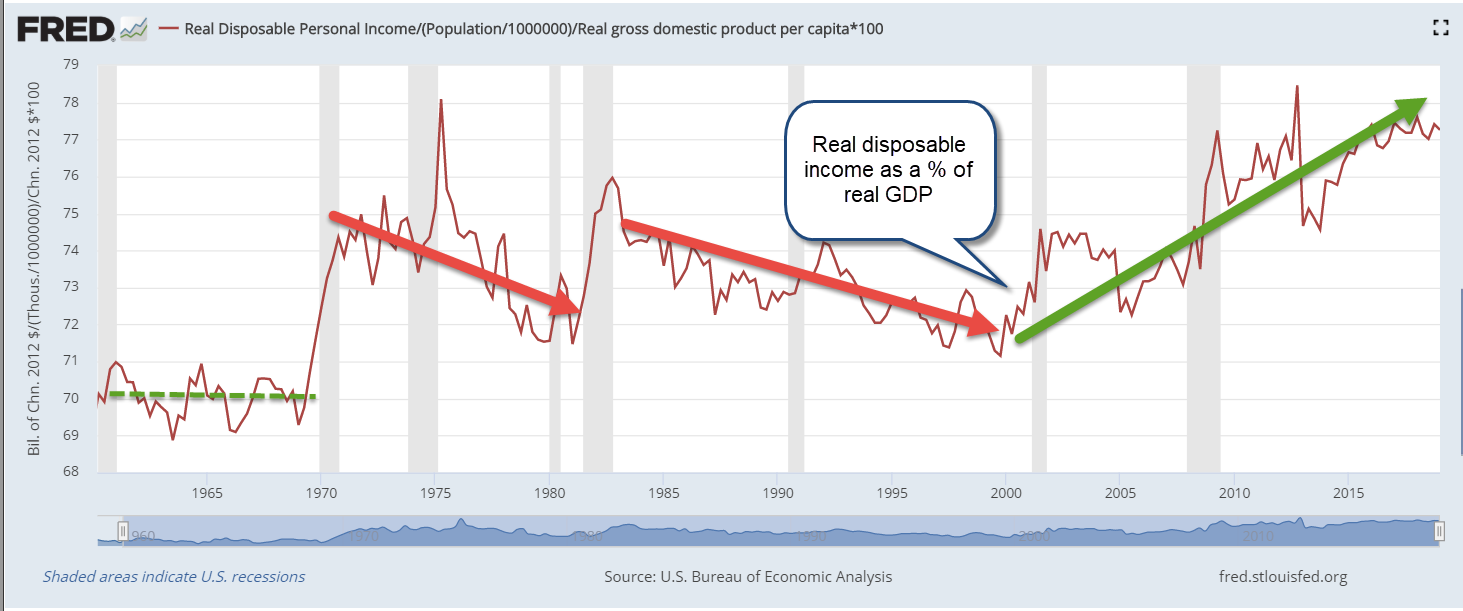

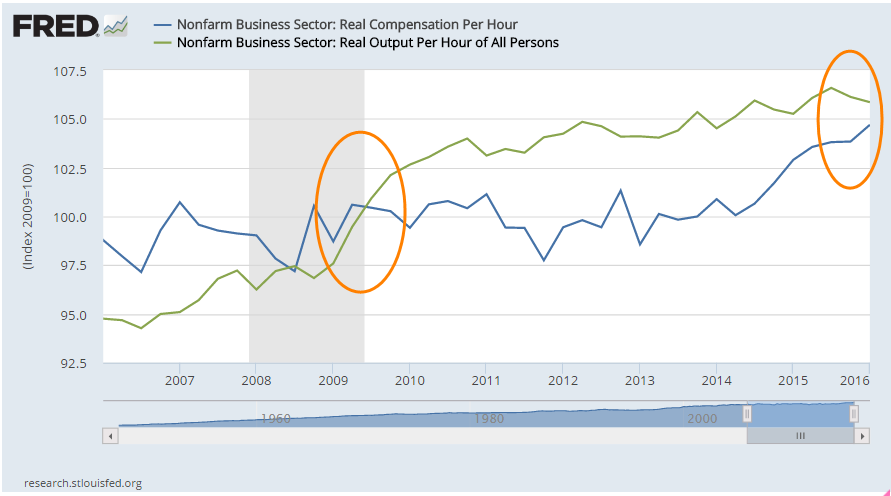

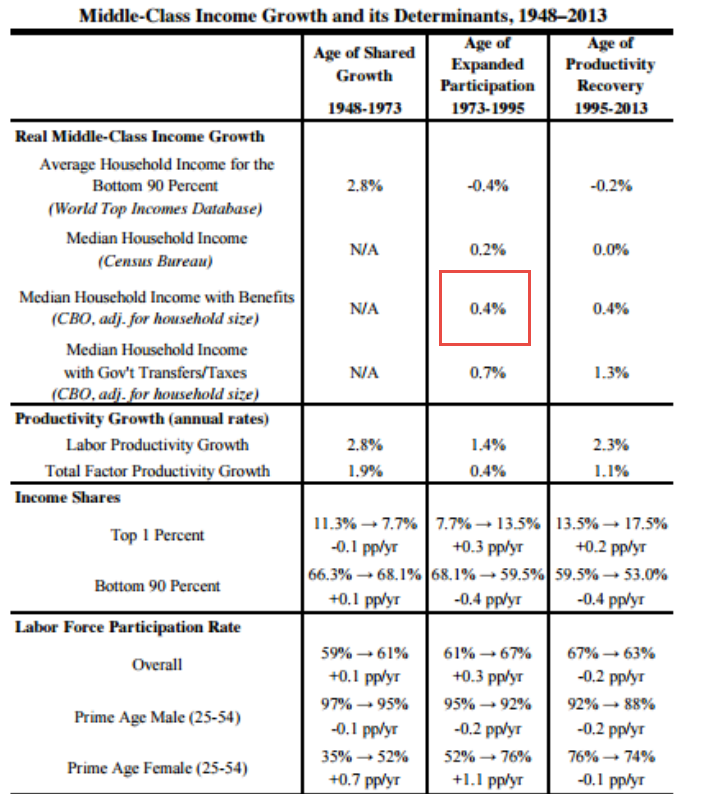

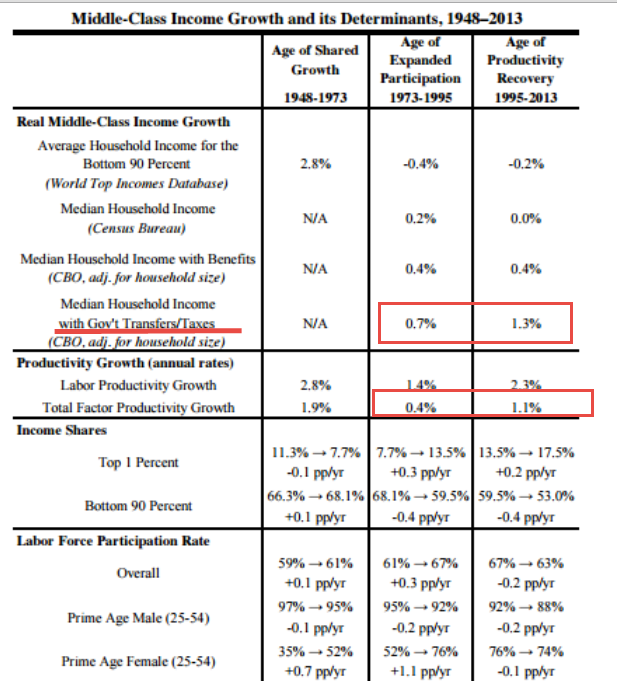

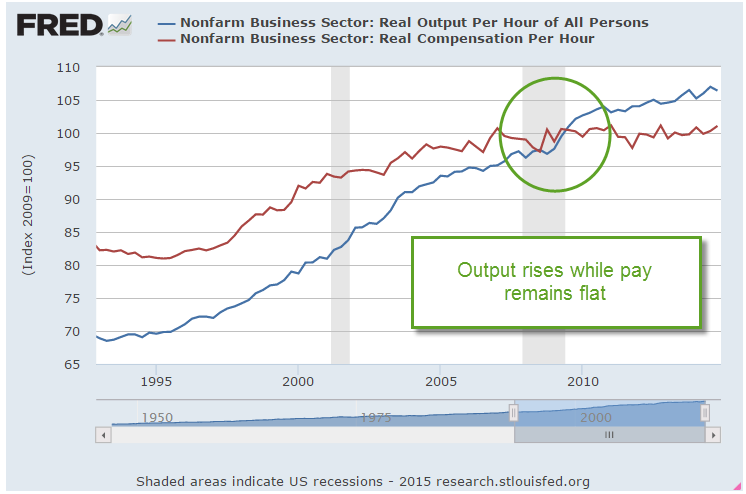

Although incomes have kept up with inflation, they have not kept up with productivity gains. Most economists believe that a worker gets paid the value of her marginal product. If that is so and there have been productivity gains since 1987, then incomes should reflect some of those gains.

The BLS calculates a Total Factor Productivity that includes capital and labor. A 2018 study by the BLS calculated 2.9% annual output growth since the late 1980s. Estimating the sources of growth, they found that capital had contributed 40% more to productivity than labor but, even so, labor’s share of the gains should be at least 1% annually. If so, the MHI would be considerably higher today.

There are several reasons why American household income has not kept pace with productivity gains. They include:

A smaller percentage of workers belong to a union and so have less bargaining power. According to the BLS (2022), only 10.3% of all workers belong to a union. Among public sector workers the rate is far higher – 34%, but only 1 out of 7 employees are in the public sector.

Critics argue that greedy business owners are keeping all the productivity gains. Perhaps so, but that requires market power. Why have workers continued to work for less than a livable wage? Business owners complain that they have little pricing power. If workers and businesses have no pricing power, who has it? It may be buried in the garbage heap where capital goes to die in a competitive and fast changing marketplace. Before 2000, consumption of fixed capital accounted for 15% of GDP. Today, it has risen to 17%. In a $24 trillion economy, a 2% change is a lot. In a world where companies must innovate to survive, we notice only what survives. Growth comes at a cost.

Some say that the job mix has changed so that it is difficult to compare incomes, job skills and productivity with those of 35 years ago. There are now more lower paying service jobs, fewer high paying manufacturing jobs.

Making comparisons tough are the smaller household size today. With fewer people per household, incomes won’t be as high. The 1960s and 1970s saw explosive growth in household formation and this helped fuel the high inflation of the 1970s. Since then household formation has trended upward at a slow pace. The ratio of households to population today (.39) is only slightly higher than it was 40 years ago (.36). That slight difference does not account for the lost income in unpaid productivity gains.

Some argue that illegal immigrants are taking American jobs. They are willing to work for lower wages, and are reducing the bargaining power of American workers. There are an estimated 12 million undocumented immigrants in this country, including children and people past working age. Many of those who do work do so in agriculture which is not counted in the payroll numbers. Some work in construction but those jobs are only 5% of the workforce. There wouldn’t be any noticeable effect on the incomes of 150 million workers.

So where are the missing productivity gains?

/////////////

Photo by Proxyclick Visitor Management System on Unsplash

BLS. (2018). Sources of growth in real output in the private business sector, 1987-2018. Productivity. Retrieved May 1, 2022, from https://www.bls.gov/productivity/articles-and-research/source-of-output-growth-private-business-productivity-1987-2018.pdf. Note: this is a short summary less than one page. Multi-factorial growth is the difference between calculable inputs and total output. I have divided it up according to the ratio of each factor’s input. Interested readers can find a list of articles on productivity at https://www.bls.gov/productivity/articles-and-research/total-factor-productivity-articles.htm

BLS. (2022, January 20). Union Members – 2021. Bureau of Labor Statistics. Retrieved April 30, 2022, from https://www.bls.gov/news.release/pdf/union2.pdf

FRED Construction Employment: USCONS – 7.6 million. Total employment – 151 million.

FRED Employee Cost Index – Total Compensation: ECIALLCIV, adjusted for inflation using PCEPI.

FRED Median Household Income: MEHOINUSA646N

FRED Total Factor Productivity at Constant Prices RTFPNAUSA632NRUG

M.I.T. (2022). Living Wage Calculator. M.I.T. Retrieved April 30, 2022, from https://livingwage.mit.edu/counties/08031

///////////////