October 24, 2021

By Steve Stofka

There are two types of federal benefit programs: those that require “dues” to qualify for benefits and those that are means-tested. Social Security is an example of the first type. With some exceptions recipients must contribute to the program to qualify for benefits. Supplemental Security Income (SSI) and the SNAP food program are examples of the latter. A person’s circumstances, not their contributions, determine their qualification for benefits. Because people think of Social Security as an insurance program, not a government charity, it is the “third rail” of politics. Voters feel that they have paid into the system and deserve their promised benefits. The Boomer generation points to the $2.9 trillion in the Social Security Trust Fund as evidence they have indeed paid into the system. Talk of cutting benefits can earn a politician the boot. The question is: have workers paid in enough?

Our choices today are constrained by the priorities and choices of past generations. The Social Security program was created in 1935 to relieve seniors burdened with crushing poverty. The failure of thousands of banks prior to that time had wiped out the lifetime savings of many workers. With a commanding majority in the House and Senate, Democrats responded to the plight of many seniors. Those first generations received far more in benefits than they paid in contributions and created what is called a “legacy debt.”

In 1965 the program was expanded and in 1975 benefits were indexed to inflation. By that time, the sum of contributions exceeded benefits paid so that the trust fund had a reserve of 56% of benefits expected to be paid that year. By 1983, the reserve stood at only 18% of that year’s anticipated benefits. High inflation during the 1970s and some miscalculations in computing inflation adjustments to beneficiaries had depleted reserves. At that time, the Boomer generation ranged in age from 20 to 37, about the same as the Millennial generation today. By 2008, the first of the Boomer generation would be eligible for benefits. A commission recommended accelerating tax increases to build up the trust fund in anticipation of this demographic bulge. When the great financial crisis hit in 2008, the trust funds had 358% in reserves. It should have been much more.

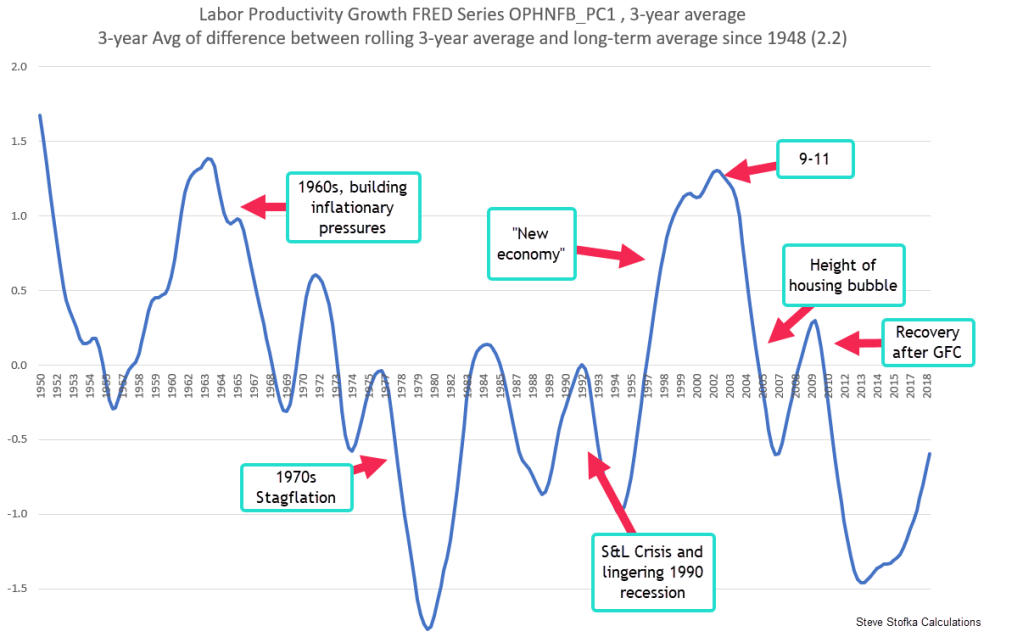

Economists and politicians have remarked on the slow wage growth of the past decades. The cause of that slow growth is a matter of political perspective, but one thing is certain. Labor productivity has slowed as well and there is no consensus on the cause of that. In the chart below, I’ve smoothed out some data from the Bureau of Labor Statistics on Labor Productivity to show the long term trends. I set the 70-year average of 2.2% annual growth at zero to show the periods of below average productivity. The chart shows the two decades of below average growth from 1975 to 1995.

In a 2001 paper William Nordhaus (2001, 2), a researcher at the National Bureau of Economic Research (NBER) noted “after growing rapidly for a quarter century, productivity came to a virtual halt in the early 1970s.” Nordhaus attributed the growth of the late 1990s to the “new economy,” the communications technology and software development at the dawn of the internet. The productivity surge lasted about a decade, succumbing to the drag of low productivity in the service sector in general.

Because many service jobs have low productivity growth, America has given up the robust growth of the modern industrial age in the post-WW2 period. Low wage growth means less taxes to fund benefits and political tension. Since 2010, Social Security has been tapping the trust funds to pay benefits as the Boomers retire. By 2034, the trust funds will be depleted and the trustees estimate that each year’s taxes will be enough to pay about ¾ of promised benefits unless taxes are raised or general taxes are used to pay benefits. As much as workers have paid in SS taxes, it wasn’t enough. The Social Security trustees estimate that an additional 2.83% in taxes would cure the problem for another 75 years but politicians don’t have the courage to push taxes higher.

The program was created during the depths of the Depression. The generation that enjoyed SS benefits far above their contributions has passed on, leaving their legacy debt with us. They believed that the future would be like the past, that strong productivity and wage growth could pay inflation adjusted benefits for 15-20 years of retirement. Across a divided country and a divided Congress, we must put down the word weapons and ask ourselves “What are we going to do?”

////////////////

Photo by Markus Spiske on Unsplash

Nordhaus, W. D. (2001, January 01). Productivity growth and the New Economy. Retrieved October 24, 2021, from https://www.nber.org/papers/w8096

SSA. (2021). Social Security – Trust Fund Ratios. Retrieved October 24, 2021, from https://www.ssa.gov/oact/tr/2020/lr4b4.html