March 27, 2016

Happy Easter!

Before I take a look at a dynamic allocation model for older readers, I’ll quote from a paper published in the last decade: “adequate savings is the primary driver of retirement success and is approximately 5 times more important than Asset Allocation.” For readers who are not near retirement, what is called the accumulation phase of life, the one word that sums up a lot of financial advice is “Save.”

A reader sent me an article that recounts several common sense strategies for investors nearing or in retirement. I was especially interested in a strategy for recent retirees: to have a cautious 30/70 stock/bond allocation in the first years of retirement and transition to a more agressive 60/40 portfolio over 10 – 15 years. Is this madness? Conventional advice advocates more caution in the later years of life.

The initial conservative approach is designed to minimize the negative effects that a bear market would have on a portfolio in the first years of retirement. At seven years old, the current bull market is long in the tooth, so to speak. One of the authors of the article is Wade Pfau, whose Retirement Researcher site I include in my blog links in the right column of this blog. I have a lot of respect for Mr. Pfau’s work and his sensibilities so I was inclined to trust this recommendation.

In order to forecast, one has to backtest, and the authors have more sophisticated portfolio allocation testers than many of us have. I have recommended before a free allocation tester at Portfolio Visualizer. Their web site also has a free Monte Carlo simulation tool (MC). What the heck is that, you ask?

For Dr. Who fans, an MC is like a time trip in the doctor’s Tartus. First we set the thing jab on the whozee panel, spin the furbee wheel clockwise to go forward in time, then stand one pace to the left – do not stand on the right! – of the big lever as we pull the lever knob.

For those of you without a Tartus, an MC uses historical returns and creates a number of what-if possibilities based on variable parameters like the period of time to run the simulation, the inflation rate, the withdrawal amount or rate, the asset mix, etc. If I start out with $1M in savings at age 65, for example, and I take out $40,000 each year adjusted for inflation, what are the chances I will have any money left after thirty years, at age 95? Will the Daleks catch up with my savings and exterminate it? No, not the Daleks!

The remaining balance, the money a person would have left, is ordered by percentile: 25%, 50%, the median, and 75% are common. Example: A remaining balance of $500K for a certain allocation at the 75% percentile means that 75% of retirees will have less than that amount.

A success rate is computed; a 75% success rate means that you don’t run out of money in 75% of the simulations. What about the other 25% of the time? Care to roll the dice on that one? A 90% success rate is considered a desireable minimum in the industry. I tend to focus on both the success rate and the median balance.

If using historical asset prices as a basis for computing future possibilities, an important assumption is the time period. If the past forty years have included some really good returns for a few decades, then the MC results will be optimistic. What if the next twenty years are not so good? Move in with your kids?

Using the historical data of the past 20 years or 40 years as a basis for future returns is a bit optimistic, I think. During this past twenty years, bond prices have been inflated by extraordinarily low interest rates set by the Federal Reserve. The price of a composite of intermediate corporate bonds, Vanguard’s VFICX mutual fund, has almost quadrupled since 1995. A 60/40 stock/bond mix has returned 9.5% over the past 20 years. We are unlikely to see such returns in the future. My gut instinct is to err on the side of caution and assume a 7.5% return on a 60/40 mix, and a 6% return on a 30/70 mix.

Here’s the assumptions: $1M initial portfolio; 30 year future period; withdraw an initial $45K adjusted annually using a 3% inflation rate.

.nobrtable br { display: none } td {text-align: center;}

| Stock/Bond % |

Success Rate |

Median Bal |

| 30/70 |

57 |

$278K |

| 60/40 |

73 |

$1.6M |

| 30/70 –> 60/40 |

92 |

$1.7M |

Using a 30/70 mix for the first 5 years and a 60/40 mix for the following 25 years gives a median balance of $1.7M after 30 years, about the same as the 60/40 mix above BUT the success rate shoots up to 92%. The authors suggest a gradual transition but this simple simulation shows the advantage of a dynamic allocation strategy.

In short, this does look like a good strategy.

Readers who want to use the more optimistic historical returns of the past 20 years would see these simulation results:

| Stock/Bond % |

Success Rate |

Median Bal |

| 30/70 |

92 |

$2.7M 10 times higher! |

| 60/40 |

88 |

$4.3M |

| 30/70 –> 60/40 |

92 |

$4.3M |

Using historical returns for the past 20 years sure pumps up the median balance on the conservative allocation.

///////////////////

Existing Homes

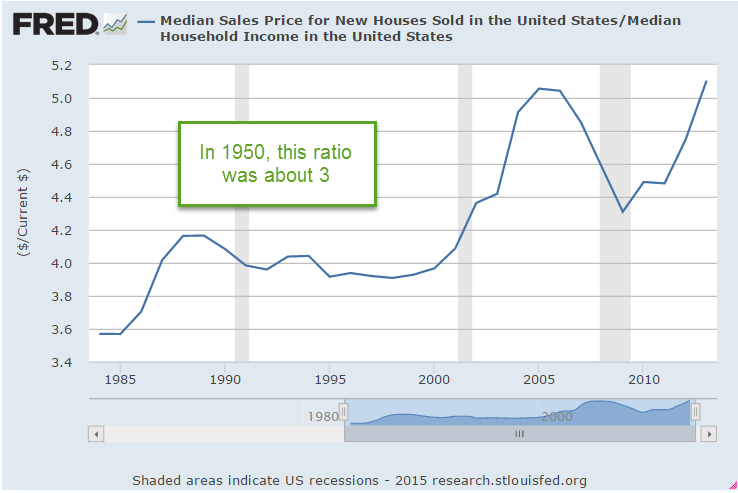

Existing Home sales fell 7% in February. Mortgage rates are at all time lows. What’s going on?

Below is a chart of the ratio of Existing Home Sales to New Single Family Homes. As you can see, the ratio has remained fairly steady over the past several years. The spike in the ratio in early to mid 2013 coincided with historically low mortgage rates (Money) . In the last quarter of 2015, this ratio started sinking despite the stimulus of low interest rates. Are home buyers at all levels being priced out of the market?

////////////////////////

The Immigration Carousel

The 1900 census counted a total population of 78 million, of which 13% were foreign born. Responding to a growing hostility toward immigrants, Congress passed strict quota laws for immigrants in 1921 and 1924. Regarded as lazy, shiftless, boorish, stupid, or criminal, southern Europeans were among the undesireable groups. During the 1920s, the foreign born population began to decline and, beginning with the 1950 census, stayed below 8% for 40 years.

The 2000 census counted 11% of the population as foreign born. The 2010 census counted 13% foreign born, so that our population mix now matches that of the early 20th century.

It is hardly surprising then to see a growing antipathy towards immigrants in the past decade. Donald Trump’s candidacy is partly fed by the same anti-immigrant sentiment prevalent in the America of one hundred years ago. We like to think we have put some crude and cruel instincts behind us, but we are again confronted with our “herdness.” We will tolerate “others” as long as their percentage of the herd remains relatively small. In America, that tolerance limit seems to be 10% foreign born. How does America compare to other countries?