June 7, 2026

By Stephen Stofka

I am recovering from hip surgery this week. I hope to see you next week.

////////////////

Photo by Alexey Taktarov on Unsplash

June 7, 2026

By Stephen Stofka

I am recovering from hip surgery this week. I hope to see you next week.

////////////////

Photo by Alexey Taktarov on Unsplash

May 10, 2026

By Stephen Stofka

Last week, I wrote about the Supreme Court’s cutting away key portions of the Voting Rights Act. This week, I want to understand the conservative attempt to keep the country imprisoned in the sentiments and prejudices of the 19th century.

Three-quarters of the states must vote in favor of an amendment to the Constitution. It takes only a plurality of Supreme Court justices to amend the Constitution through reinterpretation. Throughout our history, the Court has acted as a second Congress, limiting or amending statutes using some judicial theory invented by one or more members of the Court. The Congress must jump a high hurdle to make substantial constitutional changes. The Court has only to step a bit higher to have the same effect.

At the Constitutional Convention, the framers underestimated the power of the judiciary so badly that they left it up to the first Congress to draft the rules. What if the Constitution had set the same three-quarters threshold for substantial changes to the Constitution? Today’s court would need seven justices to set new precedent, amend or overturn a former precedent. Key decisions of the Roberts’ court would not have met the minimum threshold.

Marbury v Madison and Roe v Wade (abortion) would have passed the test. Dobbs v Jackson Women’s Health Organization, which overturned Roe, would not have passed the test. Infamous rulings like Dred Scott v Sandford and Plessy v Ferguson would have passed the test. The 13th and 14th Amendments overturned the Court’s decision in Dred Scott. Brown v Board of Education overturned Plessy and was a unanimous decision.

Conservatives on the court often refer to customs or precedents mentioned in 18th and 19th century text. In District of Columbia v Heller, Justice Antonin Scalia used 18th century dictionaries, English common law and practices in the American colonies to understand what the words “bear arms” meant in the Second Amendment. What was the notion of self-defense in colonial times? He used this historical foundation to justify his interpretation of the Second Amendment as an individual right to carry a gun. Scalia declared that the First, Second and Fourth Amendments were pre-existing rights. The Constitution could only recognize then, not create them. Thus, it could not diminish or take away those rights.

Scalia was a proponent of Originalism, a judicial analysis which insists that modern opinions rely on the meaning of texts when a law was written, and the historical practices and statutes prevalent in that period. Originalism has a central conflict. The Constitution, the Bill of Rights and statutes written during the decades before the Civil War were based on a different understanding of rights than we have today. In the 18th and early 19th century, rights depended on each person’s status in society, their race, gender or property. Different people had to play by different rules. A historical analysis of the law must struggle to overcome those multiple standards and reach a precedent that is consistent with modern sensibilities.

The problem was that different people had different sets of rights. White people had rights that black people didn’t. A shop owner had rights that his workers did not have. Women had few rights. Under the common law custom of coverture, a married woman’s legal status was merged with her husband. She could not make a contract, own property or sue in court. The English jurist William Blackstone wrote that a husband and wife were one person in the eyes of the law.

The Declaration of Independence stated that “all men are created equal, that they are endowed by their Creator with certain unalienable Rights.” In America, unlike Britain, official titles of class and nobility were forbidden, but people understood that there were roles in society, and roles were not equal. This was especially true in the southern states whose economies were founded on agriculture. Their social hierarchies were more static than those in the northern states. My maternal great-great-great grandfather was a farmer in S. Carolina, and three succeeding generations of sons were farmers. Rights varied by one’s role in society. The responsibility of a state was to manage the roles and rules within that society.

It’s important to understand that, prior to the ratification of the 14th Amendment, the protections contained in the Bill of Rights applied only to the Federal Government, and not to the states. The founding states were concerned that the central government not interfere with the sovereignty of the states in how they dealt with their citizens. The protection of the rights of their citizens was the main responsibility of the states. In fact, the constitutions of some states afforded far better protections of individual rights than was contained in the Bill of Rights.

By the time of the Civil War, Americans recognized that the southern states had managed those roles and rules to segregate or exclude black Americans in private and public life. After the Civil War, the Equal Protection and Due Process clauses of the 14th Amendment promised to equalize the rights and freedoms that people enjoyed. Following the passage of the Civil War amendments, several Supreme Court decisions reduced their scope by drawing distinctions between civil and social rights, and enacted double standards for government and private business.

In 1875, Congress passed the Civil Rights Act to ensure the equal treatment of black Americans in hotels and inns, in theaters and on public transportation. In The Civil Rights Cases(1883), the Court ruled that the Fourteenth Amendment allowed the federal government to regulate discriminatory behavior by state and local governments, not private businesses. This was an 8 – 1 decision, reflecting the normal understanding of rights as they were understood at the time the 14th Amendment was ratified. If Justice Scalia’s Originalist approach is correct, then today’s justices should apply that same distinction between government and private parties.

In Plessy v Ferguson(1896), the court ruled that segregated but equal accommodations enacted by state law did not violate the equal protection of the law. This was a 7-1 decision, reflecting the dominant understanding of equal protection at the time the 14th Amendment was ratified. The lone dissent, authored by Justice Harlan, did not reject the distinction between government and private parties but noted that a private institution like a railroad serves a public function and is subject to the protections contained in the 14th Amendment. In Brown v Board of Education (1954), the Court overturned that precedent of “separate but equal.” If Justice Scalia’s Originalist approach is correct, then today’s justices should apply that same understanding of “separate but equal,” and overturn the precedent set in Brown. Do you think that is not coming? Just wait.

In fact, the inevitable outcome of Originalism, consistently applied, is to resurrect these 19th century understandings, the sentiments and prejudices of that age. Both the Originalism and Textualism projects will rationalize stratifications in our society because of the roles that people play. Six of the current Court’s justices are involved in one or both of these projects.

In Trump v United States (2024), the Court gave former Presidents “absolute immunity for actions within his conclusive and preclusive constitutional authority,” and “at least presumptive immunity from prosecution for all his official acts.” This is 19th century court jurisprudence that sets out different rules and rights depending on one’s role in our society.

In Dobbs v Jackson Women’s Health Organization, Justice Samuel Alito concluded that the Constitution did not “confer a right to abortion.” He based his reasoning on 18th and 19th century abortion regulations and English common law, all of which regarded women as functions, as roles in our society. Women bore the children, kept the house and cooked the meals. Society did not recognize a woman’s personal boundaries. With that understanding as a foundation, it is no wonder that Alito could find no sense of privacy, of personal sovereignty for a woman who was performing a role similar to a brood cow.

The 18th century philosopher, Immanuel Kant (1724 – 1804) formulated a rule of ethics that we should treat people as ends, not just as means. In other words, people were more than the roles, the functions they played in society. That ethical rule ran counter to 18th and 19th century legal jurisprudence which regarded people as functions, not beings in their own right. In fact, much of English common law and Blackstone’s Commentaries, used frequently by conservative justices on the court, regard people as functions within society. By basing their reasoning on that ancient jurisprudence, the conservative justices on the Court reject Kant’s rule.

Three of the six conservative justices might serve another 20 – 25 years, so we can expect more of this type of jurisprudence in the future unless Congress changes the number of seats on the Supreme Court just as it did after the Civil War. That is quite an undertaking but the Originalism and Textualism projects were big undertakings that began in the 1970s with the establishment of the Federalist Society, ALEC and Heritage Foundation.

We can be a nation rooted in the present and looking to the future, or we can be a nation trapped in the birdcage of historical prejudices. The conservative court constructs a cat’s cradle of confusing opinions and unexplained shadow docket rulings that the lower courts have struggled to apply. The court itself has little to no checks on its power to interpret the Constitution and we must correct that. We can open the bird cage. I hope to see you next week.

/////////////////

Photo by Enrique Chagoya on Unsplash

Home prices could be a simpler alternative measure to guide the Fed’s monetary policy.

http://dlvr.it/SwxWT9

October 2, 2022

by Stephen Stofka

The dollar is the world’s reserve currency and its strength – its price relative to other currencies – is straining both the economies and the financial expectations of other countries. Businesses in developing countries with an unreliable currency regime often have to borrow in dollars – what is called “dollar denominated debt.” Businesses must make their loan payments in dollars so they must trade in ever more of their local currency to get the dollars to make the payment. European nations stocking up on liquified natural gas (LNG) from the U.S. are feeling the pinch as well. Why is the dollar strengthening?

In international finance there are two equations that model the relationship between expected inflation, exchange rates and interest rates. Currency traders are expecting inflation to moderate more quickly in the U.S. than in other countries. Because the U.S. has a better supply of natural gas, its energy prices will be less affected by the war in Ukraine. Secondly, the Fed has been increasing interest rates, enticing investors in other countries to invest their money in U.S. debt. The dollar-euro exchange rate has not been this low since 1999 when the Eurozone countries began using a common currency, the euro.

When the dollar gets stronger, exports decrease because American goods are more expensive to buyers in foreign countries. Imports become cheaper so Americans buy more stuff from other countries. However, if the U.S. is sliding into a recession, Americans are less likely to buy enough European imports to offset the LNG that European countries will buy from the U.S. This will increase the demand for dollars relative to the euro, further driving up the price of dollars in other currencies.

The dollar has been strengthening against other forms of currency like gold and digital exchange mechanisms like Bitcoin. Priced in dollars, gold has lost about 16% of its value in the past six months. Bitcoin has lost 60% since March. Gold is both a commodity and a currency. Gold holds a store of work that it can do in the future. It has cosmetic and industrial uses.

Bitcoin is the product of past work only – a “proof of work” done in the past. It stores no capability of future work. It takes a lot of electricity and computing power to mine Bitcoin but it cannot store electricity for future use. If it could do so, the price of Bitcoin would go up when electricity prices went up.

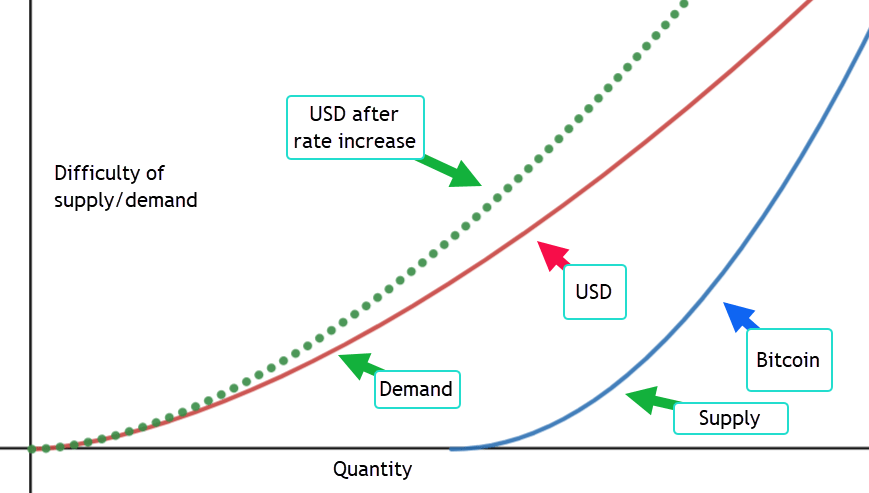

In the graph below I’ve illustrated a key difference between the dollar and Bitcoin. On the right is Bitcoin. Its algorithm incorporates a “diseconomies of scale.” As more Bitcoin is mined, it takes more effort to mine Bitcoin. Bitcoin focuses on the difficulty of supply.

On the left is the fiat dollar. There is no difficulty in supplying it. The Fed focuses on the demand for the dollar by adjusting the interest rate, the bend in the curve. It is currently tightening that bend – the dotted green curve – and increasing the difficulty of getting more dollars. The dollar can respond to changing demand more easily than gold or Bitcoin because it targets demand.

Like Bitcoin, the dollar stores no future work. In an article earlier this year (2022), I wrote that America’s store of wealth was both a proof-of-work, proof-of-stability and proof-of-trust. The dollar itself is only a sign of trust in American institutions. The checks and balances of our system of government ensures that most policymaking is incremental. While that frustrates Americans, the relative predictability of U.S. policy is reassuring to foreign investors. Americans often run around like crazy monkeys on the deck of a cruise boat but the ship is unlikely to make a large course correction.

Think of the bend in the curve as a toll for using the highway to the future. Bitcoin’s curve is rigid. The toll remains the same. Bitcoin enthusiasts would maintain that this rigidity should shift the curve to the right over time, increasing the buying power supplied by Bitcoin.

Let’s look at three approaches.

1) Bitcoin limits the length of highway that will be built. Enthusiasts claim that this will make each “mile” of the bitcoin highway more valuable.

2) MMT advocates offer a different solution. As long as there are resources – both labor and material – available, build more highway. By targeting the supply available, congestion will ease.

3) The Fed offers an approach that targets demand, not supply. The Fed raises and lowers the interest rate – the toll – to get onto the highway to the future. Raising interest rates is a form of congestion pricing. High inflation means that there are too many people using the available length of highway. The Fed has promised that it will keep raising the toll until fewer people are using the highway. As demand declines, some of those working on the highway may lose their jobs. Unemployment will increase but historically it is very low.

The strength of the dollar against other currencies, including Bitcoin and gold, indicates increasing demand for the Fed’s approach. What is the morality of an international floating rate regime where businesses in a developing country have to work even harder to pay their dollar-denominated loans? Bitcoin advocates claim that global adoption of Bitcoin will make a more even playing field, reducing the advantage that developed countries have over developing countries. That can be the subject of another article.

////////////

Photo by kyler trautner on Unsplash

Stofka, S. (2022, April 16). Fortress of Trust. Innocent Investor. Retrieved October 1, 2022, from https://innocentinvestor.com/2022/04/17/fortress-of-trust/

October 17, 2021

by Steve Stofka

A current topic of controversy is a popular comedy special on Netflix featuring the acerbic wit of Dave Chappelle. In this last of several Netflix specials, Mr. Chappelle airs many grievances, one of which involves previous remarks he made about transgender people. Hannah Gadsby, an Australian comedian with a quiver of arrows and the skill of a markswoman, targets the bias and bigotry in our culture. Recently she has aimed at some remarks by Netflix executives who defended Mr. Chappelle’s humor. Ms. Gadsby leads a growing audience of voices who worry that the Chappelle special could inflame hate attacks against people with a non-mainstream sexual orientation or gender identity.

In past centuries society has regarded non-straight orientation as a behavior outside accepted norms and ostracized those individuals as deviants. Social scientists have now recognized the importance of biology in sexual orientation and gender identity. Recent jurisprudence and law have accorded equal access to marriage, property and employment regardless of sexual orientation or gender identity.

Black people have long been ostracized for their skin color and there is no dispute whether skin color is biological or behavioral. Decades of law and jurisprudence have not been able to undo the bigotry and bias against those with black skin. Two comedians, each from a marginalized group, confront each other and the larger society over the nature and construction of identity. This is an enduring debate.

2400 years ago Aristotle attributed the falling of objects to their nature. People accepted that view until Galileo showed that it was a dynamic of forces, not an inherent nature that made things fall. Explanations that attribute causes to nature – the within – are attempts to answer the question of why. Explanations that investigate the dynamic between things answer the question of how. In the 17th century John Locke argued that people had a natural right to private property that no king could dispose of without violating a natural law. That was why society had an obligation to protect property rights. The how of that natural right involved a dynamic between God, Adam and Eve when He turned them out of the Garden of Eden and set them to toil the earth for their food.

In his special Mr. Chappelle adopts a realist approach, arguing that gender is an unalterable fact of nature. An alternative perspective is that gender is a construction of biological, social and psychological factors. The nature vs. dynamic identity debate exists in many fields. Some people claim that only gold has real value as a money, regarding paper money as a mass illusion of value. Economists argue that the value of something is what you will give up for it, a value based on a dynamic. Karl Marx thought the fundamental value of any good was the labor that went into producing or harvesting it. Mainstream economists assume that the value of a good is its utility to the user, a fluid construct of preference, time and price. The debate over sexual orientation and gender identity is another manifestation of this conflict of perspectives.

Some comedians walk the dark alleys of our society and psyche. In the 1960s, Lenny Bruce and George Carlin questioned mainstream values. In a brash and vulgar style, Bruce openly flouted speech prohibitions and police often arrested him during his act. His notoriety helped bring these laws to the Supreme Court where they were ruled unconstitutional. In the 1970s, Richard Pryor offended many with his off-color remarks as he dug deep to unearth the hatred and hypocrisy that rotted our culture. In other cultures today, comedians who ridicule authority figures are arrested. Caustic remarks are against the law. Liberal societies tolerate a wide range of speech and views. Those are the two choices on the menu: authoritarian or liberal. I’ll take the liberal, please.

//////////////

Photo by ANGELO CASTO on Unsplash

September 19, 2021

by Steve Stofka

Economics is built on the principle of the rational person capable of making a choice between two options. In casual conversation we use the word “rational” to mean making sense but in economics it means making a choice. The choices presented may have constraints that make the word “choice” seem inappropriate. Does an addict have a choice? Yes. Sometimes we steer our lives with a critical choice of more or no more, having to choose between an unbearable more and a no more that contains an equally unbearable number of unknowns.

We might leave a job with only the hope that we can find another one soon. We may cast a no more vote, rejecting an incumbent for an unknown candidate. People living in the path of a hurricane or forest fire must make the difficult choice of evacuating the area or staying in their home and hoping they will be safe. Making a no more choice with family relationships can twist a person’s mind and soul in knots. A battered women may endure more until they reach the point of no more and leave their situation.

As the Delta variant of Covid-19 sweeps through the population, many people are making difficult life choices about their jobs. In March 2020, the number of job openings plunged more than a third from 7 million to 4.6 million. In January this year, openings regained their pre-Covid levels and have risen quickly since then. The July report indicated almost 11 million openings, a series record.

After adjusting to online work, some workers have made that a critical preference. They have said no more to long commutes. Some have moved from dense urban areas to less populated states like Montana where rents or house prices will not consume half a paycheck. They have said no more. The sudden job loss last year caused some workers to rethink their priorities and career choice. The lack of affordable childcare has been a deciding factor for some workers.

In economics, utility theory explores a choice between quantities of two goods. For example, will I have more pizza or more ice cream? These simple unrealistic examples help a student practice the concepts but are not suitable for no more life choices. Because these decisions act like switches, their calculations are hard to model. We may be able to bargain with our company who wants workers back in the office. Many times, we have to make a hard choice, one that can’t be undone.

We may revisit difficult choices, trying to understand and refine our decision making process. Many younger workers will look back and see this as a defining moment in their life. Some will wonder what if, replaying their choice. In a period of five years, our grandparents and great-grandparents endured rationing during WW1, followed by the Spanish flu that killed thousands, then the severe recession of 1921. Life narrowed their choices and they endured. By the time a person reaches their 80s, they have decided on more about 30,000 days. We remember the no more decisions more than we remember the many decisions of more. Each day is a crossroad.

/////////////

Photo by Einar Storsul on Unsplash

August 29, 2021

by Stephen Stofka

In the short version of Monopoly, the property deeds are shuffled and dealt out to the players. Some think that God does the same with our talents and circumstances and that it our duty to play with what we are given. They argue that the proper role of government is to provide for the common welfare, like defense, police, schools and infrastructure. Some take a more secular view, arguing that the hands dealt are largely the result of past policies and practices, the good, bad and quite ugly. Given this history, government has a duty to correct these inequities. They argue that government should take an active role in improving individual welfare to raise the general welfare. Moderates argue that a mixture of individual and common welfare programs will best improve the general welfare but they disagree on priorities.

According to the Bureau of Economic Analysis, federal assistance for education, welfare and housing has increased 3 times since 1960 as a percent of GDP. During that period, health care spending at the federal level has increased 9 times; at the state and local level it has increased 3 times. To help offset these increases, federal spending on defense has declined by 67%. What distinguishes all these increases in spending is that they are targeted toward individual welfare in the hopes that an improvement in individual welfare will raise the level of general welfare.

State spending on the common welfare like education and transportation have both declined 25%. After several decades of this shift in strategy, our schools, roads, water and sewer systems are in bad repair because state revenues as a percent of GDP have changed little in the past fifty years while spending on individual welfare has increased. The $3.5 trillion infrastructure bill being debated in Washington targets that neglected common infrastructure.

The spending mix of families has changed as well. In 1964, 33 cents of every family’s expenses was spent on food. Today, it is only 13 cents, a drop of 67%. Despite that decrease in food spending, 1 out of 12 families relies on food stamps, the SNAP program, to help feed their families. Why is that? In the past four decades housing costs as a percent of GDP have gone up 30% (CRS, 2021). Since housing is the largest monthly expense for most families, this sizeable increase has significantly lowered individual welfare. Government programs help alleviate that stress.

During the Depression, a shared suffering prompted a shift in the role of government from public projects, the common welfare, to individual welfare. Many New Deal programs incorporated both elements in their design. Electric generating projects like the Hoover Dam and Tennessee Valley Authority (TVA) were built by men who sent part of their government paychecks to their families to help with food and housing expenses. A contribution to the common welfare helped relieve individual suffering. During that era, the Roosevelt administration and Democratic Congress initiated the Social Security program, requiring working Americans to contribute to a common fund which would be used to pay benefits to contributors when they retired. Those payroll tax contributions were the price of admission to the benefits of the program.

At that time, only states, local communities and private charities administered welfare programs. These were benefits paid to families based on their need, not an admission fee of contributions to the program. In the 1960s, the Johnson administration and Democratic Congress ushered in the Great Society programs that firmly established a precedent that raising individual welfare increased the general welfare. In the late 1970s, Democratic President Jimmy Carter fought this expansive role of government but his sentiments were countered by the liberal wing of his party, particularly the powerful House Speaker Tip O’Neill, a strong believer in the government’s power to correct social problems (Cuomo, 2021).

Conservatives argue that federal programs designed to increase individual welfare exceed the boundaries set out in Article 1, Section 8. Such programs may weaken the supports provided by family, church and local community (O’Neil, 2021, 106). They do not incentivize people to change their behavior. The programs encourage people to cast their vote for those politicians who promise more benefits, making the voting process a transaction, not a civic endorsement of a voter’s values. At a fundraiser in the closing weeks of the 2012 Presidential Election, Republican candidate Mitt Romney commented that the 47% of Americans who paid no income tax were the base constituency of the Democratic Party (Moorhead, 2012). His implication that half of Americans were moochers was a blow to his campaign.

Liberals argue that the “general welfare” clause of the Constitution implies a government duty to improve individual welfare. They counter that many people in poor communities do not have informal support networks to lean on. Many people did not choose their circumstances and their decisions, whether prudent or ill-advised, are not based on gaining access to a government program. Farmers, business owners and executives also vote for government programs like subsidies, lower taxes, and less regulation. All voters are motivated in part by their self-interest.

How do individual, common and general welfares interact? What is meant by the general welfare? What does it consist of? Shortly after the Constitution was presented to the states for ratification, anti-Federalists argued that “providing for the … general welfare” imposed few constraints on the federal government’s ability to tax the people to fund that general welfare (Debates). Americans continue to argue the merits of these programs and the role of government in their lives.

////////////////

Notes:

Photo by Camylla Battani on Unsplash

Congressional Research Service (CRS). (2021, May 3). Introduction to U.S. Economy: Housing market. Retrieved August 28, 2021, from https://sgp.fas.org/crs/misc/IF11327.pdf

Cuomo, M. M. (2001, March 11). The Last Liberal. Retrieved August 28, 2021, from https://archive.nytimes.com/www.nytimes.com/books/01/03/11/reviews/010311.11cuomot.html

Debates. “Centinel,” the pen name of Samuel Bryan, and “Brutus” were among several anti-Federalists who protested the insertion of the “general welfare” clause in the Constitution. See Centinel I and Brutus V editorials.

Moorhead, M. (2012, September 18). PolitiFact – Mitt Romney says 47 percent of Americans pay no income tax. Retrieved August 28, 2021, from https://www.politifact.com/factchecks/2012/sep/18/mitt-romney/romney-says-47-percent-americans-pay-no-income-tax/

May 30, 2021

by Steve Stofka

As an employee, a worker moves between the “work box” and “life box” each working day. The business builds the work box and defines the boundaries for the worker. A worker who is a business and thinks like a business must build a box that incorporates work and life, with a moveable wall between the two. That worker must be more conscious of total production costs or they go out of business.

Almost half of this country’s output is produced by micro and small businesses owned by a few people who take an active part in the business and have their personal fortunes are at stake. Integrating and balancing work and personal life is especially difficult and economic models don’t incorporate the distinct dynamics of these companies. Politicians on both sides of the aisle pay lip service to small business but the substantive beneficiaries of most policies are medium and large businesses who spend heavily to influence lawmakers. Forced to work from home, workers in large companies experienced the production process much like the owners of small businesses. The world’s attention was drawn to a worker’s total costs of production. Will lawmakers and economists finally incorporate the interests and concerns of workers and small businesses?

In economic models there are two inputs to production, capital and labor. In the short-run, capital costs such as plants and equipment are fixed and labor costs are variable. What are the worker’s capital costs of producing that labor? An investment in a home or apartment, in transportation, and in human capital – education, training and past experience. In mainstream economic models, an investment in a home is recognized as an investment, but not as an input to the production of labor. The compensation for the human capital that a worker invests in production is supposedly included in the wage the worker receives. Tax law disregards the costs of housing unless they are traveling expenses away from the primary place of business. How the worker replenishes their physical and emotional needs when they are not at work is not a concern for economics, the Congress or the IRS.

What are a worker’s costs to produce their labor? In the short-run, six months or less, a worker has supplier costs that are either fixed or “sticky,” variable obligations that are difficult to shed. They have leases and financial obligations for living and transportation, for childcare, for education and other commitments to family. For small business owners and many workers during the pandemic, space in the house must be set aside for work activities. In tax law and economic models, those fixed and variable costs are largely disregarded.

Subchapter S corporations are small businesses usually owned by a few shareholders who take an active part in the business. According to the IRS, there are five million S corps. In 2017, they filed 4.7 million returns accounting for $8.1 trillion in business receipts. In that same year, more traditional C corporations filed only 1.6 million returns, but accounted for $21.2 trillion in business receipts (IRS, 2021). Even though larger corporations were only a third of small businesses, they produced almost three times the receipts.

Larger companies leverage that volume to win favors in Congress and state capitols around the country, and those benefits come at the expense of smaller businesses. In political science and economics, it is known as “concentrated benefits, diffuse costs,” a groundbreaking insight of Mancur Olson in 1965 (2014). The few who receive the bulk of the benefits lobby hard to protect them. The many who pay the price are hurt but not crippled by the costs and do not fight as hard for change. Olson challenged the popular notion that the majority always oppresses the minority in a democracy, showing how a minority often controls many agendas. The pandemic has highlighted the plight of the majority of workers in large and small businesses.

In 2017, C Corps deducted 98% of their total business receipts (Table 2.3). S Corps deducted 94% of receipts, but there are also costs of production that a small business owner absorbs because the deduction is either disallowed or requires too much effort to substantiate for the cost of the deduction. For employees, the rules are stacked against them. A worker making $60K per year gets a standard deduction of $12,400, or 20% of their total receipts. If an employee were able to deduct their total costs of production, that standard deduction might be more than $50,000. Employees would pay far less income tax and this would put political pressure on large businesses to pay more taxes. How do a minority of large businesses control the fate of an overwhelming majority?

In Marx’s analysis, the rules of property were a remnant of feudalism, where a small minority of aristocracy controlled the land, had a large influence in policy making, and most workers were agricultural peasants with little education. He thought capitalism was the most formidable force of production that mankind had invented but its rules of who got what were founded on the rules under feudalism – a few got most of the gains.

John Stuart Mill, a contemporary of Marx, agreed that property rights had their foundation in “conquest and violence.” Although a staunch defender of property rights, he acknowledged that the distribution of property was arbitrary and not equitable (Heilbroner, 1997, p. 135). He predicted a gradual transition to socialism where society would distribute the benefits from production more evenly to both the capital and labor responsible for that production.

Those who favor capitalism think that the owners of capital should keep all the profits from production. Those who favor socialism think that the inputs to production should determine the outputs, the profits, from that production. Many advocates on each side are convinced that they are “right.” Believers in capitalism may, like John Locke did in the 17th century, found their “right” on the Bible. Long before game theory was formally developed, both Marx and Mill understood that property distribution was decided by arbitrary rules, not some inherent right. Even Marx disagreed with his own followers in that regard, declaring that he was not a Marxist (Heilbroner, 1999, p. 151). Europeans transplanted their sense of property rights to America, where the acquisition of property was now founded on the three-legged stool of hard work, conquest and violence.

Economic models and tax law were crafted in the environment of 19th and early 20th century industrial production. Capitalists needed workers as disposable cogs in the factory machine and there weren’t enough of them. Policymakers sold a dream to poor but hopeful people in far off countries but awarded all the profits to the capitalists. A lot of workers died in the fight for an eight-hour workday and prohibitions against child labor.

Programs like Universal Basic Income and other variants hope to alter the distribution of profits. Those who gain from the current arrangements naturally resist any change. Laws and attitudes are “sticky” and slow to adapt. The changes in work production during the pandemic may bring new awareness to the totality of the worker’s cost of production, but will that effect policy changes? Let’s hope so.

///////////////

Photo by Martin Sanchez on Unsplash

Heilbroner, R. L. (1997). Teachings from the worldly philosophy. New York, NY: Norton & Company. (p. 137).

Heilbroner, R. L. (1999). The Worldly Philosophers the Lives, Times, and Ideas of the Great Economic Thinkers (7th ed.). New York: Simon and Schuster.

IRS. (2021). SOI Tax Stats – Corporation Complete Report, Table 2.3. Retrieved May 28, 2021, from https://www.irs.gov/statistics/soi-tax-stats-corporation-complete-report. Table 2.4 contains the data on Subchapter S corporations.

Olson, M. (2012). The logic of collective action public goods and the theory of groups. Cambridge, MA: Harvard University Press.

March 28, 2021

by Steve Stofka

At a Senate Banking Committee hearing this week, Fed Chairman Jerome Powell responded to Republican concerns about inflation. The American Rescue Plan signed into law two weeks ago had little Republican support. Without the passage of the law, millions of Americans would have been subject to eviction in the middle of March. Republican Senators expressed few worries about inflation in 2017 when they passed a tax cut that had the same ten-year cost as the American Rescue Plan. It can be difficult to separate the genuine economic concerns about inflation because the topic is used as a political tool.

Mr. Powell reassured Senators that the Fed has the tools to curb inflation. What they lack are the tools to counter deflation. Once the Fed sets interest rates at zero, they cannot lower them, a situation called the Zero Lower Bound. Higher inflation is a persistent worry among older politicians and voters who experienced the high inflation of the 1970s. Since then, the Fed has been given far more power by Congress to prevent a repeat of that decade’s stagflation, the unusual combination of high unemployment and high inflation.

Inflation is one of the many human behaviors that is a function of expectations. Let’s say that, ten years ago, I got scared by a neighbor’s dog who got loose and almost bit me. I changed my route home to avoid the dog. The homeowner may have put up a chain link fence to keep the dog inside the yard, but I don’t trust that the fence can contain the dog. The homeowner could have moved or the dog has died and the threat no longer exists, but my behavior has permanently changed. If I walk on the opposite side of the street, and I don’t see the dog out in the yard, that doesn’t mean that the dog is not a threat.

Fear keeps us alive. A six-year-old may have seen a small spider crawling up a wall, imagines that it could crawl inside their ear while they are sleeping and doesn’t want to sleep in their bedroom. Many of us stop worrying about spiders while we are sleeping, or we think we do. As we grow up, our spiders mature. We lose sleep worrying about financial and relationship issues, our health or our job. Inflation is one of those grown-up spiders.

In the popular understanding, inflation is higher prices. Economists understand inflation as higher wages, the main component of most goods and services. Inflation is both a short-term and medium-term process. In the short run, if demand exceeds capacity to meet that demand, prices will go up because workers have more bargaining power and wages go up. However, as Chairman Powell has noted, the insidious aspect of inflation is that not all prices and wages go up at the same time. Inflation distorts the distribution of income and, in the medium run, affects the accumulation of wealth.

Economists anticipate a return of demand this year; there is a lot of pent-up buying power. Credit card delinquencies are near all-time low, barely above 2%. They were almost 7% in the summer of 2009. The charge off rate is 2.6%, 8% less than it was in 2009. The country has the capacity to meet that demand. There are still ten million unemployed and capacity utilization is below 80%.

There is one troublesome area – housing, which makes up a third of the Consumer Price Index, one of the measures of inflation. For the first time since World War 2, household formation declined in 2020 (FRED Series TTLHH) in response to the pandemic. Last year, many millennials and Gen Z just starting their adult life moved back in with their parents.

Housing supply remains tight. The National Assn of Realtors announced that there were now more real estate agents than homes to sell. The number of housing starts has increased since the housing crisis more than a decade ago, but there are only 7 starts per 1000 working age adults 16-64, slightly above the number of starts during the 1990 recession after the savings and loan crisis.

In response to the Covid crisis, the growth in housing prices (HPI) has shot up from 2% annual growth to over 10% since last March. Although a small part of the total economy, the housing market and the 5% of the labor force that it employs is like the tail that wags the dog. Growth in construction employment went negative last year and is still negative at -4% (FRED Series USCONS). The last time it went negative was in the spring of 2007, six months before the 2007-2009 recession and financial crisis.

This trend is a powerful deflationary force that counteracts inflationary forces that might occur in the 2021 recovery. Understanding those deflationary forces and lacking the tools to combat deflation, the Fed is watchful but less concerned about inflation. One of the forces acting as a brake on inflation is our own expectations of inflation. At the hearing this week, Powell noted that those expectations have become anchored at low rates over the past two decades. During the 1970s, expectations were unanchored. People expected inflation to be as much as it was the past year or worse.

The anchoring process occurs slowly and changes slowly. People who are less than 50 have formed different expectations based on their life experience. Older Americans may still be suspicious, watchful for the least sign of a phenomenon that imprinted on them when they were younger. In the 1970s, people who would not think of stealing, stole gasoline from their neighbors to get to work. Neighbors in New York City beat each other up over their place in line to get gasoline. Retired people in subsidized housing froze to death because they couldn’t afford the skyrocketing costs of heating their home.

“Don’t go that way,” older Americans say. “That dog could bite you.” Younger Americans ask, “What dog?”

We make our journey through life avoiding that dog, the one that bit us. Our choices do not keep us safe from a dog biting us. What protects us from a dog bite is the choices of others, the ones that dog owners make to install fences or to keep their pet inside the house. We live in community with others; that makes our lives more convenient, but we are more vulnerable to the choices that others make. The pandemic has focused our attention on that fact, and those who have lived through this past year are imprinted.

////////////

Photo by Tillmann Hübner on Unsplash

January 31, 2021

by Steve Stofka

The trading in GameStop (GME) has spurred romantic visions; a mob of peasants has stormed the castle and the nobles have fled! Huzzah! This love of the romantic convinced a bunch of peasants to storm the Capitol on January 6th. We are human beings; we love stories. The truth is less appealing or ordinary.

At a press conferences this week, the well-prepared and even-tempered White House Press Secretary, Jen Psaki, was asked if President Biden planned to speak to the issue of the volatile trading in GameStop (GME). She said that it was a new age; the President was not going to speak to issues he had no expertise in. Imagine that. We will miss the enjoyment of watching former President Trump standing in the White House driveway and opining to reporters on every topic under the sun.

Reporter: “Mr. President, what’s your source on that?”

Mr. Trump: “My mind. I have a very smart mind.”

Without the daily source of ridicule that Mr. Trump provided, comedians are having to write new material.

But I digress. GameStop. Twenty-five years ago, internet stocks were taking off. Message boards at AOL, CompuServe and others lit up with stories of “Ten baggers,” the holy grail of stock investing. Buy a stock for a $1 and watch it rise to $10. Those in Bitcoin have experienced the heady feeling.

That romance incentivized peasants to join the Crusades; there was gold in Solomon’s Temple at Jerusalem. Thousands poured into the California gold fields in the hopes of striking it rich. The people who get rich are the ones selling pickaxes and panning tools to the miners. The gold is not in the hills but in the people digging up the hills.

On message boards in the 1990s we learned about options. Instead of buying Microsoft stock, an investor can buy options to buy Microsoft’s stock. If Microsoft’s stock is selling for $25, it costs $2500 to buy a 100 shares, the minimum lot. At that time, buying less than a 100 shares cost a lot more in commissions. If an option were selling for $1, an investor could buy 2500 options! If the price went up $5 you could quintuple your money. Imagine making $10,000 in a few weeks.

People quit their jobs to day trade. The successful ones were cautious, taking profits quickly, not taking too many risks. Someone with a family to feed and rent to pay must be responsible. A modestly successful trader can convince themselves that they have a well-balanced strategy.

About a year before the internet stock bubble blew up, someone posted a rather long post on a message board. Since he was in the options business, a family member had asked him for his advice. Aware for the first time that inexperienced retail traders were taking positions, he offered his advice, which I will paraphrase. A few points stuck with me.

Options are tools. 94% of options trades expire worthless. Professional traders use options like car insurance. Yes, there are some companies who take risks, but most of those in the business use options to mitigate risk.

Understand that multi-national companies pour hundreds of thousands of dollars into news gathering, sophisticated computers and programming by very smart people to develop and deploy options strategies. They are on the other side of the trade.

A retail trader may get lucky. The prospects for Company A improve, the stock goes up and the trader makes money. A company using options aims to make money whether the prospects for Company A improve or deteriorate. A successful racetrack makes money no matter what horse wins.

Gamblers at a racetrack can rush the window in the closing moments before a race begins and cause the track to lose money on that race because the track doesn’t have the time to change the odds to layoff the bets. With the advent of the internet, a group of retail options traders could do the same with a hedge fund, who can’t lay off the bets fast enough. It could be done but it would be difficult.

25 years later, it has become much easier for gamblers to rush the betting window. The success of those traders will no doubt inspire others to try the same strategy. An industry which uses options to mitigate risk on trillions of dollars will not let a few retail traders upset that market for long, so don’t gamble with the rent money.

/////////////