We grow comfortable with our theories, our hypotheses of the way the world works. They have an internal logic which appeals to us. We are reluctant to give up a theory when events challenge the validity of that theory. Eventually, events force us to abandon a theory even though there is no acceptable alternative which makes sense to us. So we adopt a mechanical model, a paradigm with no underlying rationale, which describes a progression of events but can not explain why it works the way it does.

A classical example of this descriptive mechanical model is the relationship of electricity and magnetism first noted in the early 19th century. Thought to be two different forces, a model was developed which defined a working and predictive relationship between the two but no one could fully understand why the relationship existed. It was not until later in the century that James Maxwell formulated a complete theory of electromagnetism, building on the work of Faraday, Hertz and Ampere.

Yesterday I examined the Starve the Beast theory, one which should work but fails to describe the relationship between tax rates and government spending at the Federal level. The theory works as long as the government entity does not have massive borrowing power, as the U.S. government does. At the state level, we do see a closer correlation between reducing revenues and lowered government spending.

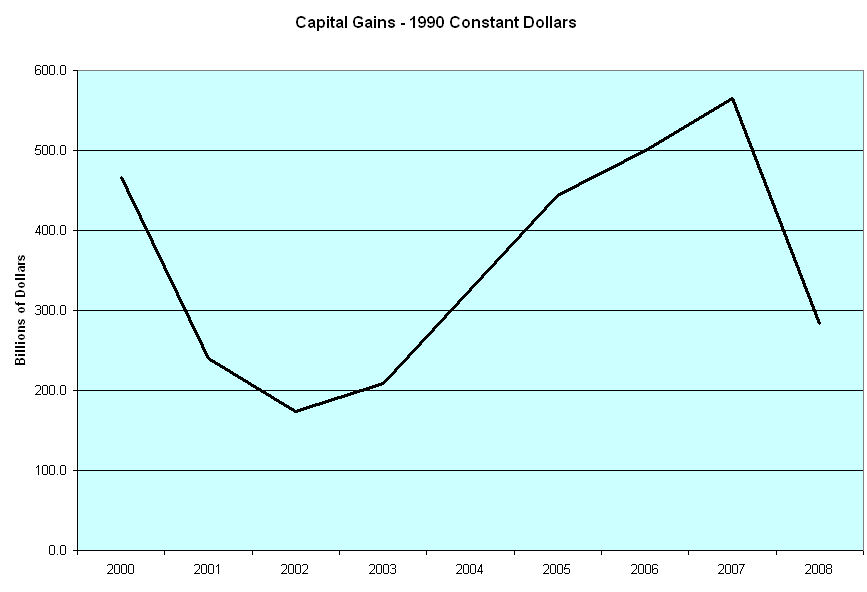

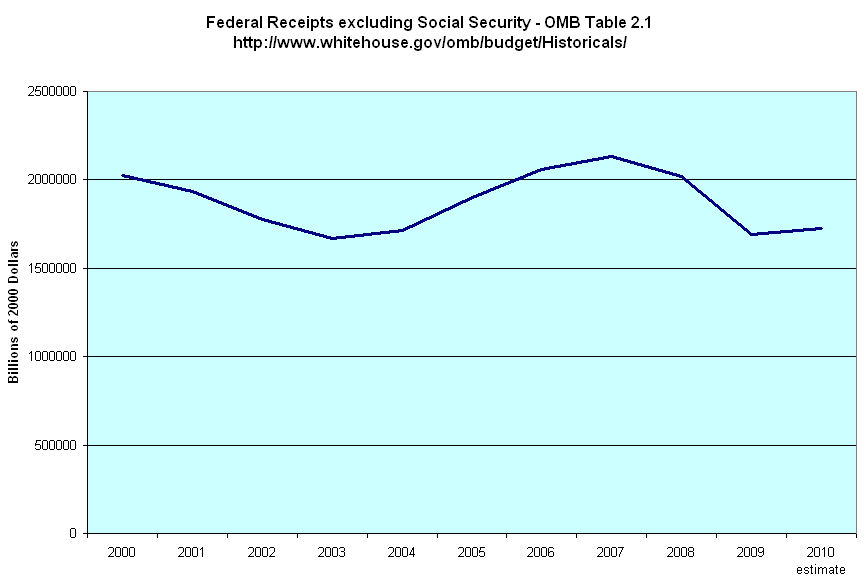

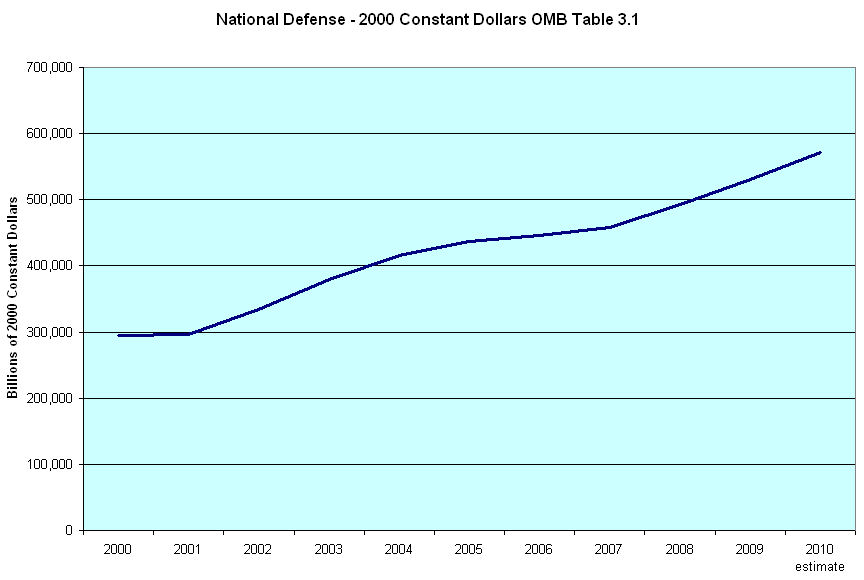

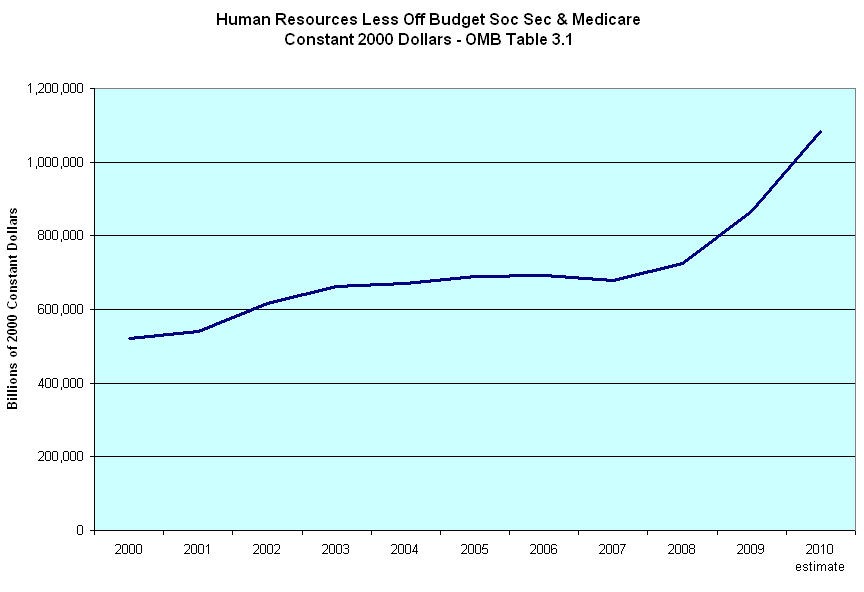

Another theory which should work is supply side economics, a model that predicts that lower marginal tax rates and less regulation will spur greater investment by businesses, the producers or suppliers of economic goods. Again, the internal logic of this model makes sense. Make it easier for people to produce and lower the tax on income from that production and people will invest more in production which will create more jobs and overall economic activity which will produce greater tax revenues to the government.. So, why haven’t income tax revenues (excluding dedicated social security taxes) over the past 30 years supported this model?

Keynesian macroeconomic theory focuses on management of the demand side of an economy through transfer payments, greater government consumption expenditures like building roads and other infrastructure projects. In the seventies, repeated economic crises, recessions and ultimately stagflation made it apparent that a focus on the demand side could not fully explain the dynamics of a country’s economy. Those who clung to Keynesian theory insisted, and continue to insist, that the theory is sound but that the implementation, i.e. management of demand, was poor.

In response to the perceived weaknesses in Keynesian theory, Arthur Laffer, Victor Canto and others developed a macroeconomic theory which focused on the supply side of the economy. Rather than manage demand, a government should manage incentives to produce, i.e. less regulation, and disincentives for those who made good income from that production, i.e. lower tax rates. As in physics, the “holy grail” of economics is to develop a unified theory that can incorporate both the supply and demand components of an economy with a predictive relationship between the two. I am not aware that anyone has developed such a theory. Unfortunately, this economic debate has become politicized, with Democrats taking the demand side of the argument and Republicans taking the supply side.

Recent history has deflated both theories yet proponents of each theory blames policy implementation or some other factor which invalidates the “experiment”, i.e. events, which cast doubt on their theory. On the demand side, economist Paul Krugman maintains that there was not enough stimulus, i.e. demand, pumped in by the government to fully test the Keynesian model. On the supply side, economist Art Laffer has blamed policies of taxation and income redistribution over the past 7 years which have reduced productivity. In a 2006 lecture, when the economy was riding high atop a housing boom, Laffer had not blame but glowing praise for both monetary and fiscal policy.

We cling to our familiar theories as though they were family and regard any criticism of a cherished theory as a personal attack. They form the foundation of our policies of government. As a nation we alter tax policy, we adjust interest rates, we bail out, we buy more Treasury bonds and get frustrated as neither the demand or supply sides of the economy responds forcefully to our efforts. We blame those who don’t agree with our chosen theory, we criticize those who did not implement it properly or adulterated it with compromise.

The lesson we find hard to learn: don’t fall in love with a theory.