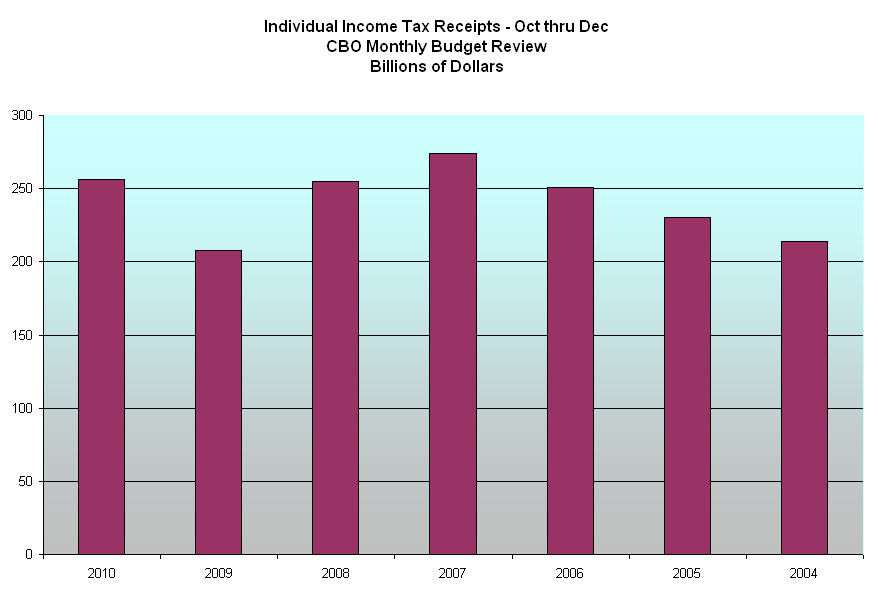

The Adam Smith Institute Blog at the Christian Science Monitor carried a financial story about pensions in Hungary that had several misconceptions. The Christian Science Monitor, while noted for its reporting in other areas, is not a financial publication. The Washington Examiner then linked to this blog and it went around the internet as a case of “European countries taking private pensions”. If this were the case, I knew I would find the story as a prominent feature in the Financial Times, the leading source of financial news in Europe, or in the Wall St. Journal, the leading source of financial news on this side of the Atlantic. If this were true, then this is pretty big news to the bond market.

At a Wall St. Journal blog, a reporter gave a more complete description of the transition which Hungary is planning. Here is an excerpt. Emphasis added by me.

Hungarians will have until Jan. 31, 2011, to decide whether they opt to return fully to the state’s pay-as-you-go pension regime. Only the private pension fund members who wish to remain in their respective pension funds will need to express their wish. Those who don’t do that will automatically return to the state scheme.

“They have two options: they either stay or decide to return, [and] both decisions have their consequences,” [Economy Minister Gyorgy] Matolcsy said at a press conference in parliament after a government meeting.

The assets of those who decide to return to the state scheme will be kept in individual accounts and will remain inheritable by the spouse, Mr. Matolcsy said.

Hungary has a hybrid social security scheme similar to what George Bush proposed about 6 years ago. Designed to encourage people to save for retirement, some of each person’s social security taxes could be invested in private pension funds. The private pension fund is supposed to generate a return that will provide 30% of a retirees pension payment (Social Security check, in the U.S.) and Hungary supplies 70% of the pension payment. Here’s the kernel of this story: Hungary had promised to make up or “top off” a retiree’s pension, i.e. pay more than 70%, if the retirees private plan had not made the returns necessary to supply 30% of the full scheduled monthly pension payment the retiree was due. Hungary can no longer promise to “top up” pension payments above the 70%. What happened?

Hungary has a large debt load. It can borrow private pension money that a retiree chooses to turn over to the state at a net effective rate that is less than the bond market charges for Hungary’s debt. The U.S. government borrows Social Security money at about 3 – 4%, a rate less than what the bond market usually (except for the past few years) charges the U.S. for its medium to long term debt.

Secondly, people close to or in retirement in Hungary took on more risk than they should have. Many private pension funds lost value during the past two years and could not meet the 30% portion of the scheduled pension payment. In a difficult economic environment, Hungary found itself “topping up” more and more private pensions.

According to the Financial Times, France and Ireland are shifting state pension assets away from stocks and into government debt and cash. Estonia, a prudently managed nation with no debt, has even considered reducing state contributions to private pension plans.

The question for developed countries with hybrid pension, or Social Security, schemes is how to design a system that encourages people to save for retirement but encourages prudent financial management. If I were a Hungarian citizen and my government said they would make up any shortfall in the returns of my private pension funds, I would have rolled the dice and invested in riskier stocks that would hopefully generate big returns for me. How could I lose when the government has promised they would make up the difference? Then, whoops, the financial crisis hit and Hungary found that their hybrid pension system had inadvertently rewarded risky behavior.

If I were a Hungarian citizen nearing or in retirement, I would be angry, of course. The government had promised me that I could have my cake and eat it too and I like fairy tales and vote for the politicians who tell those tall tales.