A few weeks ago, I wrote about a long term trading strategy using the 200 day moving average of a popular index, the S&P500, which captures 75% of the corporate activity in the U.S. As corporate profits of larger companies increasingly come from overseas, the S&P provides some foreign stock exposure as well. Over the past decade, the strategy worked pretty well, getting out of the market before the 2008 downturn, enabling an investor to pick up shares at a cheaper price in 2009. That is, after all, the point of adopting any type of trading strategy – sell when shares are expensive, buy them back when they are cheap.

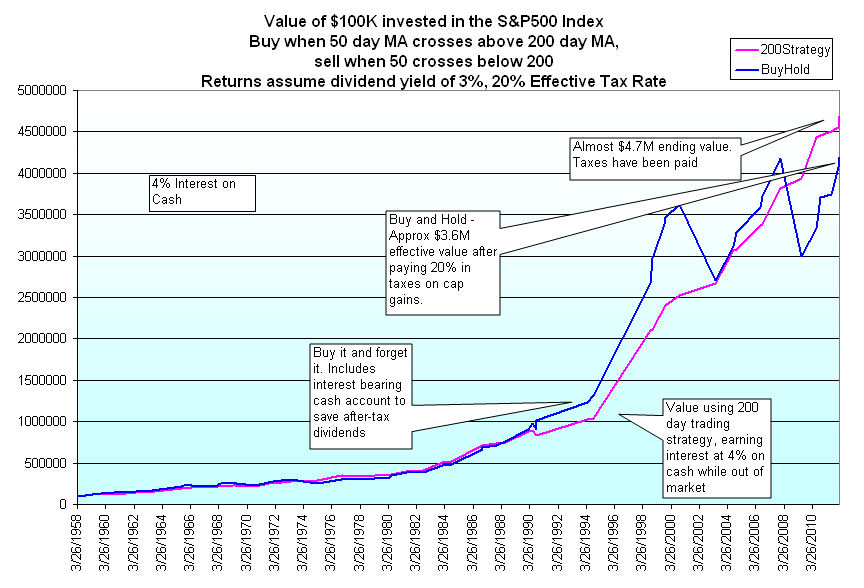

Today, I’ll look at a variation of the 200 day strategy called the “Golden Cross”, which I have mentioned in a few past blogs. A Golden Cross buy signal occurs when the 50 day moving average crosses above the 200 day moving average. A sell signal occurs when the 50 day average crosses below the 200 day average. A buy signal just occurred at the end of January. You can chart the S&P index for free at StockCharts. I will compare this Golden Cross strategy to the buy and hold strategy.

The Golden Cross strategy investor must overcome two major problems: tax attrition and the return on cash while out of the market. The first problem is formidable. The IRS takes their pound of flesh out of profits that the trading strategy produces. The downturn in prices when the strategy is out of the market may not be enough to compensate for the 20% (or more?) tax bite, which reduces the investor’s capital pool when he buys back into the market. Thus the investor may buy fewer shares on the next buy date, and those fewer shares generate less profits as market prices climb. The second problem is almost as formidable. Over the 50 years that I will explore, the investor would be out of the market about a third of the time. The interest rate one earns on one’s capital while out of the market is an important factor in total returns.

Here are the assumptions of the study:

20% Effective Tax Rate – capital gains taxes are “taken out” at the time of the sale.

3% Average Dividend Yield (see here for historic dividend yields)- dividends are recorded and taxes paid for those dividends for both strategies at buy and hold dates. While not entirely accurate, it largely accounts for the value of dividends to a portfolio.

Interest – 4% on cash while out of the market.

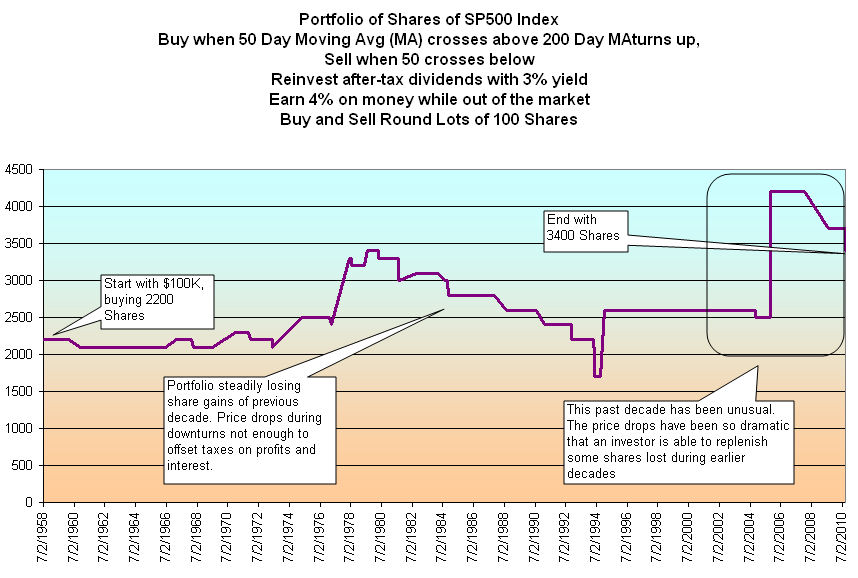

Reinvest – For the conservative buy and hold strategy, the investor pays taxes on the dividends received and puts the money in some cash equivalent fund earning the stipulated interest. The Golden Cross strategy accumulates and reinvests the dividends at the next stock purchase date. (Click to enlarge in separate tab)

The market downturn during the 70s was severe enough that the Golden Cross investor could book profits, pay taxes and buy back more shares than he had before. In the early 80s, the downturns were not significant enough to overcome tax attrition. Had we ended this exploration in the year 2000, this strategy would have done poorly when compared to a buy and hold strategy, even after accounting for the deferred taxes owed by the buy and hold investor. During the two severe bear markets of the 2000s, the Golden Cross strategy shined, exceeding the returns of the buy and hold strategy.

The lesson is that the downturn must be strong enough that the Golden Cross strategy can overcome the tax attrition by buying shares back at greatly reduced prices. Although the Golden Cross strategy produced only 5 losses out of 27 round trip (buy/sell) trades, a winning percentage of about 80%, the tax obstacle is a formidable barrier to increased profits over buy and hold. The buy and hold strategy is about 25% invested in cash at the end of this study, a conservative approach consistent with a buy and hold investor. If the buy and hold investor were to periodically reinvest dividends instead of holding cash, it would probably equal the after tax returns of the Golden Cross strategy.

The Golden Cross strategy is much more dependent on finding a good return on cash when the investor is out of the market. In these times, that is not an easy task. As a retirement strategy, it might be wise to choose a combination of the Golden Cross and buy and hold. A buy and hold investor in or approaching retirement would assess their income needs for the next 3 – 5 years and sell just enough shares to fill the cash account when a Golden Cross sell signal arrives. During their working years, a buy and hold investor would add shares when a Golden Cross buy signal arrived.