To be respected, authority has got to be respectable. – Tom Robbins

September 9, 2018

by Steve Stofka

Most nations create their own money, a super power of the modern state. The politicians and central bankers of each country have the responsibility to maintain the reputation of its money. Each nation is both the creator and net seller of its money, able to lower but not raise its comparative value. To raise that value, each nation depends on others to be net buyers of its money.

Nations carefully study the behavior of each other’s central banks. Argentina cut interest rates in January 2018 even though the country was experiencing high inflation. This action was the opposite of good central banker behavior, and hurt the reputation of the Argentine peso, which has lost half its value since January. Money traders suspected that the Argentine central bank had become captive to political control. Few trusted a politician with money super powers.

The reputation of a nation’s money rests on the steadiness of its tax revenues. As I have noted before, revenue from the sale of nationalized resources acts as a tax. Those commodity revenues do not build a money’s reputation as much as the tax revenues from the economic production of a nation’s people and businesses.

A nation can print its own money at little cost. A greater supply of anything, given a constant demand, lowers the price of that thing. The real cost of printing money is borne by the nation’s people and businesses who use that money for daily exchange. As a money’s value declines, that loss of value acts as a sales tax on each money unit exchanged. Let’s call that the king’s tax. This undeclared tax revenue does not build a money’s reputation.

A nation supports the reputation of its money by using its super powers with restraint. When a nation receives most of its tax revenues from its own internal production, that is a sign of a healthy economy, with a reasonable monetary and fiscal policy. When the king’s tax (inflation) and commodity resource revenues exceed half of a nation’s revenue, the value of its money becomes like two day old bread.

A nation’s money rises in reputation when it is bought, and there are two reasons for buying a nation’s money: 1) buying goods and services from that nation, and 2) loaning money to the governments and businesses of that nation. In 2017, China, the United States and Germany were the top exporters, putting their currencies in demand (Note #2). Loans to borrowers in emerging markets are often priced in U.S. dollars, the current reserve money of the world. If the money in that nation loses its value against the dollar, the borrowers effectively pay a king’s tax as they make their loan payments (Note #1). Typically, a nation will blame the tax on rapacious money dealers.

A nation’s money reputation relies on several factors that a nation can control: inflation, tax revenue and the source of that revenue. A nation is judged on its current and historical behavior with money and debt. Its political structure and the independence of its central bank are important factors as well. On an international stage, its money must compete with other nations in all these categories. Call it the daily beauty contest – no swimsuits.

///////////////////////////////

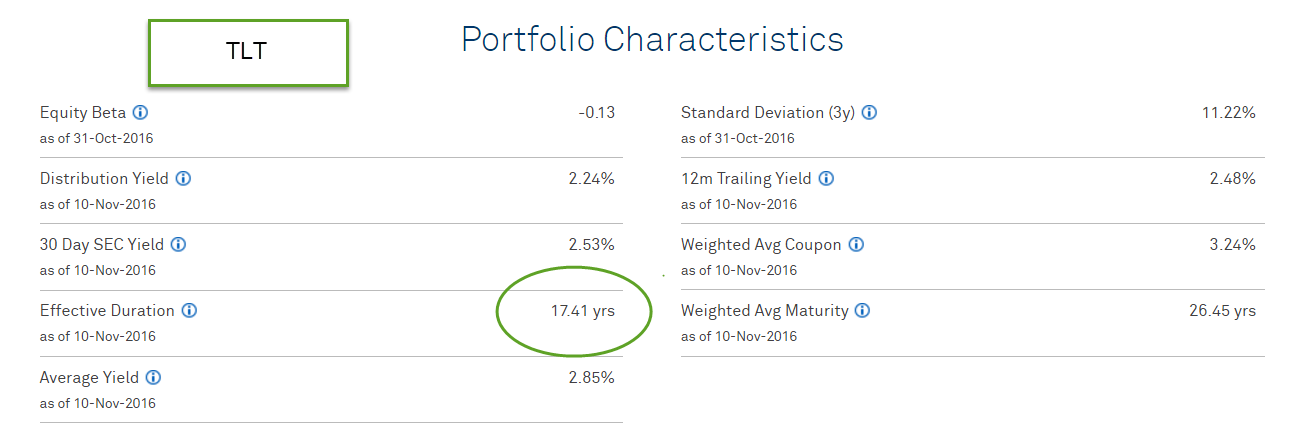

1. EMB is a basket of emerging market debt priced in USD (http://etfdb.com/etf/EMB/). It is off 5% from its high at the beginning of the year and pays a dividend of 4.6%. Its annual return for the past ten years was 6.5%, the same as a long Treasury ETF like TLT. A broad bond index fund like Vanguard’s BND earned 3.8%.

2. Germany uses the Euro, not its own national currency. In 2017, China exported $2.35 trillion, the U.S. $1.55T and Germany $1.45T. Visual Capitalist picture graph. The site is a picture book for curious minds. Here’s one on the biggest employer in each state. For southern states, the answer is Wal-Mart. Universities and health care systems are prominent employers in many states.

Related: The U.S. owes $6.2 trillion to the rest of the world. China’s share of that debt is $1.8 trillion. The U.S. holds $125 billion in foreign reserves, similar to the amount Turkey holds. As the world’s reserve money, the U.S. holds enough foreign reserves to counter any distortions in currency markets.

/////////////////////////////

Miscellaneous

In a survey of 5000 workers, Gallup found that only 51% had a single full-time job. 36% were gig workers.

Since 1991, real purchase only house prices have gone up 1.7% annually. FRED series HPIPONM226S / PCEPI, index 3/1991 = 100. Real rents and owner equivalent rent (OER) nationally have gone up 8/10ths percent annually. This is about half the rate of home price growth. Urban residents must pay an extra price. In Denver, rental prices have gone up 1.9% annually since 1991. OER has risen 1.7% annually. No doubt, California cities have even higher annual growth rates than national averages. Owner Equivalent Rent is a BLS-calculated rent that a homeowner pays themselves for use of the residence. This includes mortgage, repair and maintenance costs on the home.