November 1, 2015

Today is the day that U.S. readers fall back. Let’s hope it’s the only thing that falls back!

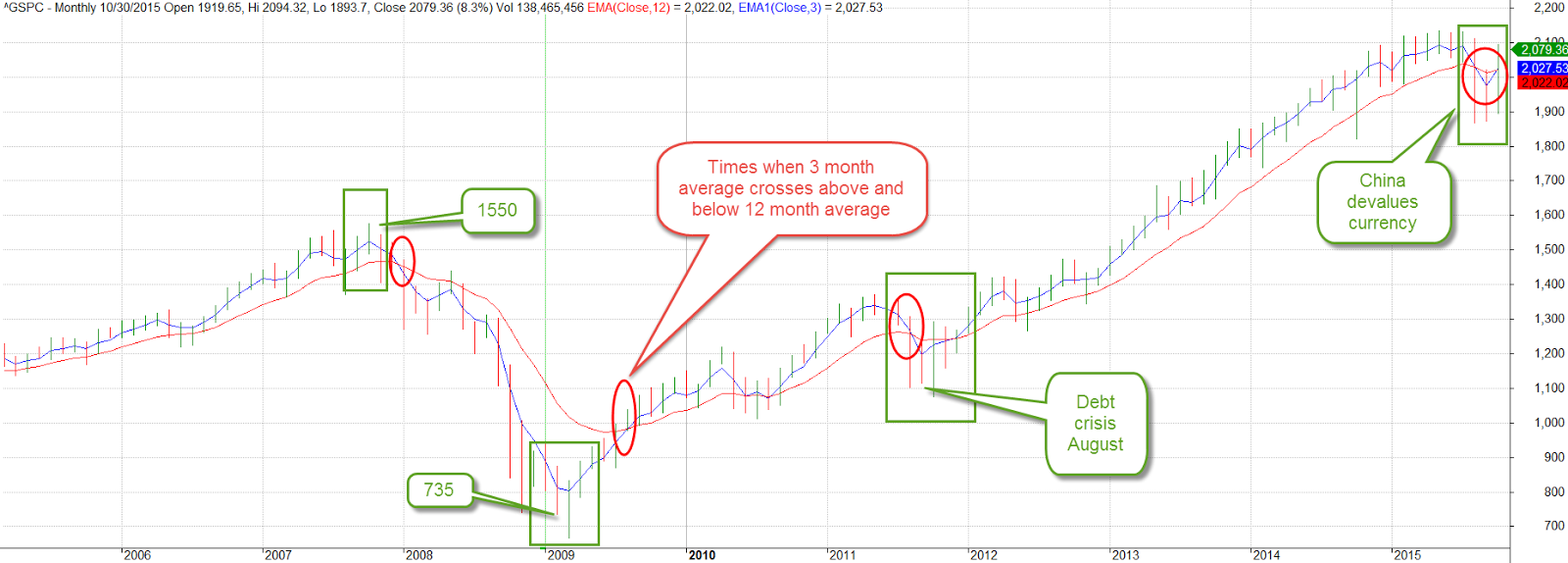

Eight years ago, in October 2007, the SP500 index reached a pre-recession high of 1550. After this month’s 8% recovery the index stands at 2079, more than a third above that long ago high. A decade long chart of the SP500 shows the inflection points of sentiment. We can compare two averages to understand the shifts in investor confidence. A three month average, one quarter of a year, captures short term concerns and hesitations. A one year average reflects doubts or optimisms that have strengthened over time. The crossing of one average above or below the other gives us a signal that a change may be coming. Concerns may be temporary – or not.

After falling below the 12 month average, the 3 month average strained and groaned to pull its chin above that long average, notching five consecutive weekly gains. Both China and the EU central banks have announced plans for lower interest rates or QE to spur their economies. Oil prices continued to bounce around under the $50 mark. OPEC suppliers announced they could not agree on production cuts. Fearing a continuing oversupply of crude, oil prices fell 4 – 5%. Then came the news that the number of oil rigs in the U.S. had fallen. Prices went back up.

Commodities and mining stocks remain under pressure. After falling over 18% in September, mining stocks gained back most of those losses in the first two weeks of October, then fell back in the last half of this month, closing the month with a 3% gain. 15 to 20% gains and losses in a sector during a month looks like so much scurrying and confusion.

Emerging market indexes lost ground this past week, slipping more than 4%. Worries of a global recession continue to haunt various markets. For large and medium U.S. companies, a slowdown in European and Asian markets is sure to have a negative effect on the bottom line.

The first estimate of 3rd quarter GDP growth was a paltry 1.5%, far below the 3.9% annual rate of the 2nd quarter. Two-thirds of the SP500 companies have reported earnings for the 3rd quarter and FactSet estimates a decline of 2.2% for the quarter, the second consecutive quarter of earnings declines.

***********************

The Causes of Depression

The economic kind, not the emotional and psychological variety. Economics history buffs will enjoy David Stockman’s critique of the extraordinary amount of monetary easing under former Fed chairman Ben Bernanke. As President Reagan’s budget director, Stockman was at the forefront of supply side economics, a theory which promised an answer to the stagflation of the 1970s that drove many to question the assumptions and conclusions of Keynesian economics.

At first a champion of this new approach to economic policy making, Stockman grew disillusioned and later coined the term “voodoo economics” to describe the contradictory thinking of his boss and others in the Republican Party who stuck by their beliefs in supply side economics in spite of the evidence that these policies generated large budget deficits and erratic economic cycles.

In 2010, Stockman penned an editorial that held some in the Republican Party, his party, culpable for the 2008 fiscal crisis. He understands that politicians and policy makers become welded to their ideological platforms, disregarding any input that might upset their model of the world.

For those who have a bit of time, an Atlantic magazine December 1981 an article acquainted readers with David Stockman in his first year as budget director. The budget process seems as broken today as it was 35 years ago when Stockman assumed the task of constructing a Federal budget.

These “internal mysteries” of the budget process were not dwelt upon by either side, for there was no point in confusing the clear lines of political debate with a much deeper and unanswerable question: Does anyone truly understand, much less control, the dynamics of the federal budget intertwined with the mysteries of the national economy?

Stockman understands the political gamesmanship that permeates Washington. He criticizes Bernanke’s analysis of the 2008 Great Recession as well as the 1930s Great Depression. Faulty analysis produces faulty remedies. Stockman goes still further, finding fault with Milton Friedman’s monetary analysis of the causes of the Great Depression. In a 1963 study titled A Monetary History of the United States Friedman and co-author Anna Schwartz found that monetary actions by the Federal Reserve deepened and lengthened the 1930s Depression. Friedman became the leading spokesman of monetarism in the late 20th century, the thinking that governments can more effectively guide a national economy by adjusting the money supply rather than employing an ever changing regime of fiscal policies.

Students of the great debate of the past 100 years – bottom up or top down? – will enjoy Stockman’s take on the matter.