December 19, 2015

For those of you who pay attention to crossing averages, the 50 day average of the SP500 index just crossed above the 200 day average. This long term buy signal is often referred to as the Golden Cross. The Death Cross, when the 50 crossed below the 200 day average in early August, is a sell signal. Those who sold some of their holdings at that time missed the volatility of the past few months. The index was at 2100 in early August. It closed at approximately 2000 on Friday. The index has lost about 4% in the past two days.

Past buy crosses were June 2009, October 2010, January and August 2012 and this past week. Recent sell crosses were December 2007, July 2010, August 2011, July 2012, and August 2015.

In buy, sell order they were December 2007 (sell), June 2009 (buy), July 2010 (sell), October 2010 (buy), August 2011 (sell), January 2012 (buy), July 2012 (sell), August 2012 (buy), August 2015 (sell) and December 2015 (buy). Note the three year period between buy and sell signals from August 2012 to August 2015. The market gained 55% during that period.

As you can see from the list above, the market usually regains its footing after a few months – except when it doesn’t, as in 2008. This buy sell rule avoided the protracted market downturns in 2000 and 2008 at the expense of acting on signals that are false positives, or what is known in statistics as Type I errors.

*****************************

Cost Basis

Mutual fund companies typically calculate an investor’s cost basis for their funds. Some investors mistakenly think that cost basis reflects the performance of their investment. It doesn’t. Let’s look at an example of a cost basis entry:

At first glance, an investor might think they have lost $186 since they first started investing in the fund. Usually, that’s not the case. In this case, the fund has earned more than $5000 in ten years.

Let’s look at some basics. An investor in a mutual fund has the option of having dividends and capital gains reinvested in the same fund or transferred to another fund like a money market. To begin our simple example, let’s choose to NOT reinvest.

Let’s say an investor put $1000 in a bond fund BONDX. Each share sells for $100 so they have bought 10 shares. Every quarter the fund pays a $1 dividend per share. A day before the dividend is paid the fund’s share price is $101. The fund then distributes the $1 dividend. The market value of each share instantly falls by the amount of the dividend – $1 – so that after the dividend the market value of each share of BONDX is $100. What is the investor’s cost basis? $1000. The market value is 10 shares x $100 = $1000. Capital gain or loss? $0. Does this mean the investor has made no money? No, they have an extra 10 shares x $1 dividend per share = $10 in their money market account.

When opening up a fund the default option may be to reinvest capital gains and dividends. This is where some investors get confused. So, let’s change the reinvest option and choose YES. Now, as before, the fund distributes the $1 dividend and the share price of the fund falls to $100, just as before. Now, however, the money is not transferred to the money market fund. Instead it is used to buy more shares of BONDX. The $10 that the investor receives buy a 1/10 share of BONDX. Now the investor owns 10.1 shares of BONDX at a cost of $100 per share = $1010 cost basis. The market price of the fund is $100 per share x 10.1 shares = $1010. Captial gain or loss: $0. Again, the capital gain or loss does not reflect the total performance, or profit and loss, of the investment. The profit is $10.

So, the capital gain or loss should be used only to calculate the tax effect of selling a fund, not the performance of the fund. The fund company will calculate the performance, or the rate of return (IRR) on an investor’s funds on a separate screen. Choose that option instead of the cost basis screen.

******************************

The Investment Cycle

Investments tend to rise and fall in price over the course of a business cycle. At the end of an expansionary cycle, commodity prices start falling. Yardeni Research has some good graphs which illustrate the ongoing plunge in commodity prices.

As the economy begins its contraction phase, the prices of bonds start to fall. As we enter recession or at least a contraction of growth, stocks fall. In the recovery, comodities rise first, followed by bonds, then stocks. Here is more information for readers who are interested in exploring the details and background of this cycle.

***************************

Diabetes

The American Diabetes Assn puts the direct costs of treating diabetes at $150 billion. That is 25% of the $600 billion spent on Medicare in 2014. Indirect costs add another $75 billion in costs. Much of the increased expenditure is for treating late onset Type II diabetes. Expenses are sure to grow as the population ages and people do not make the life style changes needed to delay or moderate the onset of the disease.

***************************

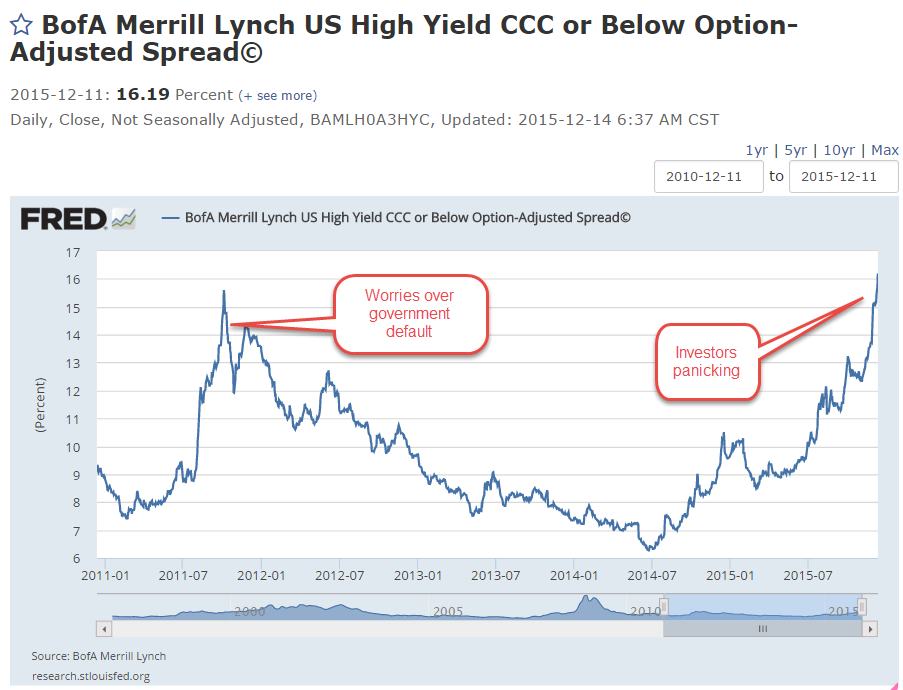

Credit Spreads

Several weeks ago, I noted the growing “spread” between Treasury bonds and high yield junk bonds. The graph I showed was the benchmark of junk bonds, the Master II class. Let’s call them Bench Junks. The bottom of the barrel, so to speak, are those company bonds rated CCC and lower. These are companies that are more likely to default as economic growth slows or contracts. Let’s call them Low Junks. While the Bench Junks’ spread shows investor concern, the Low Junks’ spread shows a stampede out of these riskier bonds. A rising spread means that the prices for those bonds are falling, effectively giving buyers a higher interest rate. Investors want the higher yield to compensate them for the higher risk of owning the bonds.

Here is an article explaining the composition of some high yield bond ETFs for those readers who are interested. in learning more.

**************************

Income Taxes

Turbo Tax may be the most widely used individual income tax software but there are many providers of tax software. Each state usually lists the software programs it has approved. You can Google “approved income tax software” and insert your state name at the beginning of the search term. Here is a link to Colorado‘s list of approved software. Here is the list for Texas, New York and California.