December 4, 2022

by Stephen Stofka

This week’s letter is about the effect of wages on inflation. In an address this week, Fed (2022) chair Jerome Powell explained the Fed’s view of the latest trends and signaled that the Fed might ease up slightly on a rate increase at its December 13-14th meeting. Friday’s jobs report had stronger than expected gains so that may temper the Fed’s willingness to ease up on the “rate brake.” In his speech, Powell cautioned that “nominal wages have been growing at a pace well above what would be consistent with 2 percent inflation over time.”

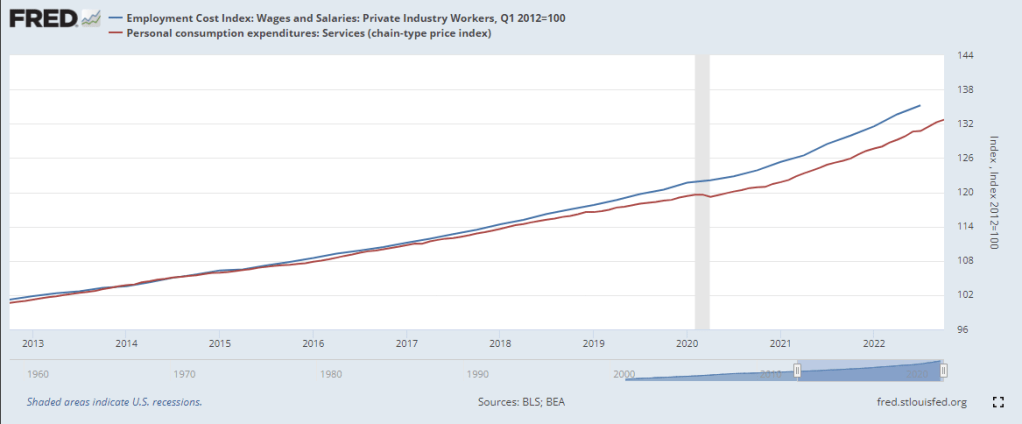

The services portion of the economy consists of mostly labor so the Fed focuses on just that sector to gauge the underlying demand for labor. In the graph below are total wages and salaries (blue line) and the services sector (red line). Both series bent upward from their pre-pandemic trends but the Fed is focused on the upward momentum of wage increases (blue line) as an underlying driver of “core” inflation.

Core inflation does not include volatile food and energy prices. Those matter a great deal to consumers but the variance makes it more difficult to predict a future price path. Imagine walking a dog on a leash down a park path. The dog might dart from side to side to sample the smells along the path but the walker stays more centered on the path. An observer who could not see the path would likely watch the person rather than the dog to predict the direction they were taking. Below is a chart from Powell’s presentation.

On a long-term basis there are two trends that are likely to produce upward wage pressures. Growth in the working age population has slowed and the participation rate has declined. Since the beginning of 2021, wages have increased 11%. The labor force has increased only 3%, partly due to demographics and partly due to a participation rate that is 1% less than the pre-pandemic level. Should the trend continue, it will affect the supply of workers, causing employers to compete by paying higher wages or give up and abandon expansion plans. The first leads to persistent inflation. The second leads to a recession.

While the Fed might moderate their rate increases, history has warned not to ease up on rate increases at the first sign of slowing inflation. In the early and late 1970s, the Fed eased and inflation resumed its upward climb. It’s like relaxing the tension on a leash and the dog immediately rushes ahead. The Fed’s tools are blunt instruments, relatively easy to deploy, but lack any surgical precision. Increasing rates dampen inflation, but both have the hardest impact on low income families who will welcome the relief of lower inflation. They can expect little help from a divided Congress as it struggles to enact any fiscal policy.

I worry about the next two years. Republicans have been out of power for a century. By that I mean that voters rarely given them the full reins of power, a trifecta where the same party controls the Presidency, the Senate and the House. They held power in the 83rd Congress from 1953-1955 and again in the two years of the 115th Congress, from 2017-2019. Their longest stint was the four years 2003-2007, a time of repeated failure and scandal – the mismanagement of the Iraq war, Hurricane Katrina, the accounting and energy scandals. They are not a party that governs well because they do not respect governing, only the political power that accompanies governing. They have become a reactionary party whose strategy is a “Lost Cause” narrative familiar to the southern Democrats they absorbed into the party over the past five decades. Party leaders and conservative talk show hosts echo a constant refrain that Republicans are the last standing guardians of traditional American values. I worry because Republicans are a party who breaks things and people are more breakable in the aftermath of the pandemic.

/////////////////

Photo by Justin Lawrence on Unsplash

Federal Reserve. (2022, November 30). Speech by chair Powell on inflation and the labor market. Board of Governors of the Federal Reserve System. Retrieved December 3, 2022, from https://www.federalreserve.gov/newsevents/speech/powell20221130a.htm

U.S. Bureau of Labor Statistics, Employment Cost Index: Wages and Salaries: Private Industry Workers [ECIWAG], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/ECIWAG, December 2, 2022.

U.S. Bureau of Economic Analysis, Personal consumption expenditures: Services (chain-type price index) [DSERRG3M086SBEA], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/DSERRG3M086SBEA, December 2, 2022.

///////////////////////