May 7, 2023

by Stephen Stofka

This week’s letter is about expectations – how we form them and why they are essential to our survival. This is a broad topic that encompasses several disciplines, from psychology to neuroscience and economics. Each field of study informs those in associated fields so the debate in economics is enriched by discoveries and theories in these other fields. I can only touch on a few aspects as I introduce yet another complication that might resolve some of the contradictions between theory and data.

We gain the ability to form expectations at an early age. Infants less than one year old learn what is called object persistence. If a toy falls out of their crib, they look over the edge to the floor below to see where the toy went. But object persistence is a primitive form of expectation. True expectation is a weighting of possibilities based on some criteria.

Instinctual responses often involve a primary measure of threat or satisfaction. We see this if we walk by a squirrel near a tree. If we are across the street, the squirrel may pause, poised to flee. If we draw nearer, the squirrel runs to the safety of the trunk as we approach. How far up the tree the squirrel goes depends on the distance we are from the squirrel. It would like to keep us in sight but if we get uncomfortably close, the squirrel must choose. It can hide on the side of the trunk opposite to our approach but it loses sight of us. It can go further up the tree, keeping us in sight and staying out of reach. That is a short term expectation formed in response to an immediate threat or stimulus. It is an instinctual rather than a rational expectation, the kind that economists consider.

Rational expectations are formed about the environments that produce events, or data samples, more so than the events themselves. For more than sixty years economists have been debating whether consumers have enough data and patience to construct a rational expectation. Richard Curtin (2022) reviewed the history of this debate as he argued for a theory that embraces both reason and passion as inseparable components of human decision making. In 1959, Herbert Simon protested that inadequate data does not invalidate the idea that consumers are trying to make decisions that improve their satisfaction – that’s the rational part – within the bounds of the data available to them. Simon called this bounded rationality. A few decades later Daniel Kahneman and Amos Tversky explored the biases in our decision making and their work became the foundation of behavioral economics.

Survey data reveals that consumers’ expectations of inflation overestimate actual inflation, according to Henry et al. (2023), economists at the Richmond branch of the Federal Reserve. The basis for that assertion is the University of Michigan (2023) survey of inflation expectations. The inaccuracy is fairly consistent and persistent, meaning that consumers are slow to correct their expectations as new data is released. Richard Curtin (2022) notes that as many as 40% of consumers are not aware of recent government data releases on the inflation rate, the unemployment rate and the growth rate of GDP.

Consumers cannot survive if they consistently and persistently form inaccurate expectations. There is an alternative explanation: economists and consumers are measuring two different things. Economists form their inflation expectations by measuring changes in the prices of goods and services. Consumers form their expectations in part by estimating their loss of purchasing power, their ability to satisfy their wants and needs. If consumers feel that their income gains are not keeping up with the change in prices, they may raise their estimate of future inflation.

The prices of frequently purchased items like food and energy guide our expectations of changes to our purchasing power. Our purchases of food and energy don’t respond quickly to changes in our income. In economist speak, these items are price inelastic. We still need to drive to work and eat. Secondly, we buy food and gas frequently so our expectations of future prices depends on an averaging of the most recent prices and the last purchase we made. It is unlikely that we will form an expectation of next year’s gas prices based on a ten year average of gas prices. Thirdly, energy prices are quite volatile. I might buy gas as frequently as I go to the movies if I like movies but the price of a movie ticket does not vary as much as the price of gas. To summarize, our expectations of inflation are guided by frequency, recency and volatility.

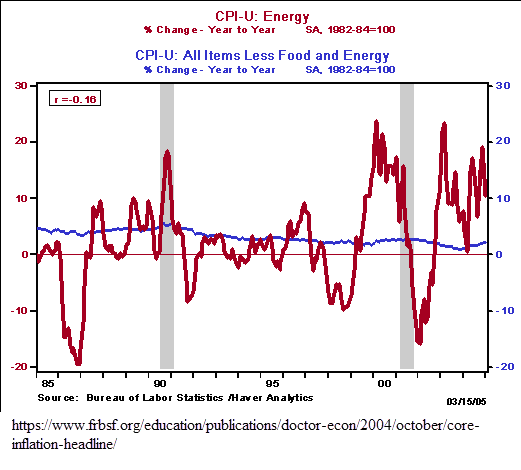

Energy prices are particularly volatile. In this 2004 article the Federal Reserve graphed the annual changes in energy prices (red) and the broad CPI price index (blue). The difference is startling.

The wild swings in energy prices are noise. Because of that volatility, the Bureau of Labor Statistics excludes food and energy items when it computes an index of core inflation. Core inflation is the inflation signal that economists use to predict next year’s prices.

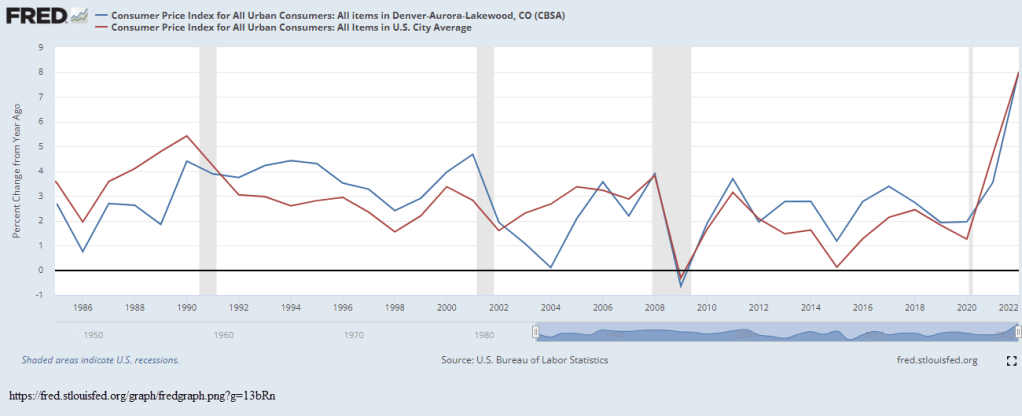

Consumer expectations of inflation include estimates of changes to their personal utility. As Richard Curtin (2022) has noted, it is not practical or possible to measure inflation at such a personalized level so economists average consumer expectations across the entire country. They collect price data at a broad metro area, or MSA. These urban areas can vary a lot from national inflation averages. In the chart below is a comparison of inflation in the Denver metro area and the nation as a whole. Rarely do the two series move together. When economists compile such a variety of consumer expectations into one national average, that average is less likely to accurately reflect individual or sub-regional expectations.

So economists are measuring changes in prices and consumers are estimating the change in their purchasing power. In his General Theory Keynes referred to the marginal efficiency of capital and the animal spirits of investor expectations of that efficiency that could be measured by the direction of market prices. Using that as a template, consumers’ purchasing power would be the marginal efficiency of income. We can gauge the animal spirits of consumers by the direction of total consumer purchases, which are continuing to outpace inflation. That is the best indicator of purchasing power expectations.

/////////////////////

Photo by Rodion Kutsaiev on Unsplash

Curtin, R. T. (2022, September 5). A new theory of expectations – Journal of Business Cycle Research. SpringerLink. Retrieved May 5, 2023, from https://link.springer.com/article/10.1007/s41549-022-00074-w

Henry, E., Mulloy, C., & Sarte, P.-D. G. (2023, January). What survey measures of inflation Expectations Tell us. Federal Reserve Bank of Richmond. Retrieved May 5, 2023, from https://www.richmondfed.org/publications/research/economic_brief/2023/eb_23-03#:~:text=Conclusion,inflation%20every%20month%20since%202012

University of Michigan, University of Michigan: Inflation Expectation [MICH], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/MICH, May 4, 2023.

{kind=link}