August 16, 2015

The big news this week was China’s decision to devalue its currency, the yuan, by 3.5% in two days. At week’s end, the yuan was about 3% less than what it was at the start of the week.

The decline in value came abruptly in a market that moves in hundredths of a percent, called basis points, each day. Since the beginning of the year, the euro has lost more than 8% against the dollar but it has done so in little teeny tiny moves.

What prompted China’s central bank to make this devaluation? China expected a small drop in exports in July, but 8% was far more than expected. (Bloomberg ) The timing of the devaluation couldn’t be worse. Emerging markets in southeast Asia have had sluggish growth in the past year and depend on exports. The devaluation of the Yuan makes Chinese exports more competitive. Vietnam and Malaysia devalued their currencies this week to maintain a competitive edge with China.

Emerging markets have had a rough ride this year. A popular Vanguard Emerging Markets ETF is down 18% from its high in April. However, today’s price level is barely below the price in mid-December.

While the SP500 has gone nowhere for the past nine months, emerging markets went on a tear in the beginning of the year, rising about 20% before falling back. Talking about the SP500…

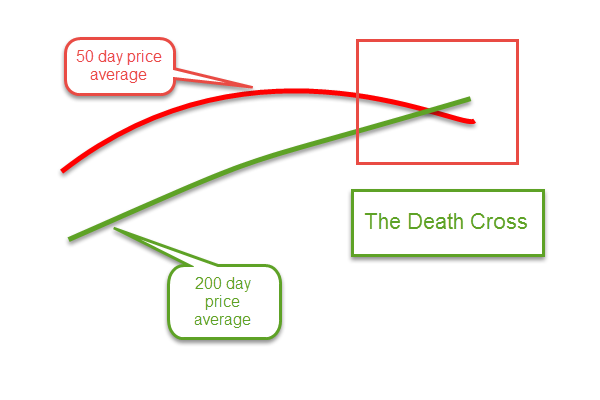

Dow Jones Death Cross alert!!! This past week the 50 day moving average of the Dow Jones Index crossed below the 200 day average. The sky is falling. Run for the hills. The rhetoric does get a bit dramatic. Should an investor disregard this signal as so much hocus-pocus? Brett Arends at MarketWatch suggests that this “indicator” is hogwash. Yes and no. The Dow Jones is a narrow index composed of just 30 stocks (CNN Money on component performance YTD). Although it is meant to capture the essentials of the U.S. market, its narrowness makes it an unreliable indicator in some environments. The oil giants Chevron and Exxon have dropped 23% and 15% respectively, dragging the index down. There has still not been a death cross in the broader SP500 index.

To investors now over 60, the equity markets of the past 15 years have told a sobering message. Investors need to either pay some attention or pay someone to pay some attention. The SP500 stock market index has only recently recovered the inflation adjusted value that it had in 2000.

In nominal, or current, dollars, recoveries from major price declines can often take seven years. Past recovery periods were 1968 – 1972, 1973 – 1980, 2000 – 2007, and 2007 to early 2013.

Long term trending indicators may be able to help an investor avoid some – emphasize some – of the pain. For the casual investor, a death cross is a signal to pay a bit more attention to the market on a weekly basis. All death crosses are not created equal. Some death crosses are wonderful buying opportunities. In July 2010, after a two month drop of almost 20%, the 50 day average of the SP500 dropped below the 200 day average, a death cross. Good time to buy. Why? Because it is a death cross coming after a sharp recent drop in price. The same type of death cross occurred in August 2011 after a steep drop in stock price in late July after the “budget battle” between Obama and Boehner went unresolved. Good buying opportunity.

In December 2007, a death cross was not a good buying opportunity? Why? Because it came after six months of the market seesawing with indecision and no net change in price. That indicates that there is a shifting sentiment, a lack of confidence among investors.

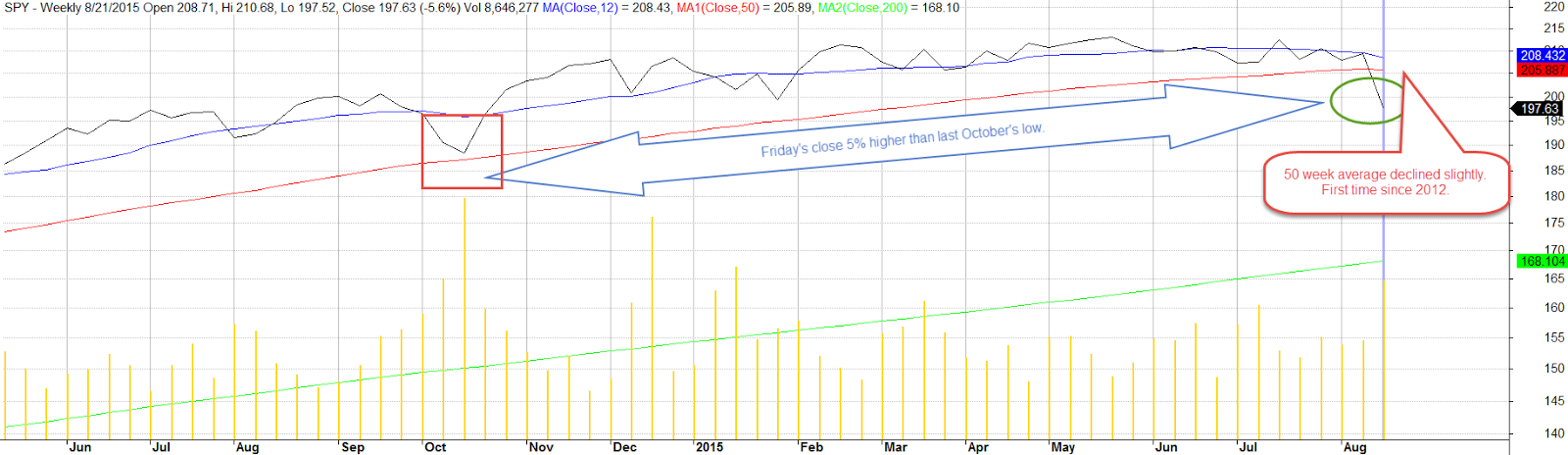

Some mid-term to long-term strategists use a weekly chart which measures the price at the end of each week, that price that short term traders feel comfortable with as they head into the weekend. In a bullish or positive market the 12 week, or 3 month, price average stays above the 50 week, or one year, average. As indecision creeps in the two averages will get close. Finally, the 50 week average will top out, either gaining nothing or losing just a tiny bit as the 12 week average crosses below. We’re not there. We may get there. Who knows?

Once that weekly cross happens, a long term investor might look at a daily chart. What is a good rule(s) of thumb to determine whether a death cross is a good buying opportunity, a negative signal, or a palms up, who knows what the heck is going on, signal?

1) Has there been a decline of 15 – 20% (high price to low price) in the past 2 – 3 months? Is today’s price several percent below the 50 day average? Then it is probably a good buying opportunity as I noted above. It is not always clear cut. In September 2000, the SP500 began a 12% slide in price that would mark the beginning of a downturn lasting several years. In mid-October 2000 a death cross occurred. Was that a large enough slide in price to present a good buying opportunity? Not really. The price that day was almost the same as the 50 day average. The recent drop in price had contributed to the death cross but a longer term re-evaluation of value was also taking place that would cut the SP500 index by 45% toward the end of 2002.

2) If there has been no substantial decline in the past few months, look at the closing price on the day of the death cross. How many months can you go back to find the same price level and how many times has that price level been tested? If just a few months, then this is an indeterminate period of indecision that may resolve itself. Prices may move either higher or lower depending on the resolution. But, if you can go back six to nine months of price flipping and flopping, then it is a bit more serious. There may be a spreading questioning of value, a re-positioning of asset balances. Does it mean sell tomorrow? No. It means pay attention.

After several years of declining prices in the years from 2000 – early 2003, the market had a Golden Cross (50 day average rises above 200 day) in May of 2003. A death cross occurred more than a year later, in August 2004, at the 1095 price level. That day’s price was close to the 50 day and 200 day average and so was not a standout buying opportunity. The market had first crossed above that price level in December 2003, then retested that level three times on market declines only to rise again. Might it have been worth waiting a few weeks to check the market’s short term sentiment and see if that price level would hold again? Probably. As it turned out, the market continued to rise for three more years.

These are not ironclad rules but act as guidelines to help an investor gauge the underlying mood of the market to make more informed investing decisions.