Millennials have witnessed several market selloffs where investors put every kind of asset in their wheelbarrow and bring them to market. Stocks and bonds, equity and debt assets, are supposed to have different risk profiles that are uncorrelated. No matter. Into the wheelbarrow they go. What was valuable a few months ago has become infected with fear, a saleable surplus. The market is neither equitable nor smart, but it is efficient at distributing surplus. Investors sold their fear and bought cash. Cash represents certainty, the antidote to fear.

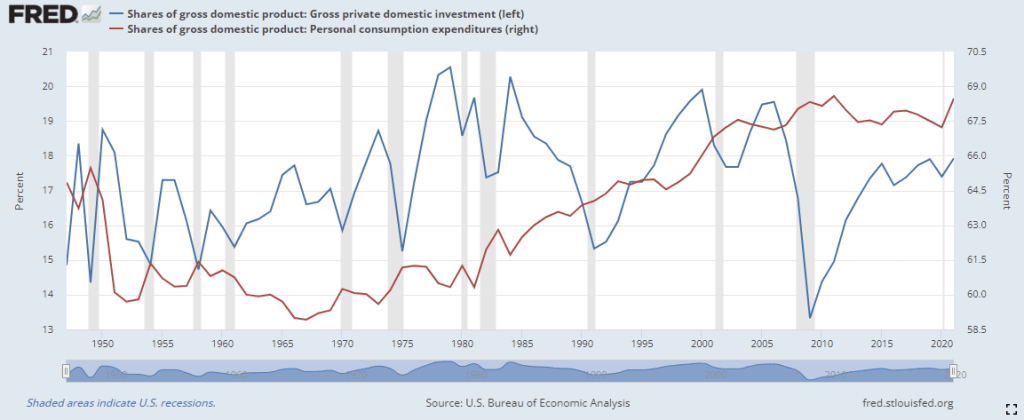

Last year private investment was 19% of the economy, near the top of the historical range of 15-20%. At that level, investment competes with consumption for real resources. The graph below compares consumption and investment as a percent of output. The blue line is investment, including residential housing, the red line household consumption.

Investment looks to the future and is more volatile because it rides on the bumpy road of expectations, a central component of human behavior. People respond not to their current environment but to a forecast of their environment, the uncertainty of further interest rate hikes to combat inflation. The expectation of rising interest rates reduces investment and that helps reduce inflation and the rationale for the Fed’s raising of interest rates – a case of simultaneous causality.

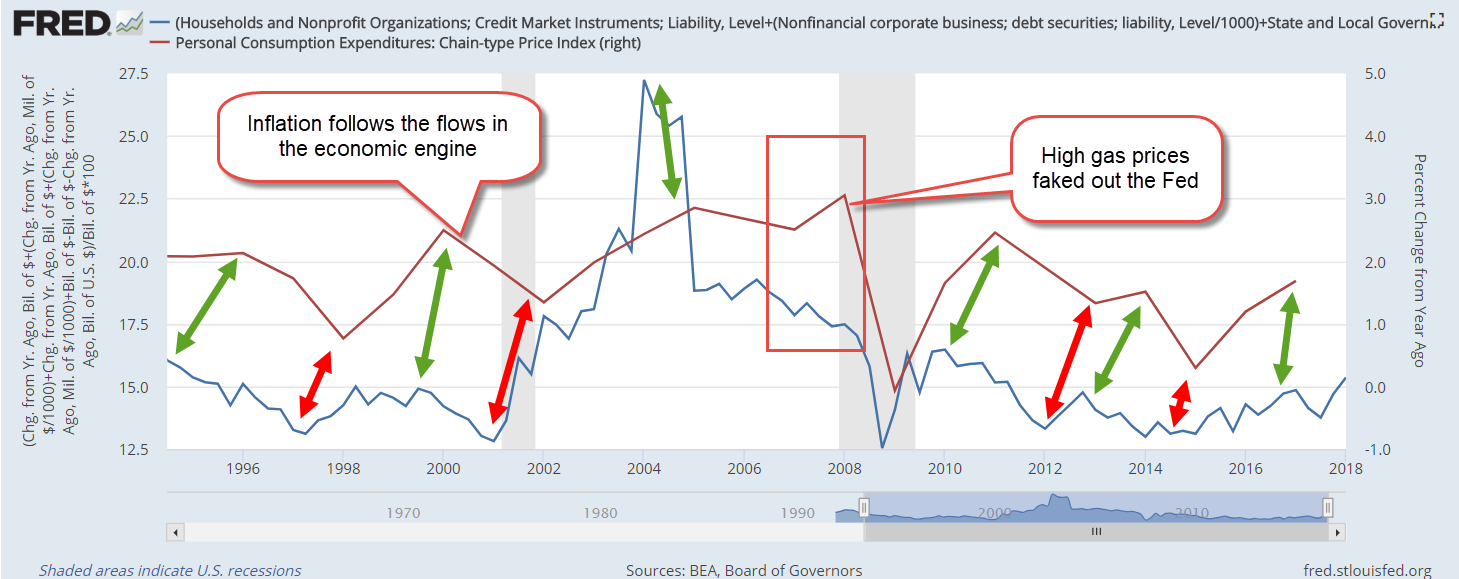

The rise and fall in inflation lags changes in investment by about three months. That does not indicate an “investment causes inflation” causality but signals that they are running around the economic racetrack together. Rising investment brings jobs and higher wages and more spending income. An interruption in the supply chain causes a divergence between supply and demand, between investment and consumer spending. That divergence causes inflation.

A surplus of misplaced investment needs to be redirected to other parts of the economy. Some investment cannot be redeployed and is lost. As the level of investment falls from 19% to 15%, the economy experiences negative growth – a recession. The market distributes saleable surpluses; it doesn’t correct the causes of the surpluses. People, institutions and policies produce surpluses and it is they who have to correct those surpluses. Why doesn’t the market distribute excess wealth? It does, but not where some people would like. People respond to shortages, inequalities of circumstances. The market responds only to surpluses.

In some cities there are a lot of homeless people crowding downtown streets. There is a surplus of little used backyard space to house the homeless. Is there a surplus of homeless people or a shortage of housing? At the heart of a persistent problem is a shortage.

A monetarist like Milton Friedman claimed that inflation was a surplus of money in the system. He argued the root cause of high and erratic inflation in the 1970s was the Fed feeding too much base money into the system. This is “high-powered” money that banks multiply when they make loans. In the peak of the oil shock and recession of 1973-75, the percentage of base money to GDP (bmg) was almost 7%. This level, far above the historical average of 5%, looked like a likely target as the cause for inflation. In the recovery after the financial crisis, bmg was nearly 23% in 2014, more than three times higher. Inflation was low – too low. Cautious bank management had parked that high-powered money at the Fed as excess reserves. The percent of deployed bmg never reached 8%. Today bmg is at 25% but the deployed level of base money has not reached 10%.

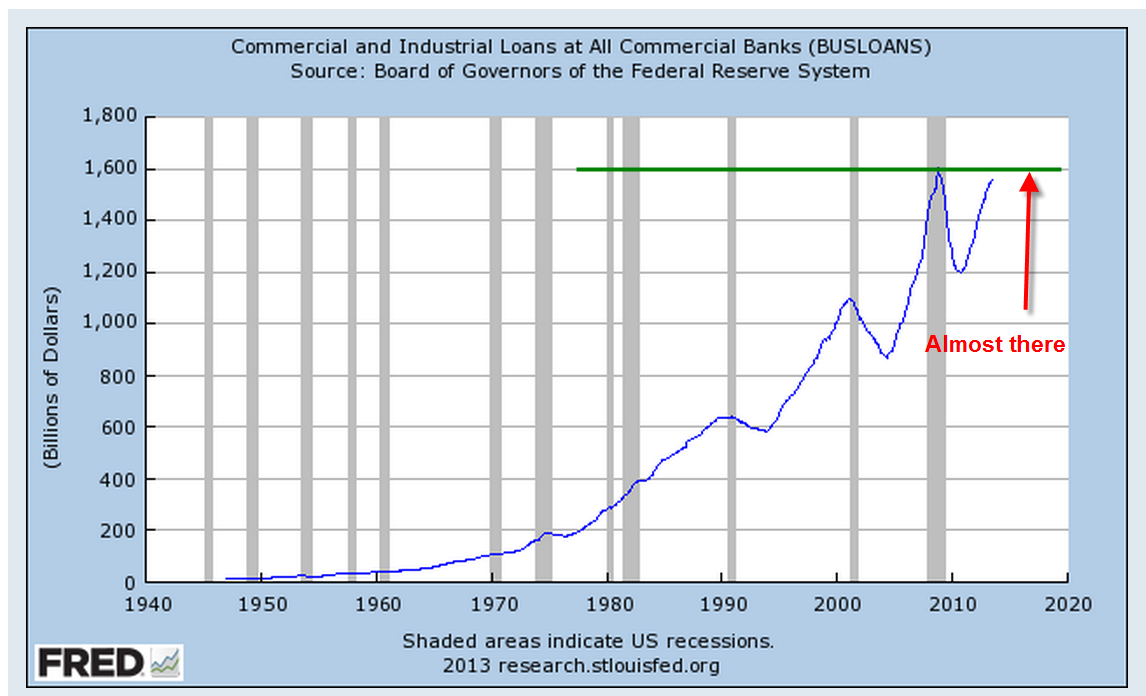

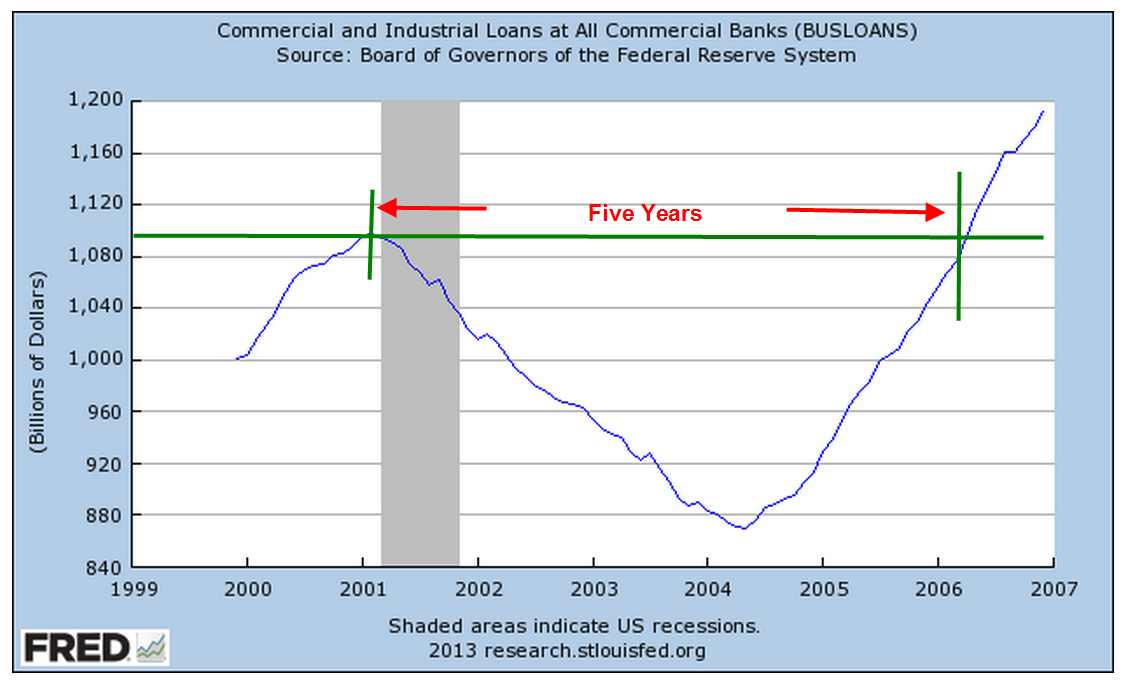

Although the Fed controls the money supply, over 4,000 banking institutions control the effect of changes in the money supply. They direct credit to where they think the losses will be the least and the gains the most. Total bank credit is up more than 9% this year and is at 68% of the economy, a historic high. Growth in businesses loans remains negative after the pandemic and at the level of loans outstanding at their historical norm of 10% of the economy. Consumers have a surplus of purchasing power that the credit market is distributing. Where does that money go? Consumers take the money they get from the banks and spend it at their local businesses. Those businesses do not have to go to the banks to get money as long as their customers have access to bank money and the businesses can attract the customers.

By now Millennials feel like bystanders at a long parade, looking down the street for a empty space that signals the end. 9-11, housing crash, financial crisis, slow recovery with too much unemployment and not enough inflation, then an overheated housing market, a once-in-a-century pandemic and now a period with too much inflation. The oldest Millennials are just approaching middle age and might be wondering if the last half of their lives is going to be as eventful as the first half. No, of course not. Everything will be fine as long as you don’t answer the phone or open the door or say, “I’ll be right back.” It’s just a scary movie.

/////////////////

Photo by Norbu GYACHUNG on Unsplash

Base money is the FRED Series BOGMBASE. Bgm is BOGMBASE / GDP. Deployed bgm is bgm – excess reserves EXCSRESNS / GDP. That series was discontinued in 2020 at the start of the pandemic.

Gross Private Domestic Investment as a share of GDP is FRED Series A006RE1Q156NBEA. Consumption is DPCERE1Q156NBEA.

Total bank credit is TOTBKCR. Business loans is BUSLOANS.