June 14th, 2014

This week I’ll take a look at some near-term trends in small business, labor, oil and housing and a few long-term trends in income and debt.

***********************

Small Business

Huzzah, huzzah! The monthly survey of small business owners by the National Federation of Independent Businesses (NFIB) broke through the 96 level after cracking the 95 level last month. Sentiment has not been this good since mid-2007. Hiring plans have been on the rise for the past several months and owners are reporting rising sales.

**********************

JOLTS (Job Openings and Labor Turnover Survey)

The Job Openings report from the Bureau of Labor Statistics (BLS) has a one month delay so the data released this past week was for April. The number of job openings was 40,000 higher than expected, coming in close to 4.5 million. As a percent of the workforce, job openings are approaching pre-recession highs.

The decline in construction job openings is a disappointment. We are near the same level as 2003, a weak year of economic growth. We should expect to see an uptick in job openings in next month’s report, confirming that projects put on hold during the severe winter in the eastern part of the country are again on track. Further declines would indicate a spreading malaise.

************************

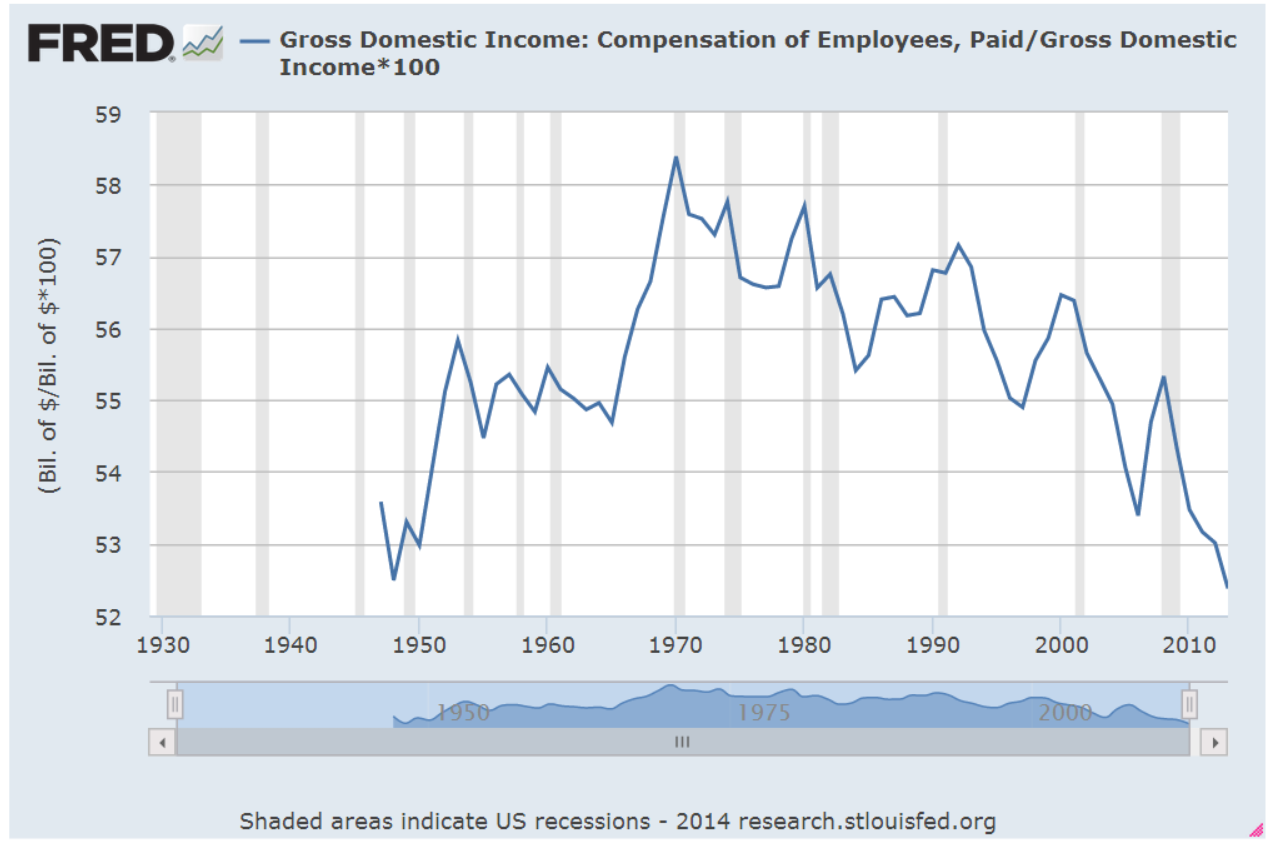

Gross Domestic Income

On a quarterly basis Gross Domestic Income, GDI, and Gross Domestic Product, GDP, differ somewhat but over the long run closely track each other. Following up on two previous posts on Thomas Piketty’s book Capital in the 21st Century, I wondered what percent of GDI goes to pay employee compensation. As we can see in the chart below, total compensation for human labor has been dwindling to post WW2 levels.

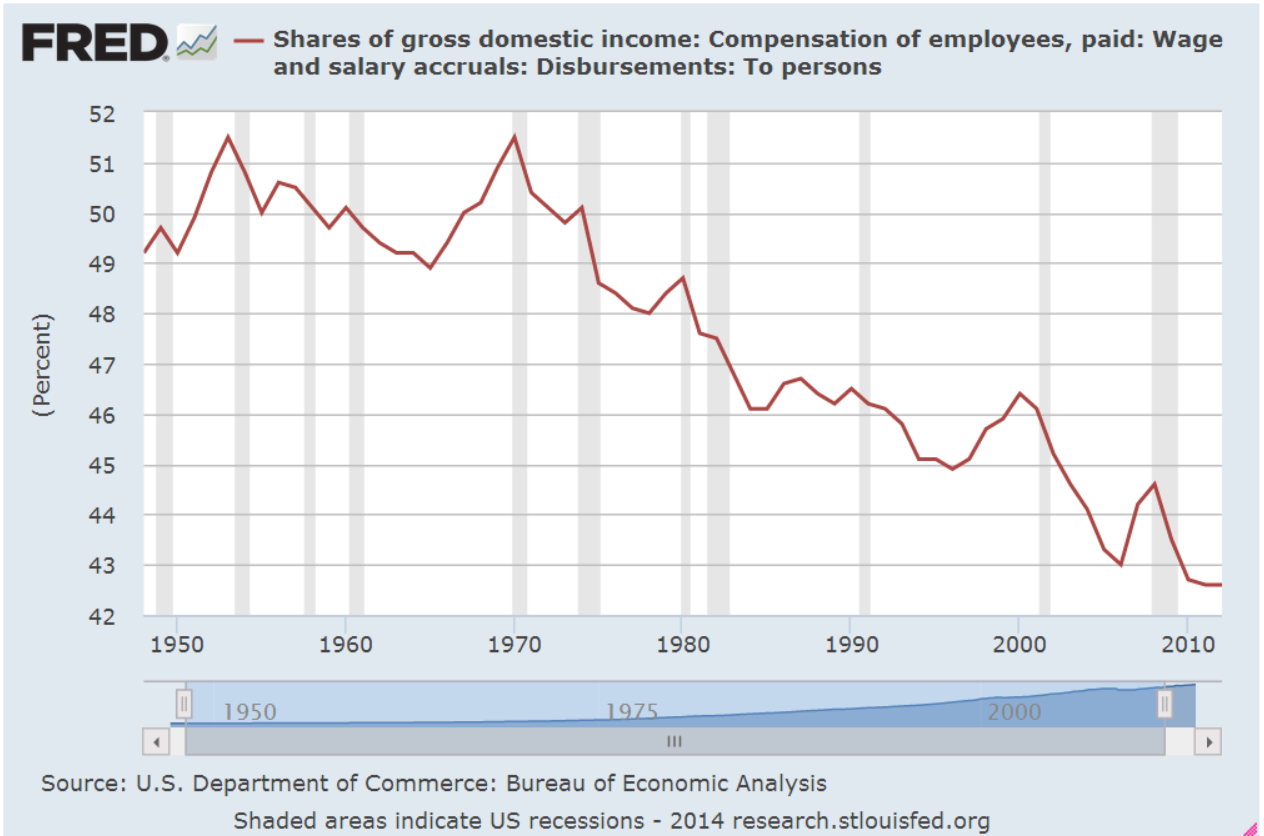

This is total compensation, including benefits. Wage and salary income as a percent of total national income has declined steadily.

As a percent of total income, employee benefits have more than tripled since the end of World War 2 and now comprise more than 10% of the country’s income.

Demographic shifts have contributed to the decline of labor income. The post war boomer generation, 80 million strong and 25% of the population, contributes to the trend as they save for retirement. As capital gains, interest and dividend income increase, this reduces the share of wage and salary income.

Economic changes have been a major factor in the decline of labor income. Capital investments in technology, both in hardware and software, have reduced the need for labor for a given level of production. Capital investment demands income to pay back the investment. For most of the 20th Century, machines replaced human muscle in farming, manufacturing and construction. In the past two decades, machines are increasingly replacing mental muscle.

How we count labor income has changed. Tax law changes in 1986 and 1993 reduced the amounts that are included as compensation but the overall effect of these changes is relatively minor.

If we divide the country’s total employee compensation by the number of employees, we might ask “What recession?” Average annual compensation has climbed from $38-54K in a dozen years. That’s almost a 50% raise for every employee!

Of course, everyone has not had a 50% increase in income over the past 12 years. Human capital, the educational and technical training that an employee has to offer, has earned an increasing premium in the past three decades. Those with more of this capital have captured more benefit from the dwindling pool of labor needed for the nation’s production.

Average disposable income tells a more accurate story of the majority of people in this country. Disposable income is what’s left over after taxes. The trend is downward.

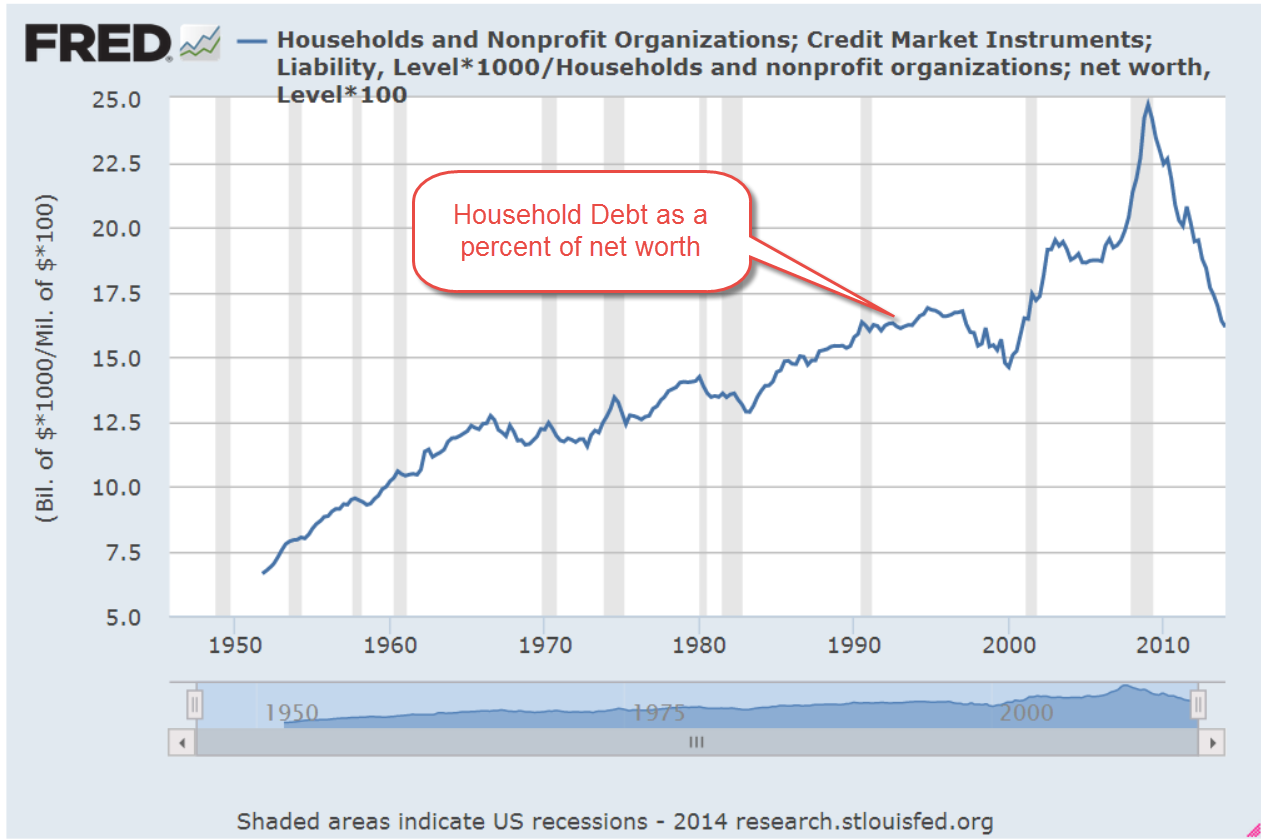

How do we cope with flat income growth? Charge it! It’s the Amurikin way! Per capita Household Debt has increased 75% in the past 13 years. After a decline from the rather high levels before the recession began in late 2007, per capita debt has leveled off in the past two years.

Rising house prices and stock market values have increased net worth. As a percent of net worth, household debt has declined to the more sustainable levels of the 1990s.

The percentage of disposable income needed to service that debt is at thirty year lows, meaning that there is room for growth.

***********************

Oil Prices

A blog by Greg McIsaac at the Washington Monthly in May 2012 presents an interesting historical summary of oil prices and production. The American love of simplicity leads many to credit one man, the President, for the rise and fall in gasoline prices, although the President has little, if any, influence on oil pricing. McIsaac notes “The combination of lower energy prices and increased energy efficiency in the 1980s reduced US expenditures on energy by nearly 6 percent of GDP.“ Deregulation of energy prices begun under the Carter Administration were largely credited to the Reagan administration. He writes “crediting Reagan with falling energy prices of the 1980s exaggerates the roles of both Reagan and deregulation and obscures the larger influence of conservation and increased production outside the US.” Production actually fell for several years after regulatory controls were lifted.

Further increases in oil prices will no doubt be blamed on this President. The one thing that each outgoing President bequeaths to the newcomer before the inauguration is the Presidential donkey suit.

Housing

Redfin Research Center reports a sharp decline in the number of houses sold through May. After a 7.6% year-over-year decline in April, home sales slid 10% from May 2013 levels. Real estate agents are reporting a shift from a seller’s market to a buyer’s market.

***********************