November 13, 2016

Sometimes the hardest thing an investor can do is nothing. That’s pretty much what a casual investor with a balanced portfolio should do in response to the election results. With a portfolio of 57% stocks and 43% bonds and cash, my total portfolio has risen 1/2% this week, or much ado about nothing. Let’s dig into this week’s election results and the market’s reaction.

Donald Trump, the President-elect, has long maintained that his campaign was a movement and was proved right this past Tuesday. White voters from rural districts around the country rallied in strong numbers to Trump’s promise to straighten up Washington.

Voters generally want a change of direction after one party has occupied the White House for two terms and this election proved to be no different. In the modern era of politics, only H.W. Bush was able to gain a 3rd Presidential term for the Republican party in 1988 after two terms of Ronald Reagan. Countering the emotion and momentum of the Trump movement on the right were the voters on the left who passionately turned out for Bernie Sanders in the Democratic primaries. Voters and superdelegates chose the establisment candidate, Hillary Clinton. Some say that the process and the rules favored Clinton over Sanders. His supporters are convinced that Sanders could have beat Trump. Movement against movement.

In the past decade, voters have expressed a preference for rallying cries, for mantras of momentum like “Si se puede!” (Obama), “Build the wall!” (Trump) and “Medicare for all!” (Sanders). Candidates must learn to condense their message into a short slogan that can be easily waved. McCain, Romney and Clinton never found a verbal cadence that would act as a catalyst for voters to enthusiastically join the parade. Sarah Palin, McCain’s Vice-Presidential candidate in 2008, understood the need for slogans.

Note to future Presidential candidates who would like to actually win: criticize the candidate, not that candidate’s supporters. Hillary Clinton made the same mistake that Romney made in the 2012 election – disparaging their opponent’s voters.

Election night. As a Trump victory became increasingly probable, global markets began to sell risk (stocks) and buy safety (bonds). In the early morning hours after the polls closed, the networks called the state of Wisconsin for Donald Trump and put him over the threshold of 270 votes in the Electoral College. Several minutes later, about 2:45 AM on Nov. 9th, we learned that Hillary Clinton had called Donald Trump to concede and wish him luck. Dow Futures were down about 4% at that point. Japan’s stock market was down 5.5%. The yield on the 10 year Treasury note was down 7.22%, meaning that the price was up about 8% as investors in world markets were seeking the safety of U.S. debt. Emerging markets fell in anticipation of protectionist trade policies under a Trump administration.

About 3 A.M. President-elect Trump began to give a sedate and rational acceptance speech that began with a gracious nod to Hillary Clinton’s fight. He spoke of unity, healing and more importantly, infrastructure spending and tax cuts. With control of the Congress and Presidency in Republican hands, there was real hope that Washington could end the years of stalemate and finally implement fiscal policy to rescue a economy that had been kept afloat by an exhausted monetary policy for six years.

The overseas markets began to turn around. By the time U.S. markets opened more than six hours later, stocks and Treasuries had reversed. Stocks were now off less than 1/2% and Treasury prices were down severely. TLT, a popular ETF for long term Treasuries, opened about 2% lower, a price swing of 10%. EEM, a composite of Emerging Market stocks, opened up almost 3% down and lost ground during the trading session. By week’s end the SP500 had risen 3.8% for the week, and EEM had fallen by that same percentage.

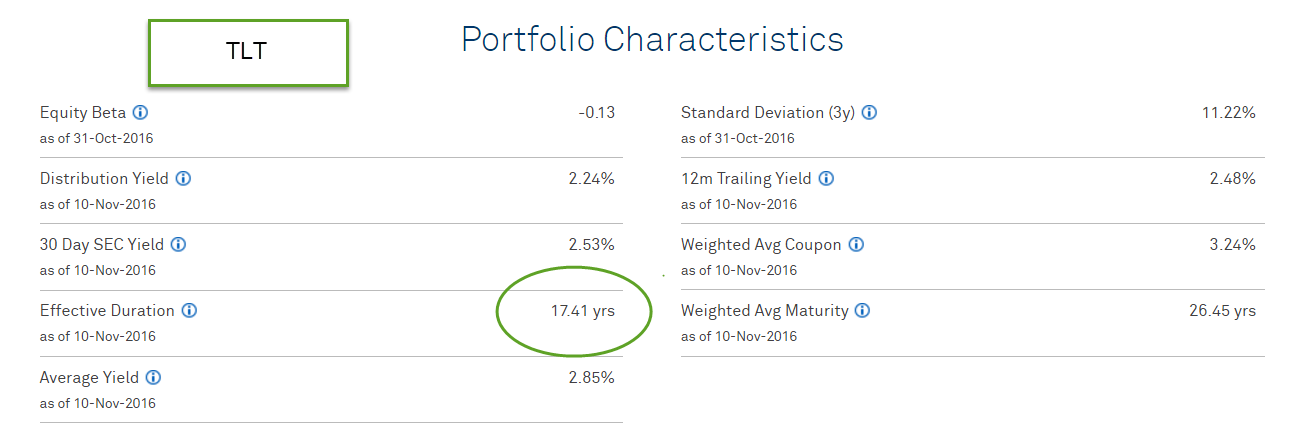

This week’s action in the bond market was a good example of the mechanics of bond pricing so let’s look at the price action and what it says about the future guesses of the direction and extent of interest rates. First, bond prices move inversely to interest rates. The extent that these prices move is measured by a bond’s duration. Here is a link to the iShares page for the TLT ETF on long term Treasuries. I have captured a section of the page with the duration highlighted.

If you have a bond fund, the mutual fund company will state the bond duration as well. What does this tell you? Leverage. Duration tells you the approximate change in price for a 1% change in interest rates. In this case, a 1% increase in interest rates will generate about a 17% decrease in price. Because TLT is a composite of long term Treasuries, its price is more sensitive to changes in interest rates, or the consensus on interest rates six months to a year in the future. The price of TLT fell 7.4% this week as traders repriced future interest rates. With some grade school math, we can calculate what traders are guessing interest rates will be a half year to a year from now.

The Fed last raised rates at the end of 2015, putting them at approximately 1/4% – 1/2%. In July, the price of this ETF was about $142. It closed this week at $122, a decline of 14% from the summer high. Now we divide the 14% by the bond’s duration of 17.41% to get a ratio of .80. This is the new guess of how much interest rates are likely to rise – approximately 3/4% – 1%. By the fall of 2017, traders are betting that the benchmark Fed interest rate will be about 1.25% to 1.5%.

Let’s look at a more balanced composite bond ETF that financial advisors might recommend for casual investors. Vanguard has a more conservative composite ETF whose ticker symbol is BND, with a duration of 5.8, about a third of the TLT ETF. (Spec Sheet here) This week BND lost almost 2% and is down almost 4% from its summer high. When we divide 4% by 5.8% (the duration in percentage terms) we get a guess of about a .7% raise in interest rates. Because BND contains shorter term bonds, this guess is slightly below that of TLT.

Why are traders betting on more aggressive interest rate increases after Donald Trump was elected? He has spoken about infrastructure spending and tax cuts, two fiscal stimulus programs that will likely spur inflation upward. With a Republican party that has control of the Presidency and both houses of Congress, these measures are likely to be passed in some form. Some sectors of the economy will likely benefit from more infrastructure spending so they rose this week. Shares in technology giants like Apple and Google fell as traders switched money among sectors but are still up by healthy margins since February lows.

Let’s say that next March comes and the Trump White House and the House Budget Committee can not come to terms on either of these programs. Investors would likely reprice interest rate expectations and lower them, causing the price of bond ETFs or mutual funds to rise.

/////////////////////////////////

Miscellaneous Election Notes

I’ll share a distinction that NPR’s David Folkenflik made this week. Those on the left took Donald Trump literally, but not seriously. Those who voted for him took him seriously, but not literally.

During Thursday’s trading the Mexican peso fell to 15.83 per dollar, the lowest since 1993 when Mexico reset their currency. Why the big drop? Trump has repeatedly said that he would cancel the NAFTA agreement that binds Mexico, Canada and the U.S. The NAFTA agreeement requires only a 6 month notification before termination. There is some disagreement whether the White House would need Congressional approval to cancel NAFTA which might delay the action. Some in the Republican party like free trade agreements and are likely to put up a fight. Some analysts think that the devaluation of the peso could lead to a recession in Mexico, which was already under economic pressure due to falling oil prices.

131 out of 231 million registered voters cast their vote in this election, slightly below the voter total in the 2008 election. (538) Trump and Clinton each took 26% of registered voters.

The Trump White House can reverse Obama’s executive action on the Keystone pipeline and re-initiate construction. It will likely amend or repeal tentative proposals to mitigate climate change.

Why did pre-election polls get it so wrong? According to Pew Research, more than a third of households would respond to a survey a few decades ago. Now it is only 9%. Statisticians must tweak this rather small sample to make it more representative of the population as a whole. A particular demographic constituent in the sample – say white working class men – might be underrepresented in the survey. Survey methodology then gives the opinion of relatively few sample respondents more weight than it actually has in the general voter population.

Some statisticians recommend using economic and demographic algorithms to gauge future election results based on actual past voting records.

Of the 700 counties that voted for Obama in 2012, a third of those voted for Trump in 2016. Polls indicated that Hillary Clinton would capture the majority of the white college-educated vote for the first time in decades but she failed to do so. More white voters voted for Obama than Hillary.

A third of Democrats in the House come from just three states: California, New York and Massachusetts. This concentration may answer to the concerns of those states but indicates that the party has become out of touch with the voters in many states.

Each time a Democratic candidate is elected President, unfounded rumors circulate that the new President will take away people’s guns. People rush out to buy guns. Trump’s surprise win caused the stock of gun maker Smith and Wesson to decline 22% in a couple of days.

On the other hand, many women feared that Trump and a Republican Congress would restrict birth control and stocked up in the days after the election. Here is a map of abortion regulations in the states before the 1972 Supreme Court’s decision in Roe v. Wade. Abortion was more permitted in the southern states than the northeast states.

Here‘s a state-by-state breakdown of the vote from NPR.