January 29, 2017

Welcome to the new site, Innocent Investor. You can easily reach this blog by entering innocentinvestor.com into your browser. Loyal readers can resubscribe by clicking the RSS Feed button at the bottom of this blog. For a few weeks, I will post up a short entry at LucreTalk.blogspot.com in order to activate existing RSS feed subscriptions.

I think readers will love the presentation of both text and graphics in this WordPress format. I plan to integrate comment balloons so that a reader who is unfamiliar with a term like “GDP” can hover over the word and a quick explanation of the term will appear.

On the menu at the top of each page is an item labeled “Tools.” That page is under construction but will include many of the resources I have mentioned over the course of the past eight years.

/////////////////////////

The Presidential Baton

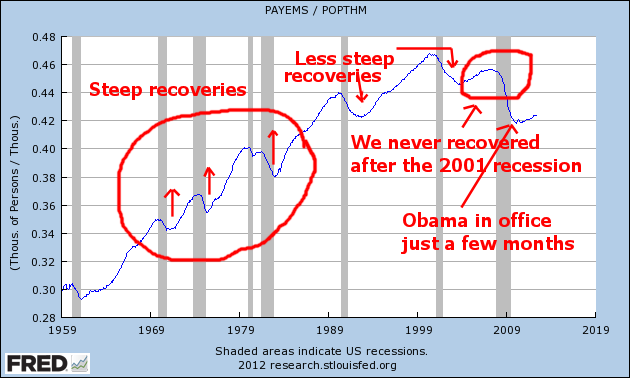

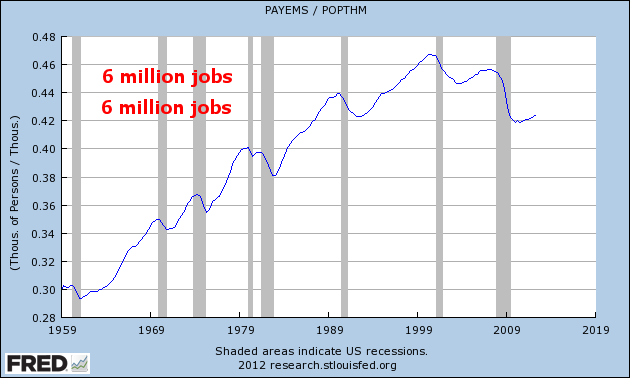

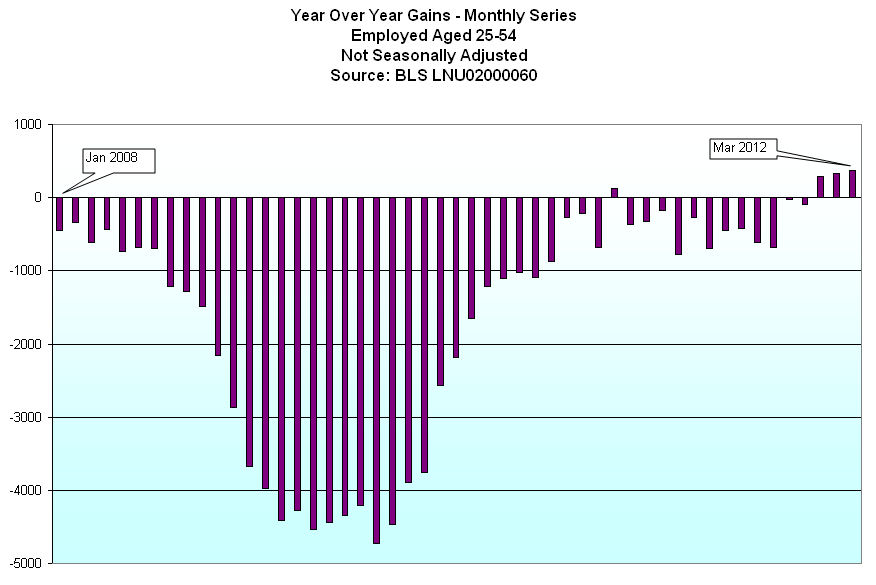

After the Trump inauguration, President Obama and his family boarded a helicopter bound for Andrews Air Force Base. The headline U-3 unemployment rate was less than 5%, half the level when he had taken office eight years earlier. In that time, the SP500 stock index had almost tripled. Consumer Confidence has risen from 61 in January 2009 to almost 100 as he left. GDP has been growing for 30 quarters.

Good job, Mr. Obama. Thanks for your leadership during a very bad economic crisis, and have a good life. Wouldn’t it be nice? History is a messy business. Presidents endure a lot of stress, their families make major compromises and yet half of us focus on their faults.

Let’s revisit another President who took office during very bad economic times, Ronald Reagan. When he assumed the leadership role, we were on the tail end of a recession, and still deep in an energy crisis. Interest rates and inflation were more than 10%, small business loans were about 20%, and the unemployment rate was 7.5%.

Reagan made the difficult decision to let Fed Reserve chief Paul Volker take some monetary measures to bring down interest rates, knowing that those actions would probably send the economy back into recession. Unemployment rose 3% to 10.8%, GDP fell 2-1/2% and stayed negative for four quarters. Inflation came down from 10% to less than 5% in that year long recession, providing an environment for businesses to grow and consumers to borrow. Real GDP started growing at rates greater than 5%, and in 1984, Reagan was re-elected by a landslide over Walter Mondale.

A historic tax reform bill capped Reagan’s second term in office. Like health care, tax reform is notoriously difficult because there are so many powerful interests involved. Although the Soviet Union did not officially collapse until 1991, the democratization process began in 1987 and conservatives have built a narrative that credits Reagan for the collapse. Like the executive of any large corporation, a President takes the credit and the blame.

A President’s administration rarely escapes scandal, and Reagan’s second term was so riddled with scandal that his own Vice-President, H.W. Bush, had to distance himself from Reagan’s policies in Bush’s 1988 Presidential bid. Iran-Contra and the S&L crisis were the most conspicuous of the scandals, but the Keating 5, and the HUD and EPA Grant Rigging to influence elections indicated an administration with lax ethics.

Let’s turn back to the first few months in former President Obama’s first term. Almost daily came the announcement of another major American company near bankruptcy. In February 2009, a few weeks after Obama’s inauguration, the credit rating firm Moody’s estimated that 15 large companies were close to bankruptcy in the coming year.

The list included Rite-Aid drugstores with 100,000 employees, Chrysler with 55,000 workers, Blockbuster with 60,000 employees, and Six Flags Amusement Parks with 30,000 workers. One of the companies, Trump Resorts with 9500 workers, went into bankruptcy within a month of Obama’s inauguration.

During Obama’s first two years he was able to get some fiscal stimulus enacted and, like Reagan, took on a historic task – health care reform. The tax bill of 1986 was passed by voice vote (Govtrack) so we don’t know the vote by party. However, the Democrats held the house at that time so nothing could be done without bipartisan bargaining. On the other hand, the health care reform was passed without a single Republican vote. A hostile voter reaction to Obamacare swept the Republicans into control of the House in 2010. The Republican House stymied attempts at further stimulus or much of any fiscal policy to alleviate the economic suffering.

The policy burden of economic recovery rested on the shoulders of the Federal Reserve, who were forced to be extremely accommodative to avoid another recession. Throughout this long and slow recovery, the Fed’s monetary tools have been stretched thin to the point of ineffectiveness. For several years, they have wanted to raise interest rates to a more normal range of at least 2%. This past year, Chair Janet Yellen felt confident enough to bump up rates by a mere 1/4% in December. This left the key interest rate in a range of just .5% – .75%.

With one party government Donald Trump has promised to get a languidly growing economy into high gear. GDP growth in the 4th quarter slowed to 1.9%, bringing annual growth in 2016 to a disapointing 1.6%. The post-WW2 growth rate is more than 1% higher.

The bond market is estimating that the Fed will raise interest rates three more times this year. This attempt to normalize interest rates may frustrate the Trump administration, since rising interest rates tend to curb economic growth. President Trump will likely voice his antagonism but Chair Janet Yellen has pledged to serve out her full term, which expires in February 2018.

//////////////////////

Best President for Stock Market

So you were having a friendly conversation with a co-worker about Obama’s legacy and you mentioned that Obama had been the best President ever for the stock market. The conversation turned not so friendly and the issue was left unresolved because neither of you could find the information at the time. Well, here’s the chart

Coolidge, the President that many of us forgot in history class, ranks top with annual gains of 25%.

The chart ranks the Presidents by Total Return during their term(s) in office. Because term lengths vary, a truer rank is by annualized return (many times the rankings are the same). Coolidge tops the list in both categories. #2 is Clinton, #3 Obama, #4 Reagan. The worst on the list were #19 Hoover, and #18 G. W. Bush.