by Stephen Stofka

This is 12th in a series of debates on various issues. The debates are voiced by Abel, a Wilsonian with a faith that government can ameliorate social and economic injustices to improve society’s welfare, and Cain, who believes that individual autonomy, the free market and the price system promote the greatest good.

This week, Abel began the conversation. “Toward the end of our conversation last week, you mentioned the shift of voter sentiment toward the right.”

Cain nodded, “Yes, the New York Times analyzed the change in election results from the 2020 election and it showed a shift toward the Republican Party in most counties (Source – NY Times).”

Abel interrupted, “Voters shifted left in the 2020 election. For the past twenty years, sentiment seesaws left and right with each election. Voters are so evenly divided that a slight shift can have a dramatic effect on party control of government.”

Cain argued, “This time is different. The voters want change. The neoliberal wing of the Republican Party has been discredited and driven out after two failed wars and a permissive trade policy that boosted China’s economy at the expense of American jobs. Gary Gerstle (2022, pg. 2) writes that it was the financial crisis that triggered the fall of the neoliberal order. President Trump is trying to undo the mistakes of that neoliberal ideology.”

Abel frowned. “I’ve read that book. Gerstle also noted that neoliberal policies were responsible for a lowering of the barriers to free trade (pg. 5). Tariffs and borders, for example. Trump is on a mission to rebuild those barriers. That will only hurt trade and weaken American business and consumers.”

Cain shook his head. “Open borders allowed for the smuggling of drugs and people across our southern and northern borders. The costs of open borders outweigh the benefits.”

Abel sighed. “25% tariffs on imports from Mexico and Canada are going to fuel inflation and hurt consumers. Both countries have said they will retaliate. We export a lot of grains to Canada. That will hurt our farmers.”

Cain argued, “In 2002, President Bush raised tariffs on steel and aluminum imports to as much as 30%. A year later, after complaints to the WTO, Bush ended the tariffs. Trump is made of stronger stuff. These countries are not doing enough to curb drug and people smuggling. It may not be an explicit violation of trade rules, but it violates the spirit of those rules.”

Abel replied, “Bush did that to save jobs in the steel industry. Instead of stemming the flow of jobs to other countries, the tariffs caused the loss of 200,000 manufacturing jobs (Source). Trump’s tariffs are going to raise unemployment and cost consumers.”

Cain rolled his eyes. “We’re not going to agree on this. We have got to restore our nation’s manufacturing capacity and the supply chains that support production that is vital to our security. China controls a lot of essential minerals used in the production of electronics. They are actively pursuing alliances with African countries to lock up essential mineral resources. This is economic warfare, and we have to take measures to defend ourselves.”

Abel frowned. “Tariffs lead to trade wars. Trump is acting like he has a mandate. He won with the lowest margin of the popular vote in the past four decades – just 1.5%. He didn’t even get a majority of the votes (Source). In 2016, he got fewer votes than Hillary Clinton. Contrast that with Obama, who had a 7.2% margin of victory in 2008, and Biden who won by 4.5% in 2020. Voters for Trump are going to wake up and find that they have been screwed.”

Cain argued, “Democrats always use the popular vote as a measure of voter approval. States with a less concentrated population provide the resources that are vital to the economy and security of this country. Those states supply the food, the beef, the fuel that people in urban areas rely on. It’s an economic symbiosis. The producers and workers in rural areas should not be put at a disadvantage simply because their production requires more land. The Electoral College balances the inequities that result from a popular vote.”

Abel scratched his chin. “Tariffs are going to hurt the rural producers and workers that voted for Trump. Those red rural states already depend on the coastal blue states for federal benefits like farm and oil subsidies, Medicaid and welfare and they resent it. They imagine that Trump will revitalize rural economies so that they are more like it was in the 1950s when relative wages were higher. It was the unions who bargained for those higher wages and benefits. Without unions in the private sector, wages in rural counties will remain low.”

Cain raised an eyebrow. “Unions abused their power and companies became less competitive. Unions sometimes enforced rules among their members with violence or intimidation in the workplace (Source). They invite free riding. ‘Shirkers’ are paid at the same rate as productive employees. It’s bad for morale and makes workers less productive as a whole. An employee in a union has two bosses – the shop steward and the employer. The employer wants the employee to work at their best. The shop steward might want an employee to slow down so as not to raise the employer’s expectations.”

Abel cocked his head slightly. “Free riding is a collective action problem that is not unique to labor unions. They empowered workers in negotiations with large companies who wielded extraordinary power in the labor market. In some counties, a company was a monopsony, the main source of employment for everyone in that region.”

Cain argued, “The government is the largest employer in the country employing over 23 million at various levels (Source). Walmart, the largest private employer, has just over 2 million workers (Source). Unions have taken over the public sector.”

Abel interrupted. “Let me stop you there. The BLS just released their annual survey of union membership. It’s less than a third in the public sector (Source).”

Cain nodded. “OK, perhaps I overstated the percentage. Still, public sector membership is five times what it is in the private sector. Unions may give workers more bargaining power, higher wages and more benefits. Who pays for all that? Taxpayers. Our public schools are not teaching essential reading and math skills. Fewer police officers on the street. Potholes go unfilled. What are taxpayers getting for their money? Screwed.”

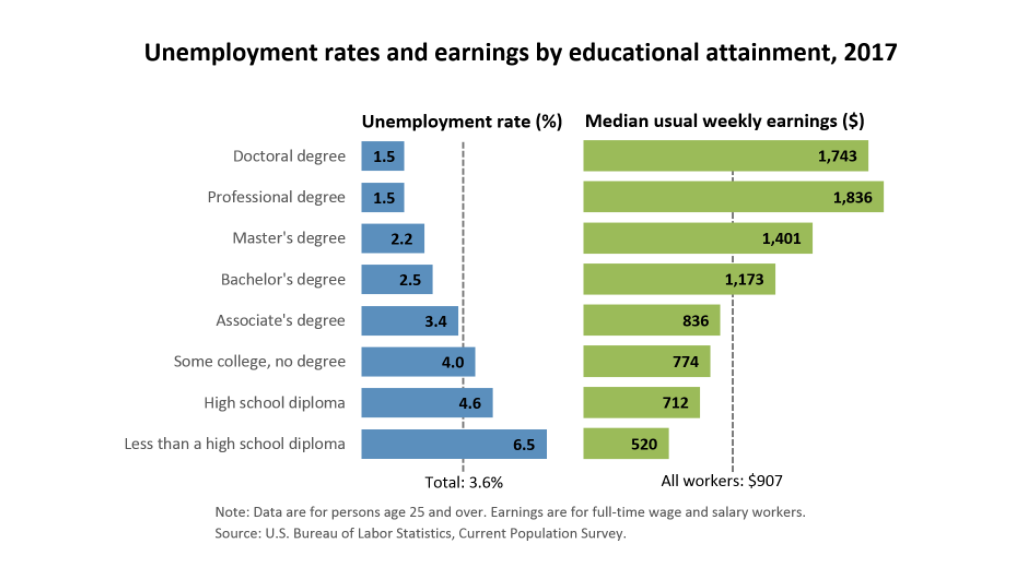

Abel scoffed. “Elementary school teachers generally make less than the average wage in their local economy. In Denver, an elementary school teacher averages almost $54,000 (Source). The average in private industry is more than $80,000 (Source).”

Cain argued, “Ok, so maybe elementary school teachers in Denver are underpaid. Their main funding source is local property taxes. In the whole metro area though, federal government employees make $2128 a week (Source). That’s far above the average weekly wage of $1721 in the private sector (Source).”

Abel shrugged a shoulder. “Look, Denver is a regional hub. There is a higher proportion of tech employees in the federal workforce in Denver than the private sector. State government employees make just $2 more than the average (Source).”

Cain frowned. “If the mix of jobs and talent was similar to the private sector, then their union is not very effective at negotiating pay.”

Abel showed some impatience. “Your group doesn’t like unions. I get that. Incorporation is a collaboration of capital for investor profits. A union is a collaboration of workers for better pay and working conditions. Capitalism has been so successful because it turns the free riding problem into an advantage.”

Cain laughed. “You’re saying something good about capitalism? Go on.”

Abel smiled. “Small investors, holders of common stock in a company, enjoy the same return on their capital as the giant hedge fund who may own a substantial stake in the company. Because they have so much at stake, large investors take an active role in monitoring or directing management decisions. The small investors freeride on those efforts.”

Cain nodded. “That’s an interesting perspective. I still don’t think that unions are needed to negotiate for workers. Worker productivity and demand will support higher wages.”

Abel sighed. “In theory. This is the real world, not a freshman class in economics. If capital can collaborate to gain bargaining power, workers must collaborate to match that power.”

Cain motioned his impatience. “We started out talking about tariffs and now we’re talking about unions.”

Abel laughed. “We are exploring different perspectives. We will never come to an agreement unless we try to understand each other’s positions on these issues.”

Cain nodded. “See you next week then.”

///////////////////

Image by ChatGPT

Gerstle, G. (2022). The rise and fall of the neoliberal order America and the world in the free market era. Oxford University Press.

The American Federation of Government Employees represents 800,000 of two million federal employees (Source). The American Federation of State, County and Municipal Employees represents more than 1.3 million workers (Source).