August 25th, 2013

(First a little housekeeping: an anonymous reader commented that when they clicked the “back” button after viewing a larger sized graph they were returned to the beginning of the blog post instead of where they had left off when they clicked on the smaller image within the text. I suggest that, after viewing a graph, try clicking the ‘X’ button on the top right of the graph page to return to where you left off. This works in the Chrome browser.)

Since the onset of the recession in late 2007, I have read many articles on the lack of wage growth despite big gains in productivity. Ideas become popular when they have a narrative, one that I took for granted. Each quarter, the Bureau of Labor Statistics (BLS) issues a report on productivity and labor costs that I have taken at face value.

The 2001 manual of the OECD manual states “Productivity is commonly defined as a ratio of a volume measure of output to a volume measure of input use.” They frankly admit that “while there is no disagreement on this general notion, a look at the productivity literature and its various applications reveals very quickly that there is neither a unique purpose for, nor a single measure of, productivity.” (Source)

The authors of a recent paper at the Economics Policy Institute cite BLS data showing that productivity has grown “by nearly 25 percent” in the period 2000 – 2012 while the median real, that is inflation adjusted, earnings for all workers has essentially remained flat. Company profits are at all time highs and workers are struggling. The narrative is familiar but I wondered: how does the BLS calculate productivity growth?

What the “headline” productivity numbers describe is labor productivity, the output in dollars divided by the number of hours worked. The BLS Handbook of Methods, page 92, gives a detailed description of its methodology. As the BLS notes, this often cited productivity figure disregards capital investments in output like machinery and buildings. For this reason, the BLS also calculates a less publicized multifactor productivity measure using methodologies which do incorporate capital spending. How does capital investment influence the productivity of a worker?

Consider the simple case of a man – I’ll call him Sam – with a handsaw who can make 20 cuts in a 2×4 piece of lumber in an hour. His company charges customers a $1 for each cut, the going rate, so that the company can sell Sam’s labor for $20 per hour. Due to increased demand for wood cutting, the company invests $1000 to buy an electric chop saw. The company calculates that Sam’s productivity will rise enough that they can undercut their competition and charge 75 cents a cut. With the chop saw, Sam can now make 60 cuts per hour at .75 per cut = $45 dollars in revenue per hour to the company. Sam’s labor productivity has now risen 150%. In our simple case, this would be the headline labor productivity gain – 150%.

A more complete measure of productivity including capital investments is quite complex. The latest edition of the OECD handbook notes that “there is a central practical problem to capital measurement that raises many empirical issues – how to value stocks and flows of capital in the absence of (observable) economic transactions.” To illustrate the point further, the asset subgroup listed in the BLS handbook includes “28 types of equipment, 22 types of nonresidential structures, 9 types of residential structures (owner-occupied housing is excluded), 3 types of inventories (by stage of processing), and land.”

You want simple? Let’s go back to our kindergarten example. At this rate of production, let’s say that the saw’s useful life is only 10 months. The company has an investment of $100 per month in the saw, plus additional costs like electricity, a bigger workbench, etc. To round out the numbers, let’s say that equipment related costs are $150 a month. If Sam’s output is 8 hours a day x $45 an hour, Sam is producing $360 per day in revenue for the company, or close to $8000 a month. The $150 a month in equipment costs is trivial and multi-factor productivity is very close to labor productivity.

Sam knows he is making much more money from the company and goes to his boss and says he wants a raise. Not only is he producing more for the company but the electric saw is much more dangerous than a handsaw. The company gives Sam a raise from $7 an hour to $8 an hour, an almost 15% increase that Sam is happy with. In addition to the raise, the company has an additional $2 in mandated labor costs, bringing the total costs for Sam’s labor to $10 an hour. Even with the higher labor costs, the company is raking in huge profits – $35 an hour – from Sam’s labor.

But now an inspector comes in and tells the company that, because an electric saw makes much more dust than a handsaw, the company will have to install a ventilation and filtering system so that the employees and neighbors won’t have to breathe sawdust. The company gets bids that average $100,000 to install this system and the company estimates that the system will equal $1000 a month in additional capital costs. Despite the additional costs, the company still continues to make substantial profits from Sam’s labor. To the company, the capital costs for this new system represents about 60% of an additional worker’s labor costs, yet that additional cost is largely not included in measuring labor productivity because Sam’s hours and the revenue generated by Sam’s labor remain the same.

A multifactor productivity comparison of handsaw vs. chopsaw production would show a percentage growth of 40%, far below the 150% labor productivity growth.

All of us have our biases (except my readers who are perfectly rational beings) which cause us to look no further than the narrative that clearly supports our previous conceptions. If we generally agree with the narrative of companies taking advantage of workers, we read of 25% productivity gains for companies and 0% gains for workers in the past twelve years, and we look no further – for the data has confirmed what we previously had concluded. Big companies = bastards; workers = victims.

In June 2013, the BLS released revisions to their productivity figures for 2012 and included historical productivity gains for various periods since 1987. During the past 25 years, multifactorial productivity, including capital investment, has averaged .9% per year – less than 1%.

While labor productivity has grown 25% since 2000, multifactorial productivity has been half that, at about 12%. Dragging the 25 year average down is a meager .5% growth rate since 2007. Even more striking is the growth rate of input into that recent tepid productivity growth; the BLS calculates 0% net input growth since 2007. For the past 25 years, capital investment has grown at more than 3% but since the recession capital growth has slowed to 1.3% per year. I wrote last week that there is an underlying caution among business owners and this further confirms that caution; companies have been cutting back on both labor and capital investment.

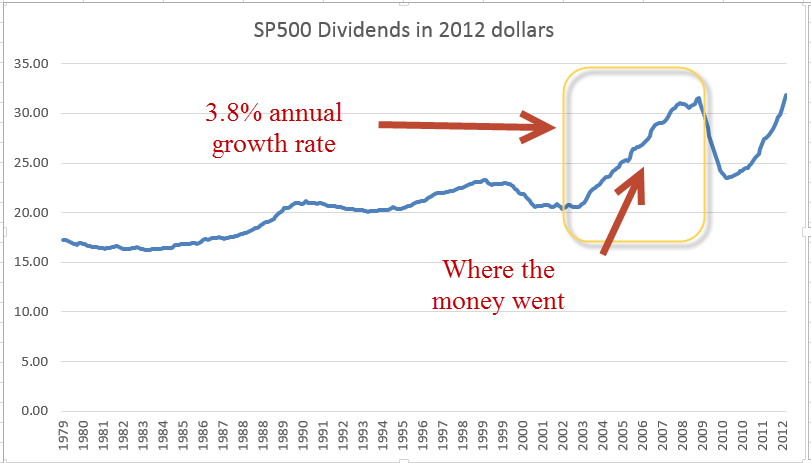

If multifactorial productivity rose by 12+ percent over the past 12 years, and the profits did not go to workers, where did the money go? For a part of the puzzle, let’s look to inflation adjusted dividends of the SP500.

From the beginning of 2000 through 2007, when the recession began, inflation adjusted dividends grew at an annual rate of almost 3.8%, eating up most of the profits from productivity growth. As bond yields continued to decline, I would guess that investors pressured companies for more of a share of the profits from productivity growth.

As workers lost manufacturing jobs during the 2000s, many were able to switch to construction jobs in the overheating real estate market and unemployment stayed low. This should have pressured management to give into labor demands for an increased share of the productivity growth but it didn’t. I suspect that the labor mix contributed to the lack of pressure on management. Fewer manufacturing jobs meant fewer union jobs; a reduced labor union influence meant less demand on management.

Looking past the headline labor productivity gains, overall productivity is slow. Capital and labor investment is slow, which means that future overall productivity is likely to remain slow.

While walking a trail in the Colorado Rockies years ago, my brothers and I complained about having to dodge moose poop on the trail. Then we ran into the bull moose that made the poop.