March 15th, 2014

Small business

The monthly survey of small businesses showed an abrupt decline in sentiment, below even the lowest of expectations, and the sixth report since the beginning of the year to come in below the consensus range. Two factors led the downward change: lowered sales expectations and hiring plans. The majority of business owners surveyed are reducing, not adding to inventory. The steady but slowly improving sentiment during 2013 has now weakened.

This reading of optimism among small business owners is indexed to 100 in 1986. The current survey reading of 91.5 is far above the pessimistic level of 80 that the index sank to in the early part of 2009. In 2006, sentiment broke below the 95 level and has not risen above that since – eight years of below par sentiment among small business owners.

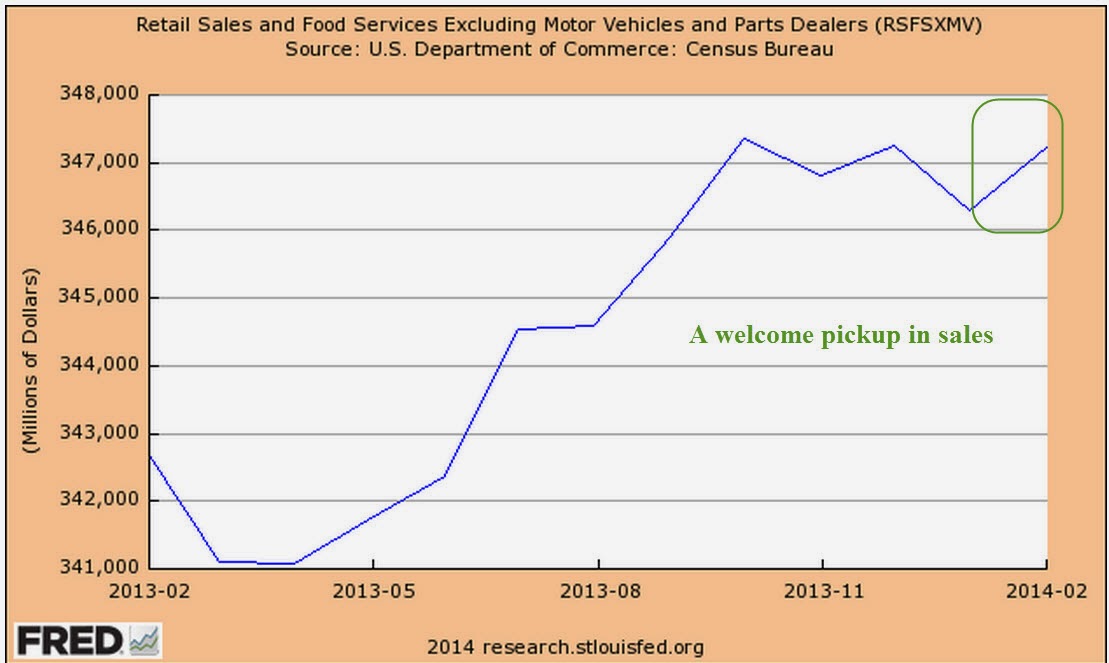

The lackluster small business report early in the week dampened market activity until the release of February’s retail sales report on Thursday. The retail sales and employment reports that are released each month probably elicit the most response from the market. A fall in February’s retail sales might have driven the market down at least 1%. Instead, the report showed an annualized growth rate of 3.6%, offsetting the weakness in January and December. Excluding auto sales, which accounts for about 20% of retail sales, total sales have formed a plateau. Even auto sales were up this past month in spite of the extreme bad weather in parts of the country. Some see this resilience in the face of the extraordinary weather this winter as an indication of an ever strengthening consumer base, a harbinger of solid economic growth.

The reason for the reduction in inventories indicated by the small business survey was revealed by Thursday’s report of the inventory-sales ratio for January. Inventories rose at a 4.8% annualized rate versus a 7.2% annualized decline in sales. January’s ratio of inventory to sales is at the same level as the beginning of the recovery in 2009. Businesses will be cautious buyers this spring until excess inventories are reduced.

****************************

Employment

The number of unemployment claims declined again this week, bringing the four week average down to approximately 330,000, considered by many to be in the healthy range. As a percent of the workforce, new unemployment claims are near all time lows. Enacted in 1993, NAFTA had some small effect on employment but the more consequential impact was the admittance of China into the WTO. As the relatively more volatile manufacturing employment decreased, so too did the surge in unemployment claims. Note the reduced volatility of the work force today compared to the 1980s.

As a rule, employees quit jobs when they feel confident that another job is readily available. The Quits rate has been rising since the official end of the recession in the summer of 2009 but is still relatively weak and declined in January. The current level is at the lows of the recovery from the recession of the early 2000s.

As a percent of the workforce, however, the level of quits has not even reached the lows of that previous recession.

***************************

Income

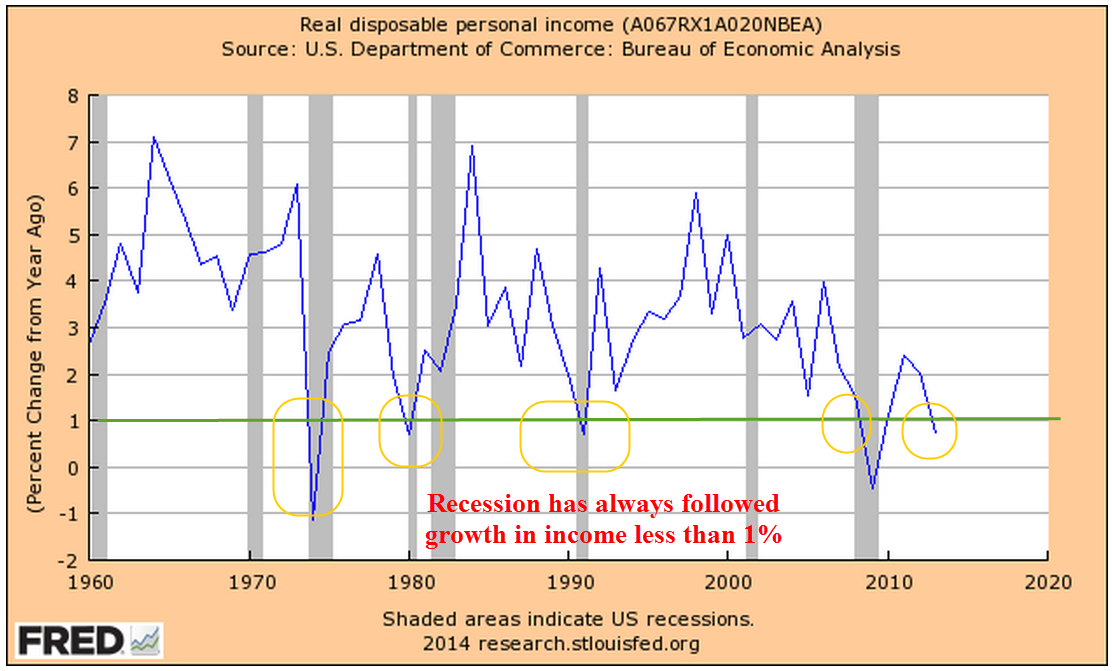

Now for a disturbing trend: the decline in disposable income below 1% has always marked the start of a recession. This annual report from the Bureau of Economic Analysis (BEA) covers the period till the end of 2013 and was not affected by the recent cold weather.

Whenever the growth in real, or inflation-adjusted, personal consumption has declined below 2.5%, the economy has always gone into recession within the year. In 2013, consumption growth fell to 2.0%.

Well, maybe this time is different. Eternal hope, persistent denial. Those of us living in the present too often believe that we belong to an elite club with special rules that those in the past did not enjoy.

**************************

For now, let’s leave out the growth in the disability and Medicare programs and focus only on retirement and survivor’s benefits, or OASI.

The SSA estimates that “By 2033, the number of older Americans will increase from 45.1 million today to 77.4 million.” (SSA Basic Facts) At an inflation rate of 2.5%, less than the 3% average of the past 50 years, the average $14K annual benefit will grow to $23K by 2033. Multiply that by 77 million people and the total of benefits that will be paid to seniors in 2033 is close to $1.8 trillion, almost triple the benefits paid in 2013.