September 14, 2014

This week I’ll take a look at the latest JOLTS report from the BLS and an annual assessment of global financial risks by the Bank of International Settlements.

********************

JOLTS

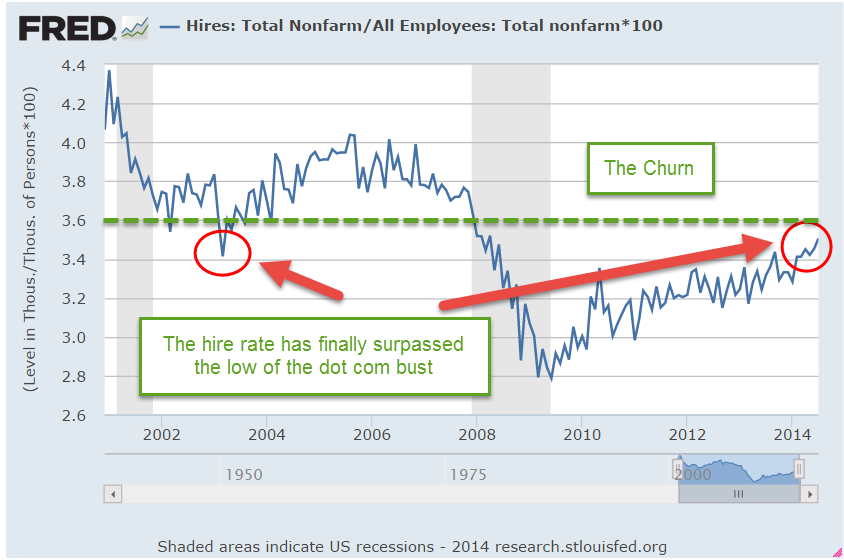

The BLS releases their Job Openings and Labor Turnover Survey (JOLTS) with a one month lag. This past week’s release covered survey data for July. The number of employees quitting their jobs is regarded as a sign of confidence in finding another job. When it is rising, confidence is increasing. The latest survey is optimistic.

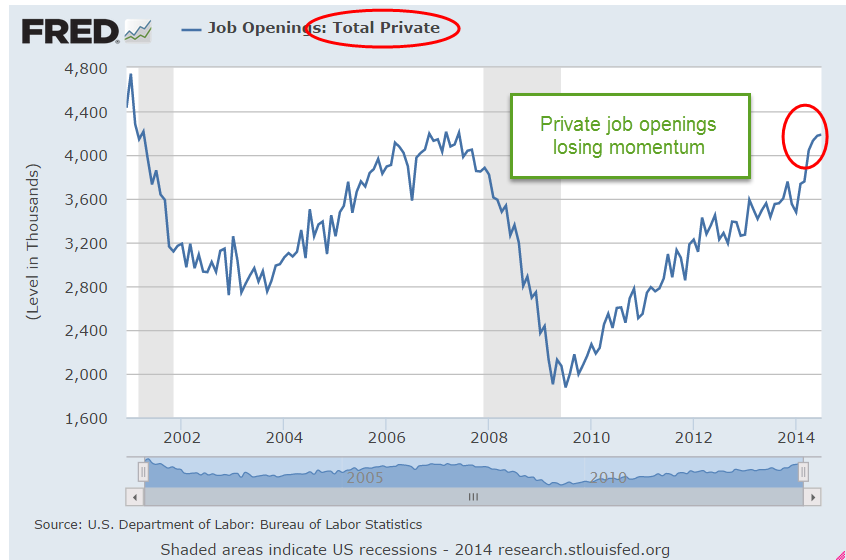

The number of job openings have accelerated since the January lows. In June, they passed the peak reached in 2007.

However, since May, the growth of job openings in the private sector has stalled.

The number of new hires continues to increase but we should put this in perspective. The hire rate, of percentage of new hires to the total number of employees, has only just surpassed the lows of the early 2000s after the dot com bust and the 2001 recession. This “churn” rate is still low, even below the level at the start of the 2008 Recession.

********************

Consumer Credit

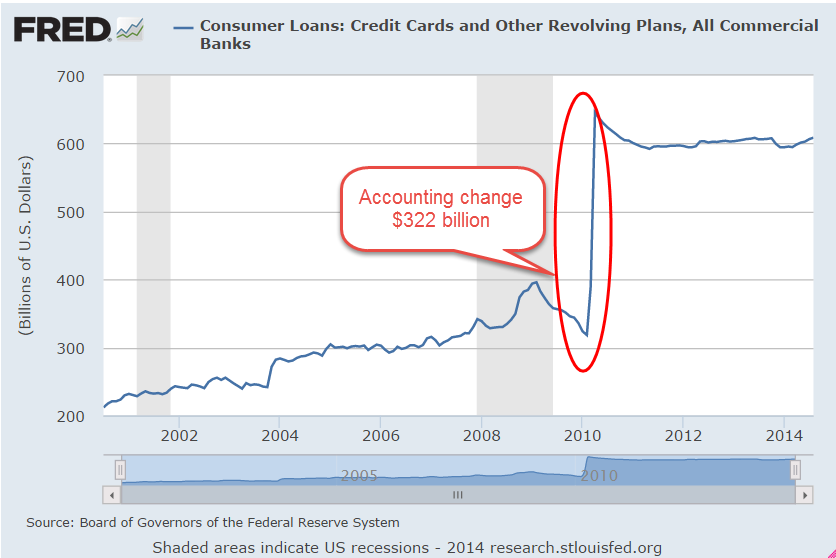

Auto sales and the loans to finance them have been strong but consumers have been slow to crank up the balances on their credit cards. Although the latest consumer credit report indicates that consumers have loosened their wallets in the past few months, the overall picture is rather flat.

*********************

China

China reported growth in factory output that was below all estimates at 6.9% and below target growth of 7.5%. The Purchasing Managers Index, a barometer of industrial production, shows that both China and Brazil are hovering at the neutral mark while the global index shows moderate growth. Home prices in China have fallen for 4 months in a row. As growth momentum slows, the clamor quickens for more easing by the central bank.

*********************

Bank of International Settlements Annual Report

The Bank of International Settlements (BIS) is the clearing house for central banks around the world, including the Federal Reserve and the European Central Bank. It is the central banker’s central bank that facilitates and monitors money and debt flows among the nations. The BIS has cast a particularly watchful eye on Asian economies, who are about 15 years into their financial cycle.

Their annual June 2014 report sounds a word of caution, emphasizing that central bankers should focus more on the financial cycle than the business cycle as they construct and administer monetary policy:

To return to sustainable and balanced growth, policies need to go beyond their traditional focus on the business cycle and take a longer-term perspective – one in which the financial cycle takes centre stage. They need to address head-on the structural deficiencies and resource misallocations masked by strong financial booms and revealed only in the subsequent busts. The only source of lasting prosperity is a stronger supply side. It is essential to move away from debt as the main engine of growth.

In Chapter 4 the BIS notes the high levels of private sector debt relative to output, particularly in emerging economies. In a low interest environment, households and companies “feast” on debt, leaving them particularly vulnerable when interest rates rise to more normal levels. International companies in emerging markets can tap the global securities market for funding and much of this private debt remains off the radar of the central bank in a country’s economy.

Financial booms in which surging asset prices and rapid credit growth reinforce each other tend to be driven by prolonged accommodative monetary and financial conditions, often in combination with financial innovation. Loose financing conditions, in turn, feed into the real economy, leading to excessive leverage in some sectors and overinvestment in the industries particularly in vogue, such as real estate. If a shock hits the economy, overextended households or firms often find themselves unable to service their debt. Sectoral misallocations built up during the boom further aggravate this vicious cycle.

While there is no consensus on the definition of a financial cycle, the peak of each cycle is marked by some degree of stress that encompasses a region of the world and can have a global effect. Emphasizing the global component of financial cycles, the BIS is indirectly encouraging central bankers to communicate with each other. Money flows largely ignore national borders. It is not enough for a central banker to sit back, confident in the sage and prudent policies of their nation. Each banker should ask themselves: what are the neighbors doing that could impact my nation’s economy and financial soundness?

Financial cycles tend to last 15 – 20 years, two to three times the length of the business cycle. It takes time to build up high levels of debt, to lower credit standards and become complacent about downside risks. There may be no clearly identifiable cause that precipitates a financial crisis.

Different regions have different cycles. More advanced western economies have been on a downward recovery phase after the crisis of 2008 while emerging economies in the east are near the apex of their cycle. Asian economies experienced their last peak at the start of the millenium. They have had 15 years to inflate asset and property prices, to lower credit standards and accumulate debt, all hallmarks of a developing environment for a financial crisis.

The report notes that borrowers in China are especially vulnerable to rising interest rates but that many economies in the region would be pushed into crisis should interest rates rise just 2.5%, as they did a decade ago.

*************************

Takeaways

Employee confidence and hiring are strong but private sector hiring may be stalling. The next crisis? Look east, young man.