September 15, 2019

By Steve Stofka

“It’s the economy, stupid,” James Carville posted in the headquarters of Bill Clinton’s 1992 Presidential campaign. The campaign stayed focused on the concerns of middle and working- class people who were still recovering from the 1990 recession. Jobs can make or break a Presidential campaign.

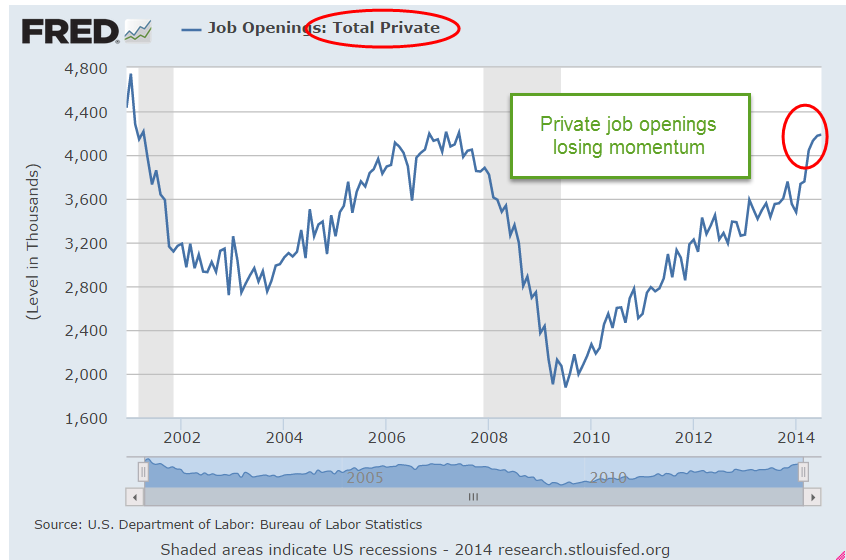

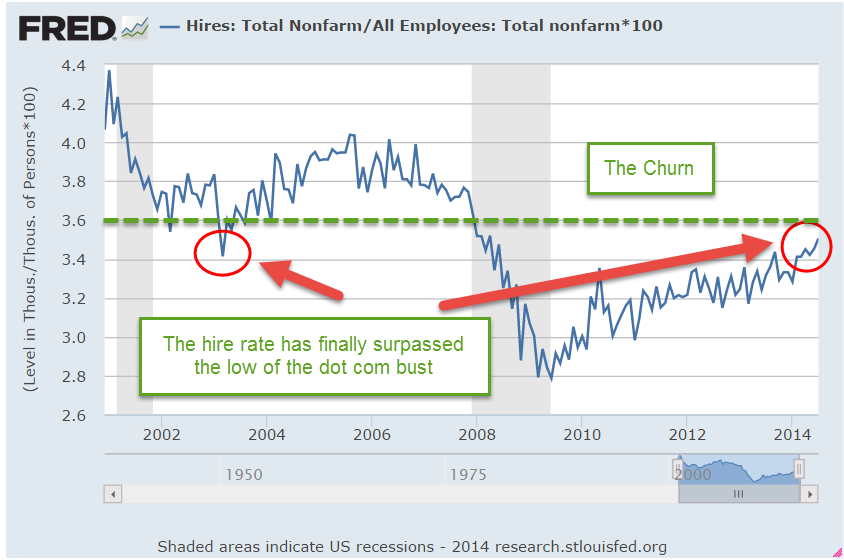

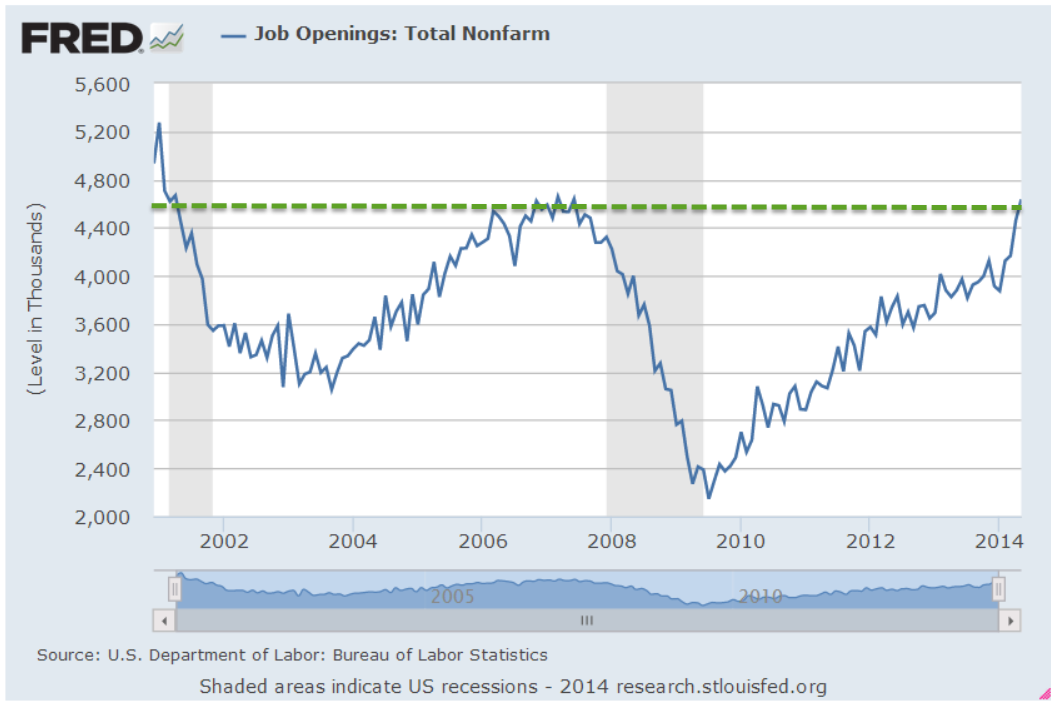

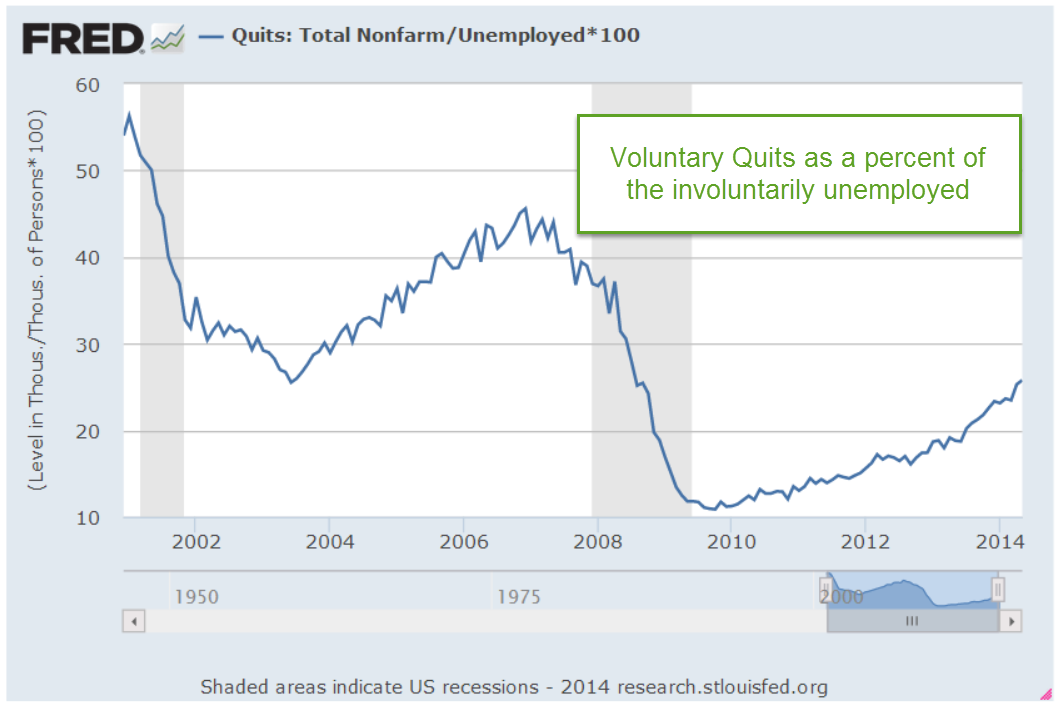

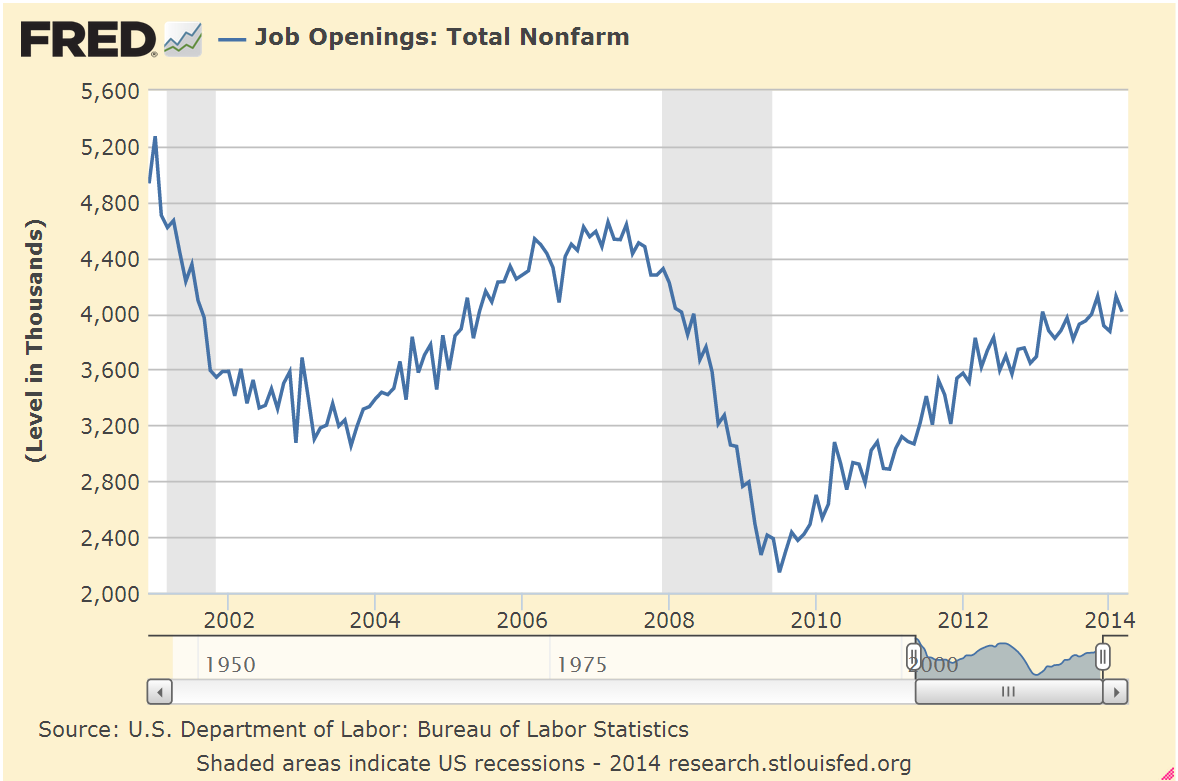

Each month the BLS reports the net gain or loss in jobs and the unemployment rate for the previous month. These numbers are widely reported. Weeks later the BLS releases the JOLTS report for that same month – a survey of job openings available and the number of employees voluntarily quitting their jobs. When there are a lot of openings, employees have more confidence in finding another job and are more likely to quit one job for another. When job openings are down, employees stick with their jobs and quits go down as well.

President Bush began and ended his eight-year tenure with a loss in job openings. Throughout his two terms, he never achieved the levels during the Clinton years. Here’s a chart of the annual percent gains and losses in job openings.

As job losses mounted in 2007, voter affections turned away from the Republican hands-off style of government. They elected Democrats to the House in the 2006 election, then gave the party all the reins of power after the financial crisis.

As the 2012 election approached, the year-over-year increase in job openings slowed to almost zero and the Obama administration was concerned that a downturn would hurt his chances for re-election. As a former head of the investment firm Bain Capital, Republican candidate Mitt Romney promised to bring his experience, business sense and structure to help a fumbling economic recovery. The Obama team did not diminish Romney’s experience; they used it against him, claiming that Romney’s success had come at the expense of workers. The story line went like this: Bain Capital destroyed other people’s lives by buying companies, laying off a lot of hard-working people and turning all the profits over to Bain’s fat cat clients. The implication was that a Romney presidency would follow the same pattern. Perception matters.

In the nine months before the 2016 election, the number of job openings began to decline. That put additional economic pressure on families whose finances had still not recovered following the financial crisis and eight years of an Obama presidency. Surely that led some working-class voters in Michigan, Wisconsin and Pennsylvania to question whether another eight years of a Democratic presidency was good for them. What about this wealthy, inexperienced loudmouth Trump? He didn’t sound like a Republican or Democrat. Yeah, why not? Maybe it will shake things up a bit. Enough voters pulled the lever in the voting booth and that swung the victory to Trump.

In the past months the growth in job openings has declined. Having gained a victory based partially on economic dissatisfaction, Trump is alert to changes that will affect his support among this disaffected group. As a long-time commentator on CNBC, Trump’s economic advisor, Larry Kudlow, is aware that the JOLTS data reveals the underlying mood of the job market. Job openings matter.

Unable to get action from a divided Congress, Trump wants Fed chairman to lower interest rates. There have been few recessions that began in an election year because they are political dynamite. The recession that began in 1948 almost cost Truman the election. The 1960 recession certainly hurt Vice-President Nixon’s bid for the White House in a close race with the back-bench senator from Massachusetts, John F. Kennedy.

In his bid to unseat President Carter in 1980, Ronald Reagan famously asked whether voters were better off than they were four years earlier. The recession that began that year helped voters decide in favor of Reagan.

Although the 2001 recession started a few months after the election, the implosion of the dot-com boom during 2000 certainly did not help Vice-President Al Gore’s run for the White House. It took a Supreme Court decision and a few hundred votes in Florida to put Bush in the White House.

As I noted earlier, George Bush began and ended his eight years in the White House with significant job losses. Those in 2008 were so large that it convinced voters that Democrats needed a clear mandate to fix the country’s economic problems. After the dust settled, the Dems had retained the house, won a filibuster-proof majority in the Senate and captured the Presidency. Jobs matter.

The 2020 race will mark the 19th Presidential election after World War 2. Recessions have marked only four elections – call it five, if we include the 2000 election. An election occurs every four years, so it is not surprising that recessions occurred in only 25% of the past twenty elections, right? It’s not just the occurrence of a recession; it’s the start of one that matters.

Presidents and their parties act to fend off economic downturns with fiscal policy or pressure the Fed to enact favorable monetary policy that will delay downturns during an election. Trump’s method of persuasion is not to cajole, but to criticize and denigrate anyone who doesn’t give him what he wants, including the Fed chairman. To Trump, life is a tag-team wrestling match. Chairman Powell can expect more vitriolic tweets in the months to come. Trump will issue more executive orders to give an impression that his administration is doing something. The stock market will probably go up. It usually does in a Presidential election year.