January 22, 2017

Mr. Trump’s inauguration marks the first time in almost a hundred years that a business person assumes the highest political position in the country. His cabinet choices share that same characteristic. There will be an inevitable clash of cultures. Many civil servants are lifers, drawn to the generous benefits of government service, and the stability of employment. Some may be drawn to the work because it gives them a sense of self-worth.

Many have little experience in private industry and distrust the motives of business owners. Former President Obama was one of these. An inspirational figure to some, his antipathy to business interests of all sizes antagonized political foes who challenged him for most of his two terms.

Mr. Trump has a similar weakness – his antipathy to and unfamiliarity with the insular culture of civil servants who work in a massive bureaucracy characterized by a thicket of rules and a lack of transparency.

Work in the private sector is characterized by competition, a striving for efficiency, the changing winds of people’s preferences, and the quality of the services and products we provide. Employment in the public sector requires patience with burdensome procedure, a tolerance of a heirarchy of both the competent and the undeserving, and a willingness to work in a system that relies less on merit and more on seniority.

What will happen when these two diametrically opposed cultures mix? Stay tuned.

/////////////////////////////////

Obamacare Kaput?

Since FDR began the custom, Presidents have signed executive orders on their first day in office to signify that they are on the job for that portion of the American electorate that put them in office. One of the highlights of Mr. Trump’s campaign was the repeal of Obamacare. Shortly after his inauguration President Trump signed an order stating his intention to repeal the ACA. The order freezes any further promulgation of rules and regulations pertaining to the act. I thought it would be appropriate to republish a blog I wrote in April 2011, a year before the Supreme Court ruled that most of the ACA was constitutional. Like Social Security, ACA premiums and penalties were a tax.

The problems of providing health care and the insuring of that care have not gone away: rising costs, more sophisticated and expensive therapies, more demand for care from an aging population. The problem is a knotty one: how to distribute health care costs. We all benefit from the availability of medical resources, yet these resources are very expensive. The 24 hour care and equipment that stays idle in an urban hospital must be paid for with funds from other parts of the health care system.

It might surprise readers that more than 50% of the $3.5 trillion in Federal outlays is for Social Security benefits ($930B), Medicare ($600B) and Medicaid and Community health programs ($500B). Eighty years ago, FDR initiated a new role for the Federal Government: an economic support system. To do that, FDR had to threaten and cajole a Supreme Court reluctant to stretch the meanings of several clauses in the Constitution.

Even FDR would be appalled to learn that the Federal Government has become an insurance company whose chief function is the collection of insurance premiums through taxes in order to pay insurance claims in the form of Social Security, Medicare and Medicaid Benefits.

Readers who would like to read more on a pie chart breakdown of government spending can visit the Kaiser Family Foundation’s fact sheet. Dollar amounts are from the latest White House budget.

//////////////////////////

MM Bash

I’m about to bash criticize some of the reporting in mainstream media (MM) publications, whose budgets rely on viewership. When that audience was more predictable, flagship publications like the NY Times, Washington Post and Wall St. Journal could wait to verify facts before running a story. In the current 24 hours news cycle and the rush to print, fact checking sometimes comes after the story is published online – if at all.

MM channels rested on their decades old reputations for thorough journalism and were willing to cut off at the knees any reporter compromising that reputation. More than a decade ago, Dan Rather lost his anchor job with CBS for running with a story about George Bush that had not been properly vetted. News (fact-checked) and opinion (not checked) were clearly defined when they were in separate sections of the newspaper. In this new age when most information is delivered digitally, we are quoting blogs or other opinions that are not fact checked as reputable news sources without verifying the information.

A lie travels around the world by the time the truth gets its boots on. Something like that. In today’s lightning fast world of information flow, an apocalyptic news item that can move markets can be tweeted, webbed, facebooked, and retweeted. “China fires on U.S. destroyer in South China sea!” “N. Korean missle hits Alaska!” Sell, sell, sell, buy, buy, buy signals can flash instantly to world markets.

Later, it’s no, China didn’t fire on a U.S. destroyer. China said it would fire if fired on by a U.S. vessel in the S. China Sea. No, the North Koreans didn’t actually fire a missle. Instead they said that they had a missle that could fire a nuclear payload on Alaska. They’ve been saying that for several years. Most defense analysts remain skeptical. Oops, nevermind stock and bond markets.

We can not prevent this, nor can we hide our savings under a mattress. We can prepare by making sure that we have some emergency funds in place. Most financial advisors recommend six months replacement income. Only after those funds are in place should we consider that boat we want on Craigslist or the down payment on that house we want to flip. Don’t just plan to have a plan. Have a plan.

//////////////////////////

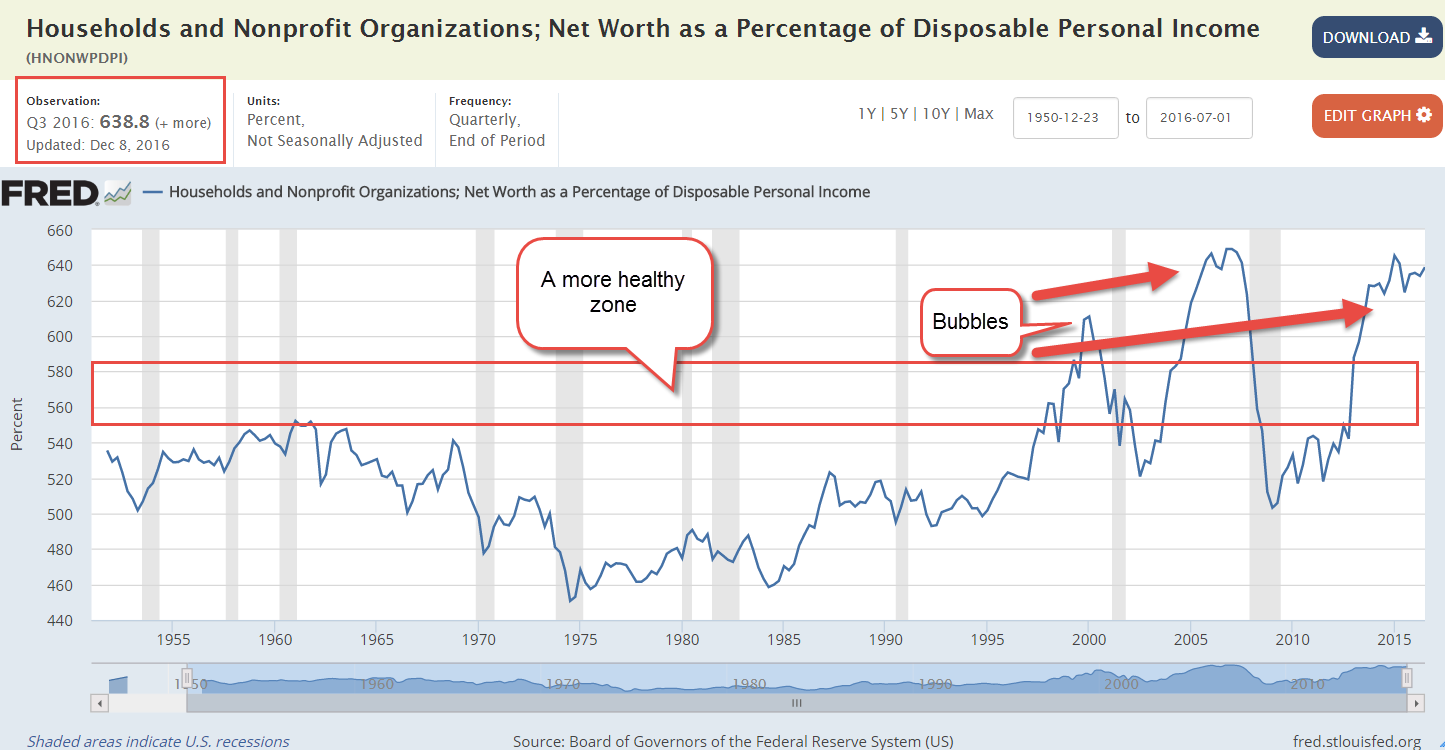

Household Net Worth Ratio

The zero interest rates for the past eight years are not natural and have created distortions in business and residential investment as well as stock market valuations. Let’s look at the residential side of the picture. Below is a sixty year chart of the percentage of household net worth to disposable income.

The majority of the net worth of households is in their home. The value of stocks and bonds comes second. One or both of the two factors in that ratio is mispriced. Perhaps disposable income has not grown to match the growth in asset valuations. When reality doesn’t match predictions for a time, assets reprice.

What affects the pricing of these assets? The stock market rises on the prospect of sales and profit growth. Salaries and wages rise as businesses compete for workers in a faster growing marketplace. Disposable income rises. Home prices rise on the prospect that more workers can afford to buy a home.

Now, what happens when disposable incomes, the divisor or bottom number in this ratio, don’t rise as much as predicted? Yep, the ratio goes up, just as it did in 1999-2000 and 2006-2008, the peaks in the graph.