January 15, 2016

10 Year Review

Before I begin a performance review, I’ll refer to an article on the errors of comparing our real world portfolio returns to the optimized returns of a benchmark index. An index stays fully invested, has no trading costs, taxes or fees. An index has survivor bias; companies that go out of business or don’t meet the capitalization benchmark of the index are effortlessly replaced, so there is no risk. Share buybacks benefit an index but not our portfolio.

The article contains some prudent and realistic recommendations: the importance of preserving our savings, a balance of risk and return that will meet our goals, AND our time frame. As we review the performance of the following portfolio allocations, keep those caveats in mind. If a model portfolio earned 8% per year, use that as a rough guideline only.

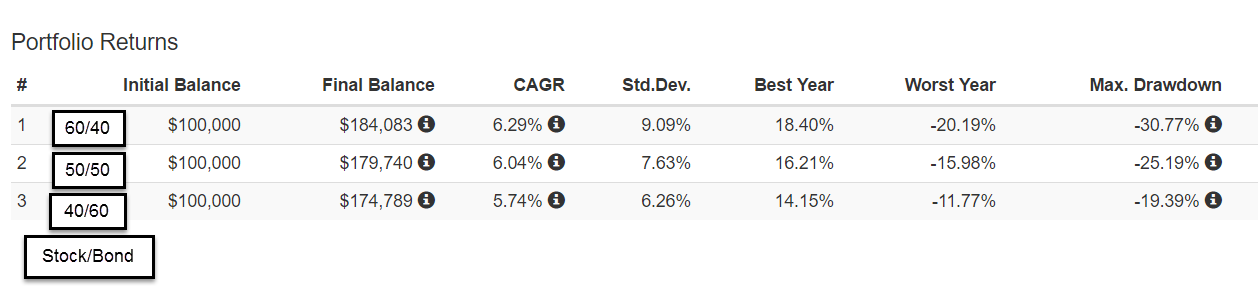

A 60/40 stock/bond portfolio returned an annual 6.3% over the past ten years with a maximum drawdown (MDD) of 30%.

A 50/50 mix returned 6% with an MDD of 25%.

A 40/60 mix returned 5.75% with a MDD of 20%.

A difference of 10% in allocation equalled a .3% in annual return, and a 5% change in MDD. Let’s put that .3% difference in dollars and cents. Over a ten year period, a $100,000 portfolio earning .3% extra return per year equalled about $43 extra per month, or about $1.40 per day. Why is this important? For whatever reason, some people worry more than others and may be willing to accept a lower return in order to sleep better at night.

Not all ten year periods will have the same response to various allocations. The majority of ten year periods will include a recession, but this past ten years included the Great Recession. Let’s look at the historical effect of portfolio allocation during the past ten years. In the chart below you can see the annual returns of various balanced allocation mixes shown in the left column. At the end of 2009, the 10 year results show the results of two downturns: the 2001 – 2003 swoon and the 2007 – 2009 crash.

Note that the more aggressive 60/40 allocation has a lower return than the cautious 40/60 allocation during the years 2009-2011. As we move forward in time, the effects of the 2001-2003 swoon diminish and, starting in 2012, the more aggressive allocation earns a better return.

Not shown in the chart are the results of a 100% allocation to stocks during the ten year period 2000-2009, the first column in the chart above. A 40/60 allocation had a return of 3.8%. A 100% allocation to large cap stocks had a LOSS OF 1% per year.

During the 10 year period 2007-2016, a 100% allocation to stocks returned 6.8% annually, a 1/2% higher return than the 60/40 mix, but the drawdown was 51%, far more than the 30% drawdown of the 60/40 portfolio.

High Winds or Hurricane?

A person who spends twenty years in retirement can count on at least two market downturns during that time. Here’s how MDD, or drawdown, can affect a person’s portfolio. I’ll present a more extreme example to illustrate the point. Imagine an 80 year old retiree with a portfolio devoted 100% to stocks. For several years, she had been withdrawing $40,000 from a portfolio that had a balance of $600,000 in the fall of 2007. Projecting that her portfolio could earn a reasonable return of at least 7% per year, or $42,000, the balance looked secure.

But by March 2009, a period of only 18 months, the high winds had turned to a hurricane. Her portfolio, her shelter in the storm, had lost 50% of its value, an MDD or drawdown of approximately $300,000. During those 18 months, she had also withdrawn $60,000 for living expenses, leaving her with a balance of about $240,000 in the spring of 2009, the low point of the stock market.

Only 18 months earlier she had projected that she could maintain a minimum portfolio balance of $600,000. She had gnawed her nails raw as the market lost 20% by the summer of 2008, then sank in September when Lehman Bros. went bankrupt, then continued to lose value during the winter of 2008-09. When would it end?

In March 2009, she had only 6 years of income left before her savings were gone. Unable to stand the loss of any more value, she sold her stocks for $240,000 – at exactly the wrong time, as it turned out. Her $240,000 earned little in a money market, forcing her to: 1) cut back the amount of money she withdrew from her portfolio to about $24,000 per year, and 2) hope she died before she ran out of money.

Of course, most advisors would NOT recommend that an 80 year old devote 100% of their savings to stocks. BUT, some retirees might – and have – adopted a risky strategy to “whip” a portfolio to get more income or capital appreciation the way a jockey might do with a tired horse. On the other hand, some 80 year olds with a very low tolerance for any kind of risk might have all of their savings in cash and CDs, a 0/100 allocation.

Now let’s imagine that our retiree had a cautious 40/60 balanced mix. She would have had a drawdown of 20%, or $120,000, during the Great Recession. After withdrawals for living expenses, she still had a balance of about $420,000 in March 2009. At a conservative estimate of a 5.5% annual return, she could have prudently drawn down her portfolio $25,000 – $30,000 for a year and waited. This is important for seniors: an allocation that allows some temporary flexibility in the withdrawal amount from a portfolio.

By the end of 2009, her portfolio had gained about 24%. After living expenses of about $22,000 taken from the portfolio during the last 9 months of 2009, she had a balance of more than $500,000. Her balanced allocation allowed her to wait longer for the market to recover.

In 2010, she could once again take her $40,000 living expense withdrawal and still have a $530,000 portfolio balance by the end of that year. She has weathered the worst of the storm. At the end of 2016, she continued to take out $40,000 (adjusted upward for inflation) and still has a portfolio balance of $486,000.

Finally, her 40/60 allocation mix kept to a rule I have mentioned from time to time: the five year rule. If she wanted to take approximately $40,000 from the portfolio each year, she should have a minimum of 5 years, or $200,000 in bonds and cash – the “60” in the 40/60 allocation mix. In the fall of 2007, she had $360,000 (60% of $600,000) in less erratic value investments. This rule helped her withstand the storm winds of the Great Recession.

//////////////////////////

Seniors at Risk

Although the number of loans to those 65+ are less than 7% of the total of student loans, a shocking 40% of these loans are in default. Most of these loans were cosigned by seniors for their children or grandchildren. The law allows the Federal Government to garnish or lien Social Security and other federal payments to cure the loan defaults. Readers with a WSJ subscription can read the article here or Google the topic.

//////////////////////////

Hot Housing Markets

In a recent analysis, western cities rule Zillow’s top 10 housing markets for valuation increases.

///////////////////////////

Take this job and shove it!

The latest JOLTS report from the Labor Dept. shows the highest quits rate in private industry since the housing boom in 2006. Employees confident of finding another job are more willing to voluntarily leave their job, and have driven the rate up to 2.4% from a low of 1.4% in the 2nd half of 2009.

Statista compiles data from around the world, including this revealing tidbit: 26% of jobs in the U.S. are unfilled after 60 days, the highest percentage in the developed world. Germany ranks 2nd at 20%, and our neighbor to the north, Canada, comes in at nearly 19%.

What lies behind this data is a mismatch. Employers may be requiring skills that job applicants don’t have. Job applicants may want more money or other benefits than employers are willing to pay.

//////////////////////////

Obamacare Repeal

The Committe for a Responsible Federal Budget (CRFB) – yep, it’s a mouthful – has projected costs to repeal Obamacare in whole and in part. Using both conventional, or static, budget scoring and dynamic scoring (google it if you’re interested), they guesstimate a 10 year cost of $150 to $350 billion for full repeal of the ACA.

Repeal of ACA’s insurance coverage would actually save a lot of money, more than $1.5 trillion. The net effect is a cost, not a savings, because of the $2 trillion in tax revenue on higher incomes that is built into the ACA law.

CRFB analysts have put a lot of work into these projections, including a breakdown of repealing just parts of Obamacare or delaying repeal of certain ACA provisions. Since the Republican Congress is likely to keep some provisions, readers who are interested might want to come back to this link in the coming weeks as the discussion of this issue unfolds.