June 25. 2017

This week I will review a decade of change to help illustrate a fundamental fact about investing: most of us are clueless about the future because we are bound by comfortable habits of thinking.

Ten years ago this month, June 2007, Apple launched the iPhone. The touch screen was innovative but I found the keyboard had a lack of responsiveness. The ability to use the internet was cool but the connection was slow. There was no camera built into the phone. Cameras took pictures, not phones. Apple did not introduce the App Store till July 2008 so users got whatever Apple thought they needed. Apple controlled both the hardware and software. People stood in line when the first phone was released because Apple people are a little bit nuts. The phone was suitable for geeks who had money to burn. Or so it seemed.

Phones were tools, not toys. People who used their phones for work used a Blackberry, a phone with a keyboard that kicked butt over the iPhone and had a great email interface to boot. The low cost workhorse phones were Nokia models. They stood up to daily wear and tear and the little screen was adequate for reading text messages.

The previous year, a relatively new company called Facebook notched 12 million monthly users (Guardian) and their user count was growing fast. Facebook was a social networking site for people who had time on their hands and the desire to connect with their friends. A passing fancy for the kids, no doubt, just like rock and roll was to an earlier generation of parents. Or so it seemed.

That same year, the internet search company Google developed a beta version of a phone operating system (OS) that could compete with Apple’s iOS. In the fall of 2008, a year later, Google released version 1 of the OS. It was built with an open source code that Google called Android. That same month, the wheels came off the global economy. As millions of people lost their jobs, they worried more about paying their bills than a phone operating system. By November 2008, both Google and Apple had lost half of the value they had in the summer. Blackberry lost 2/3rds of its value.

In June 2009, two years after the launch of the iPhone, the electronics division of the conglomerate Samsung introduced the Galaxy smartphone. The phone used the new Android OS and, to compete with Apple’s App Store, hundreds of apps were available for the phone.

Clickety-click as we turn the time dial to the present. At $10, Blackberry’s stock sells for 7% of its price in June 2008. Hillary Clinton likes her Blackberry but too many people switched. Until the fourth quarter of 2016, Samsung sold more phones than Apple, but Apple makes more profit on their phones and is the largest company by market capitalization. Since the iPhone launch Apple’s stock price has soared 900%. Together the two companies account for almost half of all smartphones. They have become wearable computers and cameras and music players and podcast devices.

The iPod was the marriage of a CD player and a portable radio – a consolidation of two functions. Following its introduction in 2001, the iPod became the dominant music player. Umpteen million songs were available on the device through the iTunes store. In April 2007, Apple announced that they had sold 100 million iPods in 5-1/2 years, and by the end of 2014, that figure stood at 390 million. But smartphone users were now using their phones to play music. In 2014, sales of the iPod fell by half to 15 million. In 2015, Apple stopped reporting the number of iPods sold. Consolidation had been the key to the iPods success and its demise.

The iPhone and the various Android models of smartphones have depended on increasing network availability and quality – “can you hear me now?” – and the thousands, or millions, of apps available for the phones. I can read email on my phone as well as my newspaper, a book or magazine. Students can read their textbooks on their phones. In addition to music, I can listen to podcasts or radio stations from far away.

The sophistication and accuracy of Google maps is science fiction made fact. I was recently in the middle of beautiful Idaho. The topographic map published a few years ago indicated that a particular county road was improved but unpaved. Google maps marked the road as paved for about ten miles. Google was right. Portions of Nevada that were blurred a few years ago on Google maps now show roads that lead to where? Maybe some alien city in the middle of the desert.

As I mentioned last week, the top 5 companies in the SP500 are tech companies. Ten years ago, the top 5 were Wal-Mart, Exxon, GM, Chevron and ConocoPhillips (Fortune), a mix of retail, automotive and oil sectors. Now there is only one sector at the top: technology. As a rule, concentration is not a good thing.

Let’s turn from tech to banks. Since 2007, America has lost a third of its banks, a continuation of a trend that began after the Savings and Loan crisis in the late 1980s. The number of commercial banks in the U.S. is about a third of what it was in 1990. New York has lost half of its banks in that time. California has lost about 60% of its banks. You can check your state at the Federal Reserve Database and search for [postal abbreviation for state]NUM. As an example, Colorado is CONUM. New York is NYNUM. California is CANUM. The U.S. figures I mentioned earlier come from the series USNUM.

Consolidation is spreading throughout the economy. In the last 12 months, more retail stores closed than during 2008, the year of the financial crisis. The stocks of the retail sector (XRT) have fallen 20% from their highs.

Adding to the pressure on brick and mortar retail stores, Amazon recently announced that they were buying Whole Foods. Amazon’s sales have grown by more than 1000% since 2007, and America’s stores have felt the pain.

The consolidation in the retail space has been going on since the 2001 recession and the demise of the dot-com boom. The population has grown 14% since then but the number of employees in retail has grown less than 3%. Inflation adjusted sales per employee have grown by 61% in the past 16 years but the inflation adjusted wages of retail workers have declined 1%.

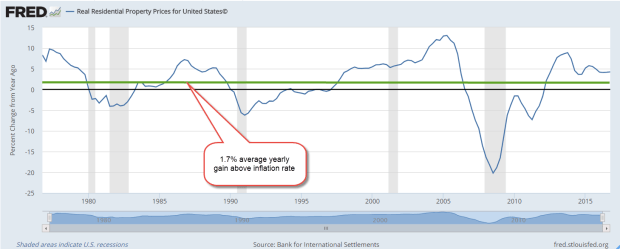

We ourselves are concentrating. For the first time in the nation’s history, more people live in urban areas than rural areas. That concentration has pushed home prices up in the larger metropolitan areas. The S&P/Case-Shiller 20 city home price index has doubled since 2000, easily outpacing the 45% gain in prices, averaging 2% better than inflation.

Smaller cities and rural areas have not done as well. Below is a 40 year chart of inflation adjusted residential prices for all of the U.S. The average yearly gain is 1.7% above the inflation rate, slightly below the 20 city gains of the past 16 years. But the ten year average tells a story of crisis, erratic recovery and migration. The 20 city price index has lost only 1/4% per year since the highs of 2007. The country as a whole has lost 2% per year.

(Sources: National sources, BIS Residential Property Price database)

Where will this consolidation lead?

Less competition

Less responsiveness to customer needs

More political power to create a regulatory environment which guards against competition.

//////////////////////////////

Performance

Mutual funds and ETFs usually specify their historical performance for several time frames, i.e. 1 year, 3 year, 5 year, 10 year, Lifetime. Four years ago, I noted the diffiiculties of getting a reasonable appraisal of performance if the comparison period begins with a trough in price and ends near a peak.

It is best to disregard the five year performance of many large cap stock funds this year because they include the 13% gain of 2012 and the 33% gain of 2013. A more honest appraisal is the ten year performance. Comparisons start in 2007, near the highs of the market before the start of the 2007-2009 recession and the financial crisis.

Vanguard’s SP500 index fund VFINX reports a ten year average annual return of 7.39%. Their blended corporate bond fund VBMFX has an annual return of 4.12% over the past ten years. If I had nothing but these two funds in my portfolio since 2007, my portfolio of 60% stocks, 40% bonds would have gained about 6.1%. With a conservative allocation of 40% stocks, 60% bonds the annual return was about 5.5%. The .6% percent difference in returns is slight but it adds up over ten years. In the first case, a $100,000 portfolio would have grown to $181,000. In the second case, about $171,000.

Let’s compare those returns to two actively managed blended funds that Vanguard offers. VWINX is a balanced fund oriented toward income. The mix is about 40% stocks, 60% bonds and it has earned 6.7% per year over the past ten years. The Wellington fund VWELX has a mix of 65% stocks, 35% bonds and cash and earned 7.13% each year since 2007. Both funds have fees that are slightly higher than Vanguard’s index funds but are relatively low at .22% and .25%. Depending on allocation preference, either fund could serve as a core “gone fishing” fund. You can use these as a basis for comparison with products that your fund company offers.

Next week I’ll put my ear to the ground and listen for….