September 3, 2017

Hurricane Harvey invaded the lives, homes and businesses of so many people in Houston and the surrounding area of southeast Texas. People around the world watched the plight of so many who were caught in the rising waters. I was cheered by the dedication of first responders, by those who came from near and far to help with their boats, with food and clothing. I have never been in a flood. Some of those interviewed had been in several. Why do they stay there, I wondered? The answer is some or all of these: their family, their church, their job, their school, their culture.

Watching so many vulnerable people reminded me of my own. If given a few minutes to leave my house, what would I put in a garbage bag? In the urgency and stress of the moment so many people in Houston forgot their medications. My list: Pets, papers, clothes, medications. Food? Will the shelter have food? Pet food, as well? Where are we going? Oops, what about a phone charger? And the laptop. What about the list with all the passwords? That too. What about the photos in the closet? I was going to get those scanned in and uploaded. No time now. Take a few of the smaller framed photos on the shelf in the living room. Out of time. Gotta go. All the questions that must have been bouncing around inside the heads of those forced to evacuate as the brown water took possession of their house.

If I don’t call it Climate Change, I could call it Flood Frequency, or Flood Freak for short. Here is a chart showing the increased frequency of flooding during the past century. This was from an article in the WSJ (paywall).

This week’s theme – vulnerability. The signs of it and what we can do to lessen it. Debt is a vulnerability. For the past three years, households have been increasing their debt load in mortgages, auto and student loans. Here’s a breakdown of household debt from the NY Fed. (As a side note, this report gives a breakdown of the different types of debt by credit score. For example, the median credit score for an auto loan is about 700).

Mortgage debt is more than 2/3rds of total debt. Despite the rise in home prices, more than 5 million homes, or 7%, are still badly “under water.” (Consumer Affairs)

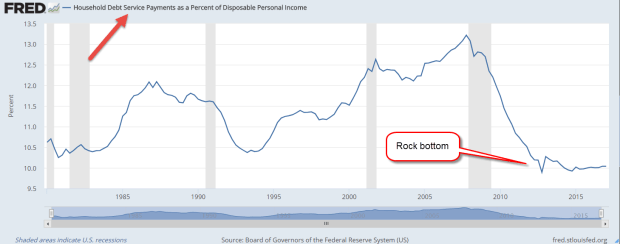

Credit card debt has stayed stable for the past thirteen years. Households are only using 10% of their after-tax income to service their debt.

Despite low interest rates, households are continuing to deleverage, to decrease their vulnerability. The ratio of household debt – the total of that debt, not the payments – to income climbed above 2.5 in late 2007. It has fallen below 2.2 but is still high. We are still up to our eyeballs in debt.

Debt reduction will curb economic growth for the near future. According to several cabinet members, Trump is focused on GDP growth in discussions about trade policy, defense policy, infrastructure spending, and the regulatory environment. How does this or that policy get us to 3% growth? he asks.

2/3rds of the nation’s economy is based on the public willingness to spend money. Jobs helps. Higher wage growth helps. Low interest rates help. But without the willingness to take on more debt relative to income, policymakers may feel like they are trying to goad a stubborn mule to go faster. Tough to do.

//////////////////////////////////

Unemployment

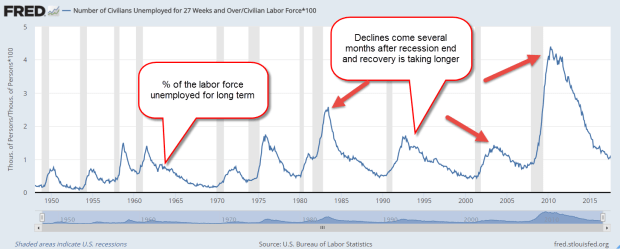

Continuing the theme of vulnerability. As a percentage of the unemployed, the number of long-term unemployed remains stubbornly high at close to 25%. I call them the 27ers because 27 weeks of unemployment is the cutoff that the BLS uses to determine whether someone is categorized as long term unemployed. 27 weeks or six months is a long time to be actively looking for work and not finding a job. Eight years after the end of the recession, today’s percentage of 27ers is at the same level as the worst of most past recessions.

During any recession the number of long term unemployed climbs higher. When these past few recessions have ended, the number of 27ers doesn’t start to decline. Instead, they continue to increase and reach a peak several months after the recession is officially over. In the last three recessions, the peaks came later than previous recessions.

This more vulnerable cohort in the labor force struggles to recover after a recession. Manufacturing is the more volatile element in the business cycle. As manufacturing has declined, recessions are less frequent. However, manufacturing used to put a lot of people back to work at the end of recessions. In a recovery, the service sectors are not as quick to add jobs.

The structural shift in the labor force will continue to leave more workers and families vulnerable and needing help just as many older workers are claiming retirement benefits. More than half of voters, both Republican and Democrat, have received benefits from at least one of the six entitlement programs (Pew Research). Elected officials offer promises of future benefits in exchange for taxes, and votes, today. When circumstances force a clash of priorities and promises, Congress seems incapable of resolving the conflict. President Trump’s approval ratings are in the low thirties, but his popularity far exceeds the public’s dismal ratings of Congress.

In a crisis, Americans come together to help each other but why do we wait till there is a crisis? Have we always been a nation of drama queens? Maybe that’s the American charm.