August 11, 2019

by Steve Stofka

I had some whole hazelnuts left over and left them out for the squirrels. They smelled them, tried to bite them, gave up and buried them in the ground. No surprise there. Squirrels bury food. But that got me to wondering. Do hazelnuts soften after a few weeks in the ground? If so, then that might be an indication that squirrels have some primitive notion of future time. I buried a few hazelnuts in the garden and dug them up this week. Still as hard as they were when I put them in there. Maybe two weeks is not long enough.

We bury money, not nuts. We put it in banks and other institutions called “financial intermediaries” and hope that our savings grow into a big money tree over time. Our bank, mutual or pension fund sends us statements every month or quarter and tells us how big our tree has grown. Financial advisors caution us not to go out and look at our money tree every day. Why? Because sometimes the wind comes and breaks a few branches.

This past Monday was a bit windy. In response to escalating trade tensions, the Chinese yuan weakened in the global money market, and the Chinese central bank did not intervene as the exchange rate dipped below a key number of 7 yuan to the dollar. President Trump accused the Chinese of manipulating their currency because they had taken a free market approach much like the U.S. does. That’s the upside down world we live in now. If the Chinese don’t manipulate their currency, they are guilty of manipulating their currency.

The popular Dow Jones index dropped 3%. How much is that? A little perspective might help. The financial crisis began when investment firm Lehman Brothers went bankrupt on September 15th, 2008. The stock market dropped 4.4%. A dip below a key number in the money exchange rate between China and the US was all it took to drive the market down a remarkable 3%. In short, the market is extremely sensitive right now to information. Don’t look at your money tree. Some of the branches have been broken.

How do the banks and pension funds grow our money trees? They loan the money out to people and businesses who need it. Unlike nuts and seeds, money doesn’t grow when left in the ground. Growth during the past decade of recovery has been slow but unemployment is at 50-year lows so demand for consumer credit is high – credit card rates are the highest in 25 years – over 17% (Note #1).

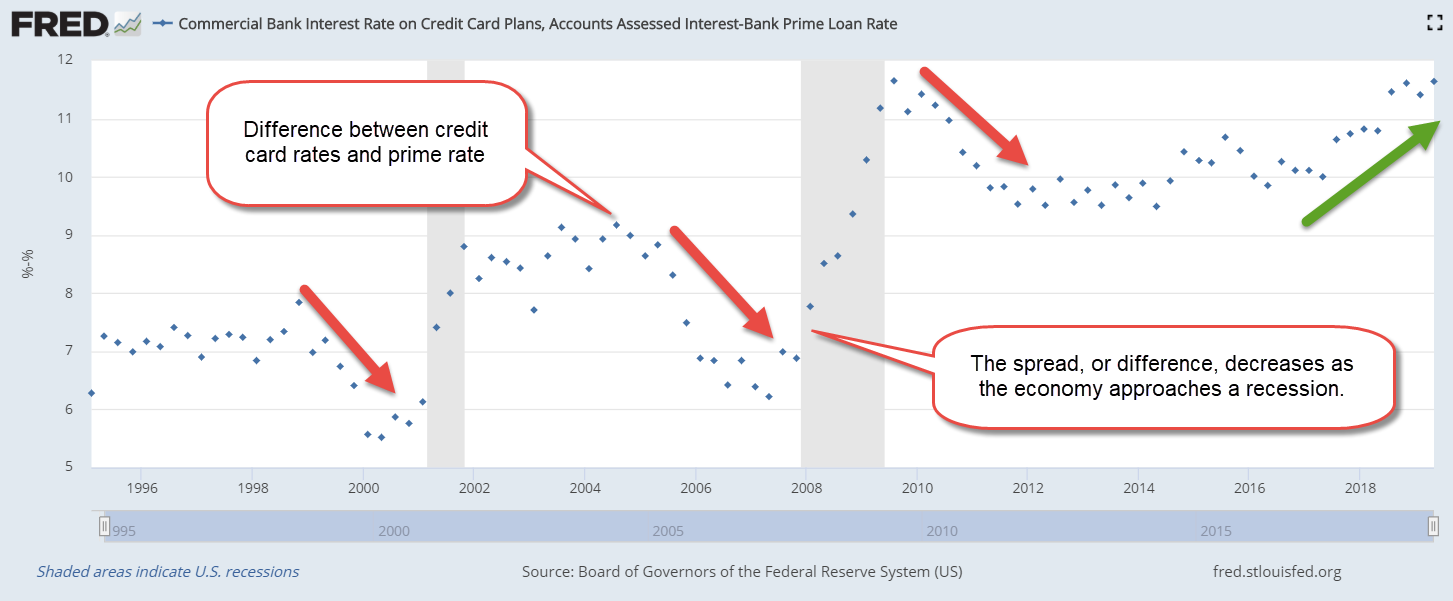

Here’s a graph showing credit card rates (the blue dots) and the prime rate (red line), the rate that banks charge their best business customers.

Here’s a chart of the spread or difference between the two rates. Notice that the spread decreases a few years before a recession actually occurs or banks get increasingly worried about a recession. Banks were already telegraphing their fears two years in advance of the 2008-09 recession.

As you can see, the current spread is increasing, not decreasing. Banks are not worried about getting paid because the economy is strong, and people are working. Credit card defaults are near all-time lows (Note #2). Interest rates are the price of money – the price of time. Banks are confident that they can raise their prices for people who want to borrow money.

Less than two weeks ago, the Fed cut interest rates for the first time in a decade. Chairman Powell cited concerns about global growth and warned that the market should not expect further cuts unless data justified such action. He called the ¼% rate cut a mid-course correction.

Conflicting signals – the “yes, buts” – drive market volatility higher. The economy is good. Yes, but the global economy is weakening.

Wage growth is slow. Yes, but unemployment and delinquencies are very low. Housing costs are through the roof and people won’t be able to keep up their payments. Yes, but annual increases in housing costs for the whole country are only 2-1/2 to 3%, the same as they were for most of the 90s and early 2000s (Note #3).

The yield curve recently inverted, meaning that short term rates are higher than long term rates. Yes, but workers in the retail industry are particularly vulnerable and their real weekly earnings are still rising (Note #4). The yes, buts.

As children we were told to go to sleep and we may have said, “yes, but I saw a spider on the ceiling, and I don’t want it to eat me while I’m sleeping.” It’s just a trick of the light, now go to sleep. “Yes, but I heard a mouse under the bed. What happens if it gets under the covers?” That’s just the wind outside, now go to sleep.

Not once did we worry before going to sleep, “Yes, but what about my piggy bank?” That’s what some of us do as adults. “Yes, but what if the financial crisis comes again and uproots my money tree and carries it up into the sky?” we ask. Close your eyes, now. Don’t listen to the market noise. It’s only the wind. Don’t look under your financial statement every minute for mice and bugs.

///////////////////////

Notes:

- Highest credit card rate in 25 years

- Credit card delinquency, FRED series DRCCLACBS

- Housing costs, FRED series CPIHOSNS

- After adjusting for inflation, median weekly earnings of full-time retail workers have risen 10% since the end of the recession. Annual earnings of $33,000 (in 2018 dollars) are far below the median $45,000 for all workers.