February 14, 2021

by Steve Stofka

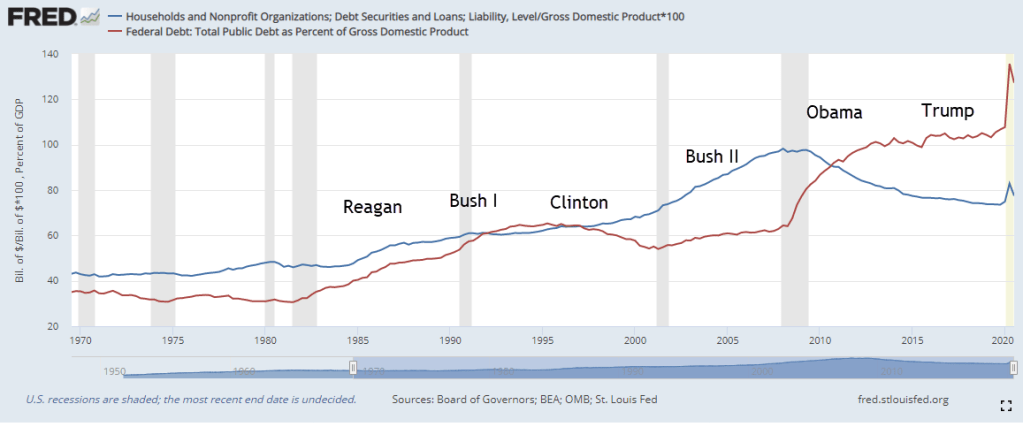

Since WW2, households have traditionally held more debt than the federal government as a percent of GDP. I’ll call it %Debt. The biggest component of household debt is mortgages, and includes car loans, student loans, credit card debt, etc. A decade ago, Federal %Debt surpassed households, effectively allowing households to reduce their debt level and put it on the federal balance sheet.

Federal debt spiked during the pandemic while household debt levels have risen only 1.5%. For decades, deficit hawks have long warned that rising federal debt levels could cause an economic implosion that would make the Great Depression look tame by comparison. They may be right – finally.

There are two ways that the federal %Debt can go down. The first is to grow the economy; that’s the GDP in the denominator of Debt / GDP. The second way is to reduce the level of Debt, the numerator. It is unlikely that Congress is going to raise taxes enough to reduce the debt, so that leaves only one way to reduce %Debt – grow the economy faster than the growth in federal debt.

To do that, consumers need to spend money because their spending makes up 70% of GDP. There are three ways to increase spending. The first is to increase incomes faster than economic growth but that has not been happening for several decades. The real growth in middle class incomes over the past 30 years is only 15%, or 1/2% per year average.

The non-partisan Congressional Budget Office projects that total incomes will increase by an average of $33B per year over the next decade if the minimum wage is raised to $15 over the next five years (CBO, 2021). That increase of 1.5% in GDP will not change the federal %Debt by much.

The second way to increase GDP is for consumers to take on more debt. A rise in housing prices has lifted the net worth of many households, who can tap into that equity to increase their spending. However, households are already choked with debt. The two largest generations, the Millennials and the Boomers are offsetting each other’s spending. Older Boomers are reducing spending as Millennials increase their purchases. The Millennials have been crushed by the financial crisis a decade ago and again with the Covid crisis. Many feel like they came along at the wrong time in history and are cautious. When consumers pay down debt, they spend less and that lowers GDP growth.

The third way is probably the trend of the future. The federal government will continue to pile debt on its balance sheet and shift income onto households in the hopes that consumers will spend money and grow the economy faster than the rise in federal debt. There is a concept called the multiplier and economists argue over its value. It is the total effect of spending in an economy when the government spends $1. That depends on consumer and business confidence, which depends on the amount of debt each sector holds. The IMF estimates that the multiplier is about 1.5, so that $1 of spending equals $1.50. If so, deficit spending might grow the economy faster than the federal debt grows.

I’ll return to a proposal I discarded earlier – increasing taxes, particularly on the top 10% who don’t spend as much of their incomes on consumer goods as the bottom 90%. Under the Budget Reconciliation rule in the Senate, the Democrats could pass tax legislation that undoes the 2017 tax cuts that the Republicans passed using that reconciliation process. In his campaign proposals, President Biden limited any tax increases to those making $400,000 or more, a small sliver of the population.

Income distribution is skewed toward the upper 5%, who will fight vigorously to keep what they have. They will complain – and they have a point – that they are already paying higher taxes in the form of lost income because interest rates are so low. Those with savings are being paid a paltry amount in interest but the low rates reduce the interest on the debt that the federal government pays each year. Boomers on fixed incomes are having to reduce their savings faster to meet monthly expenses.

The structure of income distribution is weak. No, it’s not a problem with capitalism, as some like to claim. This is a problem with political policy which pre-dates capitalism. A small group of people in a nation take command of the distribution levers and direct more of the nation’s income to themselves. In the 1700s, the problem was thought to originate with monarchy and aristocracy. Democracy was going to cure the problem, but it didn’t. Communism was going to cure the problem and it didn’t. Socialism – the middle way between capitalism and communism – was going to solve the problem, but the EU demonstrates that socialism simply slows growth, increases structural unemployment, and does little to solve the persistent problem of distributional inequalities.

Governments worry about exogenous factors like Covid, war, or a dramatic shift in commodity prices. While those do produce crises, they do so because of endogenous factors – weaknesses in a nation’s political and economic system that award property rights in such a way as to exacerbate social tensions. The Great Depression and Financial Crisis were examples.

Since the Financial Crisis a decade ago, people in nations around the world have been raising their fists and their voices. The productivity gains that capitalism promoted had ameliorated the centuries old problem of political oligarchies, but no economic system can solve what is fundamentally a political problem.

Those who voted for former President Trump in 2016 did so thinking that he was a political outsider who could “drain the swamp,” i.e., bust up the political oligarchy that controls Washington. He became part of that oligarchy, feeding the monster, because it relied on his lack of political expertise.

Those who voted for President Biden hope that his decency and moderation will help craft legislation that unlooses the grip that the oligarchy has on our political process. Which wires do we pull to disconnect the oligarchy?

///////////////

Photo by Victor Barrios on Unsplash

Congressional Budget Office (CBO). (2021, February 08). The budgetary effects of the raise the Wage act of 2021. Retrieved February 13, 2021, from https://www.cbo.gov/publication/56975

Tax Policy Center. (2020, May). What is reconciliation? Retrieved February 13, 2021, from https://www.taxpolicycenter.org/briefing-book/what-reconciliation