February 21, 2016

Capitalism

Growing income inequality, and extreme disparities of wealth in a capitalist economy prompted this 2013 speech by David Simon, the writer of the HBO series “The Wire.” Mr. Simon attributes the plight of an economic underclass to thirty years of unrestrained capitalism.

Simon confuses capitalism with politics. When the politicians and agencies in Washington amass ever more power and draw corporate lobbying money to Washington, that’s politics, not capitalism. When taxpayers bail out big banks for making stupid bets, that is politics, not capitalism. When large companies like Archer Daniels Midland and Exxon receive generous subsidies from taxpayers, that is politics, not capitalism.

Cronyism contaminates whatever political or economic system it infects, be it capitalism, socialism, communism or fascism. Cronyism and factions have infected every human society from the Assyrians of 4500 years ago to the present. Knowing how destructive these twin human traits were, James Madison, chief constructor of the U.S. Constitution, crafted a system of checks and balances to provide a legal boxing ring for the various factions to punch it out.

Simon sees the economy as a Manichean battle between capital and labor, a model first proposed by Marx. The battle is more accurately described as a triangle of capital, labor and political power. Capital and labor are the two productive components of the economy, vying for legal favors from politicians. Capital and labor must push and shove for a more advantageous place in a courtier’s line before the political princes and princesses, kings and queens in the capitols of the world.

With much of the productive capacity of the world weakened or destroyed by World War 2, most of the world’s capital flowed to the U.S., which became the economic engine of the world. With little global competition, workers in the U.S. had strong bargaining power, able to win pay packages of $200,000 (in 2015 dollars) to install parts on an assembly line. Public labor unions flexed their legal bargaining and striking power to win pension packages that paid them almost full salary for the rest of their lives.

With few challenges from the rest of the world, management at U.S. companies became undisciplined, unfocused and uncompetitive. The big three automobile manufacturers influenced politicians who passed tariffs which protected the vehicles produced by those manufacturers. Tariffs on imported pickups and cargo vans still insulate domestic manufacturers from competion. Like the automobile manufacturers, aerospace companies like Lockheed cracked under the weight of inept business planning and execution. The demands of their labor force added to the strains. Crippled by chronic cronyism, New York slid into bankruptcy and sought a bailout from the Federal government.

In the 1950s and 60s, I grew up in a union family, in a union neighborhood in New York City. I accepted the nepotism and bribery in the union shops where I worked. They were a fact of life along with housing segregation and sex discrimination. The building trades were riddled with union cronyism and “tips” to building inspectors. Repeated strikes by city workers made daily life unpleasant. Trash piled up in the streets, mass transit didn’t work and it could take an entire day at City Hall to renew a driver’s license.

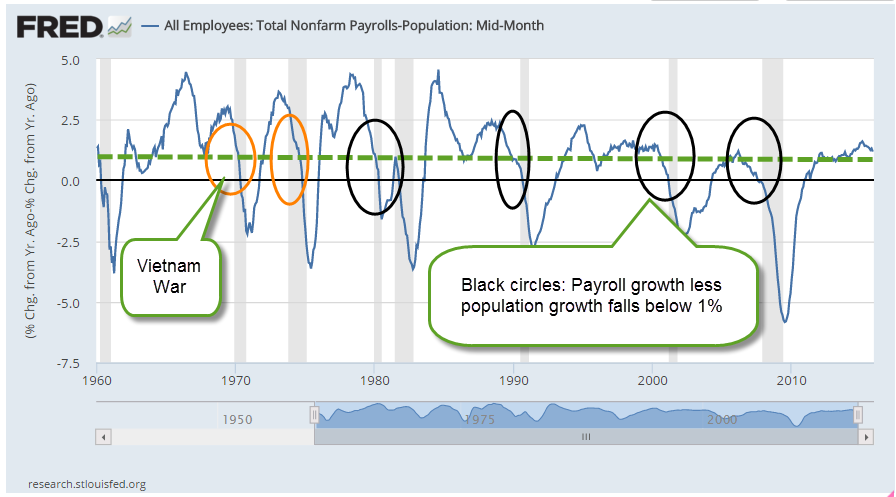

In the 1960s and 70s, whole sections of New York, Chicago, Detroit and Philadelphia were unsafe to walk in, to live in or to work in. Folks like radio and TV host Tom Hartmann and Senator Bernie Sanders find it convenient to leave out some history when they talk about the 60s and early 70s as a benchmark of fairness for working people.

In the 1970s, the problems of the past two decades were brought to a head by the oil embargo, the recession of 1973-74, wage and price controls, the Watergate scandal, and rising inflation that would near 10% by decade’s end. In 1971, Lockheed was bailed out by the U.S. government, a precedent that would be followed by others in the coming decades.

As European countries continued to rebuild their manufacturing and financial capacities, Japanese manufacturers took advantage of a new technology, transistors, to build smaller and less expensive electronic TVs and radios. Their automobiles posed a weak but growing challenge to the dominance of U.S. manufacturers. In 1979, the three cronies of U.S. capitalism – organized labor, capital and politics – renewed their pact when Congress bailed out the automobile manufacturer Chrysler.

In the 1980s, the financial industry, the “bookies” of capitalism, began a decades long courtship of politicians in Washington, competing with organized labor and capital for political favors. The decade began with back to back recessions, 8 – 10% interest paid on savings accounts, 9 – 10% mortgages (a deal!), and small business loans at 14% (secured), or 21% (unsecured) interest rates. Small business owners worked extra hard to compensate for the high interest rates paid on business loans.

Several Social Security tax increases were passed, taking an every bigger bite out of paychecks and profits. A lot of us muttered about taxes. There were 10 to 15 tax brackets, none of them indexed for inflation so that most of a raise or some occasional overtime went to Uncle Sam. For decades, fat cats had been using tax dodges – legally – to escape taxes.

Sensing a growing discontent among voters at the unfairness of the tax system, politicians deliberated for several years before passing a tax reform bill in 1986. Although tax rates were reduced for the wealthy, they lost many of their tax shelters. Any change impacts both the incompetent and the dishonest, but especially exposes those who are both incompetent and dishonest. The loss of tax shelters revealed a large network of scams in the financial and real estate industries that ignited the Savings and Loan Crisis of the late 1980s and early 1990s.

Declining union membership coupled with the growing political influence of the financial industry meant that unions could no longer afford to keep up with capital in the scuffle for treats from Washington. Politicians protest that they too are victims of the “pay to play” system of American politics but efforts to enact a system of public financing of elections have been unsuccessful. Why? Because the system fattens the wallets of too many politicians. If a few do lose their gerrymandered seats, they often find jobs lobbying the very politicians who replaced them.

The task of politicians and partisans of both major parties is to first craft the problem. Is the problem 1) greedy capitalists, 2) the immoral redistribution of income, 3) an overabundance of regulation that is stifling business growth, 4) income inequality, 5) too much power concentrated in the Federal Government, 6) too much money in politics, 7) too much taxes, 8) too little taxes, 9) ineffective or inadequate Federal regulation? Pick one, or pick several. Make up your own. The problem is that people can not agree on the problems, much less the solutions.

The essence of capitalism is that it has one metric – the return on capital which directs the flow of capital.To the champions of capitalism, this simplicity of feedback is the virtue of capitalism. To the detractors of capitalism, this primitive mechanism is a bane. Socialist and communist planners insist that an elite can direct a society’s capital for the greatest good. They offer a top-down approach in contrast to the bottom-up solution design that a capitalist system offers. Because capitalism does not present a unified solution for a society’s problems, some people reach for socialist and communist solutions presented by the few only to find that those solutions benefit mostly the few.