January 3, 2016

As we begin 2016, let’s take a look at some trends. It is often repeated that the recovery has been rather muted. As former Presidential contender Herman Cain once said, “Blame Yourself!” You and I are the problem. We are not charging enough stuff or we are making too much money. Debt payments as a percent of after tax income are at an all time low.

At its 2007 peak, households spent 13% of their after tax income to service their debt. Currently, it is about 10%. In early 2012, this ratio crossed below the recession levels of the early 1990s. By the end of 2012, this debt service payment ratio had fallen even below the levels of the early 1980s. Almost six years after the official end of the Great Recession the American people are behaving as though we are still in a recession. An aging population is understandably more cautious with debt. In addition to that demographic shift, middle aged and younger consumers are cautious after the financial crisis. We gorged on debt in the 1990s and 2000s and paid the price with two prolonged downturns. Having learned our lessons, our overactive caution is now probably dragging down the economy.

In this election year, we can anticipate hearing that the sluggish economy can be blamed on: A) the Democratic President, or B) the Republican Congress. It is Big Government’s fault. It is the fault of greedy Big Companies. Someone is to blame. Pin the tail on the donkey. Blah, blah, blah till we are sick of it.

************************

Auto Sales

The latest figures on auto sales show that we are near record levels of more than 18 million cars and light trucks sold, surpassed only by the auto sales of February 2000, just before the dot com boom fizzled out. On a per capita basis, however, car sales are barely above average. The thirty year average is .054 of a vehicle sold per person. The current sales level is .056 of a car per person. Automobile dealers would have to sell an addiitonal 900,000 cars and light trucks per year to have a historically strong sales year.

************************

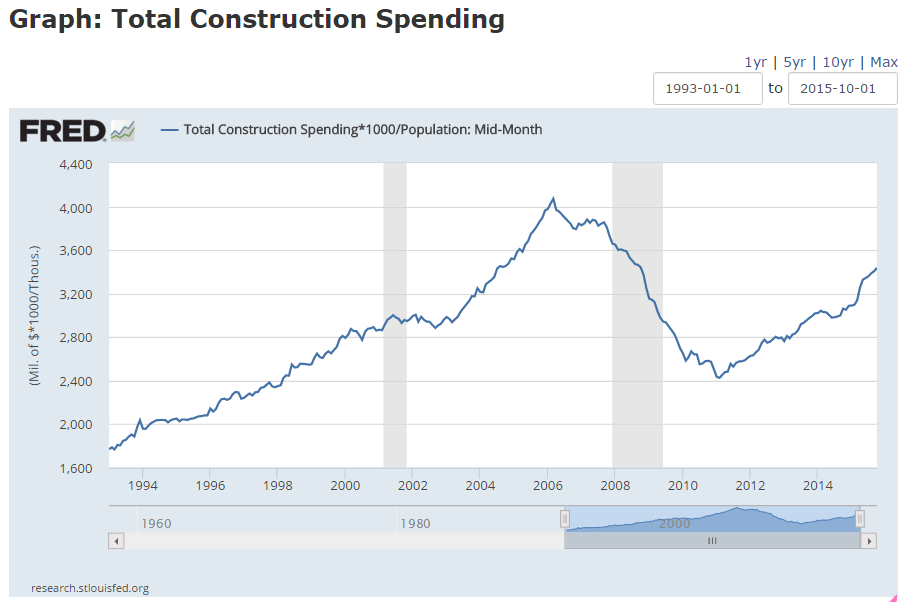

Construction Spending

In some cities, housing prices and rents are rising, and vacancies are low. We might assume that construction is booming throughout the country. Six years into the recovery per capital construction spending is at 2004 levels and that does not account for inflation. Levels like this are OK, not good, and certainly not booming.

*************************

Employment

The unemployment rate and average hourly wage may get most of the public’s attention but the Federal Reserve compiles an index of many indicators to judge the health of the labor market. Positive changes in this index indicate an improving employment picture. Negative changes may be temporary but can prompt the Fed to take what action it can to support the labor market. Recent readings are mildly positive but certainly not strong.

*************************

Stock Market

Many of the companies in the SP500 generate half of their revenue overseas. Because of the continuing strength of the dollar, the profits from those foreign sales are reduced when exchanged for dollars. According to Fact Set, earnings for the SP500 are projected to be about $127 per share, the same level as mid-2014. In the third quarter of 2015, the majority of companies reported revenue below estimates. As 4th quarter revenue and earnings are released in the coming weeks, investors will be especially vigilant for any downturns in sales as well as revisions to sales estimates for the coming year. It could get bloody.