October 6, 2019

by Steve Stofka

The employment report released Friday was a Goldilocks gain of 136,000 jobs for the month of September. Why Goldilocks? Not as weak as some feared following news this week that manufacturing was getting hit hard in the trade war with China (Note #1). Not so strong that it ruled out the possibility of another rate cut from the Fed this year. Just weak enough to speculate on another rate cut by year’s end. After several days of big losses, the market rallied on Friday.

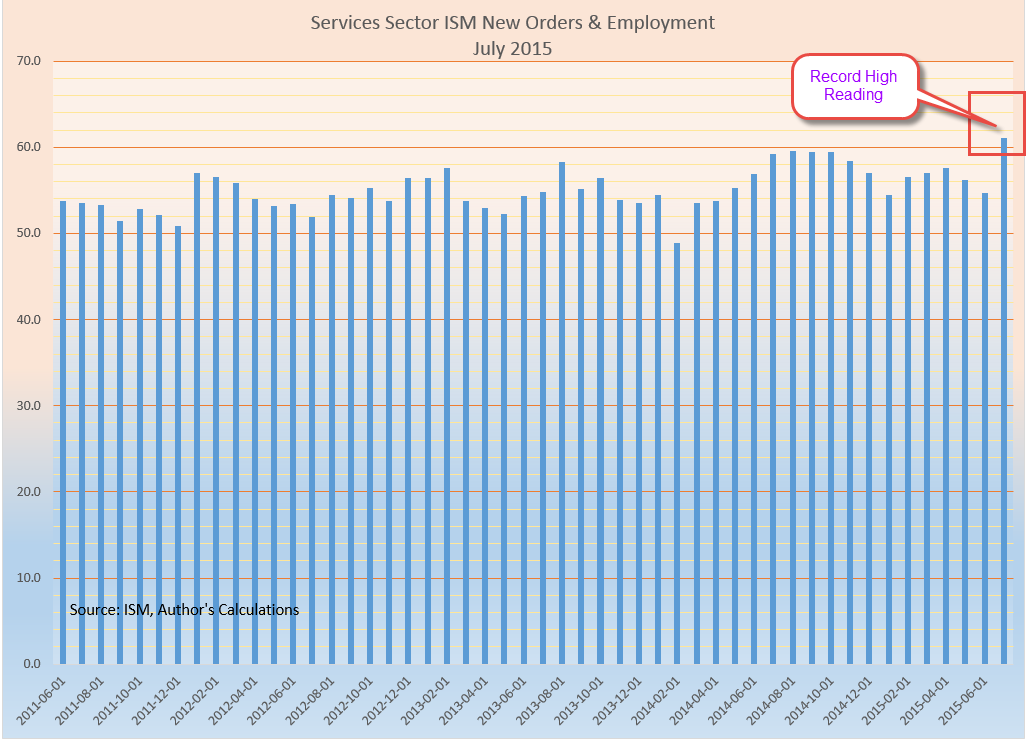

Although manufacturing has been contracting, a report on the rest of the economy was more encouraging, although a bit lackluster (Note #2). Service businesses are continuing to hire but the pace has slowed. New export orders have accelerated but new orders in total slowed significantly from August. Something to like, something not to like.

Billions of dollars around the world are traded as soon as the employment report is released each month. During Mr. Obama’s tenure private citizen Donald Trump accused Obama of fudging the employment numbers. Larry Kudlow, now Mr. Trump’s economic advisor, took him to task for that. Mr. Kudlow worked in the Reagan administration and knew well how sacrosanct the employment numbers were. The BLS is an independent agency working in the Department of Labor and its 2400 employees try to collect and publish the most accurate data it can accomplish. The agency’s Commissioner is the only political appointee in the BLS and once confirmed by the Senate, serves four years, the same as the head of the Federal Reserve (Note #3). According to Mr. Kudlow, the White House gets the number the night before only to prepare a press release when the report is released.

Mr. Trump’s reckless behavior helped him take out 16 other Republican presidential candidates in the 2016 election. He acts quickly and aggressively. That lack of caution has led to several bankruptcies, and because of that, no bank in the world will loan him money (Note #4). What if, on an impulse, Mr. Trump tweeted out the employment number shortly before its official release time? Some traders pay a lot of money so that the news will hit their trading desk a split second faster than a conventional news release. It’s that important. An early leak of the employment numbers would cost a lot of influential people big money around the world and would prompt a national if not a global crisis. Forget about the phone calls to foreign leaders to discredit Joe Biden. That would be an act of treason for sure – against the global financial community. Can’t happen? Won’t happen?

Mr. Trump knows no rules. His father protected him when his rash behavior got him into trouble as a child. The elder Trump sheltered Donald from his own mistakes in the real estate industry and his foolish foray into the Atlantic City gambling business. Now that Mr. Trump’s father is no longer there, he depends on others to protect him. He has enlisted a long line of people in that effort. They have come in the revolving door to the White House and left. The list is longer than I imagined (Note #5). John Bolton, the third National Security Advisor under Mr. Trump’s tenure, was the last high-profile team member to leave.

Mr. Trump has said that Americans would get tired of winning so much while he was President. To use a baseball analogy, when he takes the mound, the team doesn’t win very often. People who lose a lot either give up or blame everyone and everything else for their losses. They need to have an ideal environment or get lucky to win. Mr. Trump berates the independent Fed because he wants them to protect him. He needs every crutch he can get. He couldn’t succeed in a war or in the financial crisis because he is not disciplined or organized.

What does this mean for the average investor? Take a cautious approach and keep a balanced portfolio. Betting that Mr. Trump will pitch a good game is a poor bet.

Or is it? At an event on Friday, he claimed that the stock market has gone up 50% since he was elected. Not quite but it is up 42% since the day after he was elected (Note #6). It’s been about 35 months. That’s pretty good. A 60-40 stock-bond portfolio has gone up 30% in that time. Under Obama’s tenure the market only went up 27%. A balanced portfolio went up almost 40% and he had to deal with the worst recession since the Great Depression. The budget battles with Republicans put a big dampener on investor enthusiasm during Obama’s first term.

35 months after the Supreme Court awarded the presidency to George Bush, the market was down 25% but a balanced portfolio was up 21%. Even Mr. Clinton could not best Mr. Trump, although he comes close. 35 months after the 1992 election the market was up 38%. A balanced portfolio was up 40%. The winner? A balanced portfolio.

What might an investor expect? At today’s low interest rates and inflation, a break-even return might be 5% a year, for a total gain of 22% in four years. Will Mr. Trump’s first four years be one of his few wins? Check back in a year. It’s bound to be a tumultuous year.

/////////////////////////////

Notes:

- Institute for Supply Management (ISM). (2019, October 3). September 2019 Manufacturing ISM Report on Business. [Web page]. Retrieved from https://www.instituteforsupplymanagement.org/ISMReport/MfgROB.cfm

- Institute for Supply Management (ISM). (2019, October 3). September 2019 Non-Manufacturing ISM Report on Business. [Web page]. Retrieved from https://www.instituteforsupplymanagement.org/ISMReport/NonMfgROB.cfm?navItemNumber=28857&SSO=1

- Bureau of Labor Statistics. (n.d.). About the U.S. Bureau of Labor Statistics. [Web page]. Retrieved from https://www.bls.gov/bls/infohome.htm

- Business Insider. (2019, August 28). The world is talking about Trump’s relationship with Deutsche Bank. [Web page]. Retrieved from https://markets.businessinsider.com/news/stocks/trump-tax-returns-deutsche-bank-relationship-drawing-intense-scrutiny-2019-8-1028482268#why-it-matters2

- Wikipedia. (n.d.). List of Trump administration dismissals and resignations. [Web page]. Retrieved from https://en.wikipedia.org/wiki/List_of_Trump_administration_dismissals_and_resignations

- Prices are SPY, the leading ETF that tracks the SP500. Clinton: 42 to 58 (approximately) – up 38%. Bush: 138 to 103 – down 25%. Obama: 91 to 116 – up 27%. Trump: 208 to 295 – up 42%. Balanced portfolio returns from Portfolio Visualizer calculated using a mix of 60% U.S. stock market, and 40% of an evenly balanced mix of intermediate term government and corporate bonds. Dividends were reinvested and the portfolio re-balanced annually.