March 8, 2015

Labor Market

If you are reading this and have not set your clock forward, that’s OK. March to your own drummer!

On Wednesday, payroll processor ADP released their data for February, showing private payroll gains of 212,000. This confirmed estimates that total job gains from the BLS would be about 230,000. The bothersome data point in the ADP report was the huge upward revision of job gains in January, bringing it close to the BLS estimate. ADP is working with a lot of hard data – actual paychecks – so was this revision a discrepancy in seasonal adjustments?

On Thursday, the BLS issued revised figures for labor productivity in the 4th quarter of 2014. The report includes this: “The 4.9 percent increase in hours worked remains the largest increase in this series since a gain of 5.7 percent in the fourth quarter of 1998.” 4th quarter productivity sagged 2.2% from the 3rd quarter, and was essentially unchanged from the 4th quarter of 2013. Labor productivity is often a lagging indicator but it narrowed Thursday’s trading range as investors crossed bets on the Fed’s plans for raising interest rates later in the year.

The BLS report of 295,000 job gains in Febuary was so over the top that many traders punched the sell button. Government employment increased 7,000, meaning that private job gains as reported by the BLS was almost 290,000, a difference of almost 70,000 between the BLS and ADP reports. When in doubt, traders get out.

For mid to long-term investors, the continuing strength in the labor market is an optimistic sign. Employees add to costs and commitments. If businesses are adding jobs, it is because they anticipate higher revenues in the near future. Some analysts pointed to the high number of jobs gained in the leisure and hospitality sectors as a sign of weakness in the labor market. These are jobs that pay on average about 25% less than the average of all production and non-supervisory employees and a third less than the average for all employees. However, higher paying jobs in professional services and construction also showed strong gains.

As I have mentioned before, the Federal Reserve compiles a Labor Market Conditions Index (LMCI) which summarizes 24 employment trends and one which chair Janet Yellen uses as her gauge for the fundamental strength or weakness of the labor market. Next Wednesday, the Fed will release the LMCI updated for February but a chart of the past twenty years shows longer term trends.

While the index itself is still in negative territory, the momentum (red line) of the index is strong and consistent. We can understand Yellen’s cautious optimism when recently testifying before the Senate Banking Committee. This index was only developed a few years ago so this chart includes revised data and methodology that is backward looking. If history is any guide, a long term investor would be ill advised to bet against the momentum of this index when it is positive.

A key indicator for Ms. Yellen is the Quit rate, the number of employees who quit their jobs to go to another job or who feel confident that they can find another job without much difficulty. That confidence measure continues to rise and is currently in a sweet spot. It is not overly confident as it was at the height of the housing boom in 2006 and the dot com boom of the late 1990s. It is neither pessimistic as it was in the early 2000s or darkly apocalyptic as in the period from 2008 – 2012.

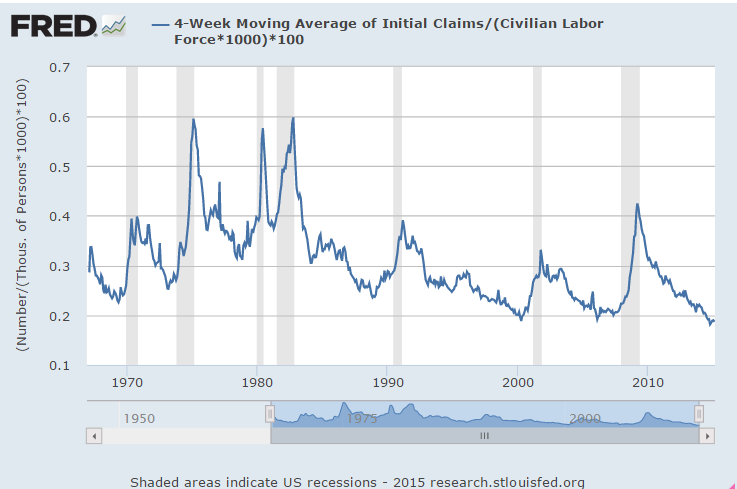

The number of new claims for unemployment as a percentage of the Civilian Labor Force is at historic lows. One could argue that new claims are too low.

Wage growth in this month’s report was minimal. However, wage growth since 2006 has not done too badly, growing more than 25% and outpacing the 16% growth in inflation during the period.

Benefits have grown more than 20% in the same period and showed no decline during this past recession. Many employees are simply not aware of the costs of their benefits. They may think that vacations and holidays and health care are the only benefits they get. There are several mandated taxes and insurance that an employer is required to pay.

Because some benefit costs are “sticky,” and not responsive to changing business conditions, the continued strength in the labor market shows an increasing commitment on the part of employers, a growing confidence that economic conditions are fundamentally improving. Several years ago, many employers were reluctant to take on new employees because positive news was regarded with a healthy skepticism. “We won’t get fooled again,” as the Who song lyric goes. Despite improving fundamentals, the market is likely to be somewhat volatile this year as investors and traders speculate on the timing and aggressiveness of any interest rate moves from the Fed.

**************************

Purchasing Managers Index

Based on the monthly survey of purchasing managers, the Constant Weighted Purchasing Index (CWPI) declined slightly again this month as expected. The manufacturing sector slid a bit this past month but employment in the service sectors popped up, keeping the composite index up above the benchmark of strong growth. If the post-recession trend continues, we might see one more month of softening within this growth period.

New orders and employment in the service sectors are the key indicators that I highlight to get a more focused analysis of growth trends. When this blend of the two factors stays above 55, the benchmark of strong growth, the economy is strong. Except for a slight dip below that mark (54.4) last month, this blend has been above 55 for ten months now.

We can also see the brief periods of steady decline in these two components in 2011, 2012 and the beginning of 2013, causing the Federal Reserve to worry about a further decline into recession. The Federal Reserve enacted a series of bond buying programs called QE. Continued economic strength may prompt a slow series of interest rate hikes. The key word is “slow.” Under former chairman Alan Greenspan, the Federal Reserve adjusted interest rates up and down too quickly, which produced small shock waves in the financial system. Banks, businesses and investors may make unwise choices in response to rapid rate changes. Live and learn is the lesson.