December 22nd, 2013

Merry Christmas!

Last week I reviewed several decades of trends in corporate profits, as well as the 1990 change in measuring inflation that has helped increase corporate profits as a share of GDP. (For those of you interested in the inflation controversy, here is an article that provides some additional insight.) This week I’ll look at patterns in the economic growth of this country that sheds some light on recent events and provides some context to understand ongoing trends.

During the 30 years following World War 2, the economy grew at an annual rate of 3.7% after inflation. Population growth was about 1% per year. Productivity growth was about 1 – 1.5%. Government spending, including debt, grew a bit more than 1%. The chart below shows the compounded annual growth rate.

But I think the story is more clearly told by a different chart constructed from the same data. The growth rate trend is more easily visible and it is the change in this trend that I will be focusing on.

During the 1970s, an economic trend known as staflation increasingly took hold. This period of high inflation, coupled with slowing growth and growing unemployment, was not thought possible by economists using theories proposed by John Maynard Keynes in the 1930s, during the Great Depression. In 1974, economist Arthur Laffer first sketched out a theory that tax cuts would stimulate the economy. As the Federal debt began to rise in the mid to late 1970s, few wanted to take a chance that lower tax rates would produce more revenue for the Federal Government.

The 1980s began with back to back recessions and the highest unemployment since the 1930s Depression. Big spending and tax cuts during the 1980s dramatically increased the federal debt but did little to spur growth.

During this 13 year period, profit growth slowed to 2.4%. The myth that the 1980s was a high growth era continues to live in the minds of political pundits. In a WSJ op-ed on Dec. 18th, Daniel Henninger referred to “the high-growth years of the Reagan presidency.” Myths live on because they serve a purpose to those who cherish them. The cardinal rule of politics is “Disregard the Data.”

In 1990, economists at the BLS adopted what is called a hedonic methodology to computing the CPI. Used by other OECD countries, this supposedly more accurate assessment of the growth of inflation shows a lower growth rate of inflation. This naturally increases the growth rate of inflation adjusted GDP. (GDP dollars each year are divided by the inflation rate to get the real growth rate.)

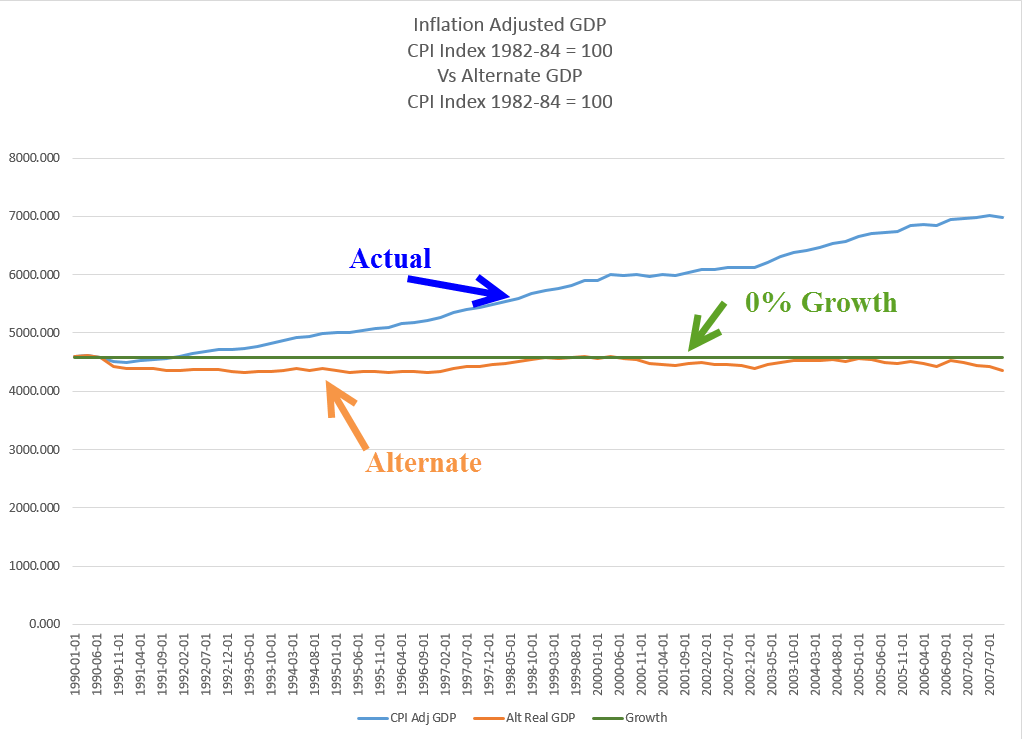

The conventional narrative is that the 1990s was an explosive growth period of new technology and growing globalization. From the beginning of 1990 to the start of 2000, stock market values grew four times. After the bursting of the internet bubble, 9-11, and the recession of 2001, the economy recovered. By the mid-2000s, the unemployment rate was less than 5%. While that may be the conventional narrative, the growth of the economy from 1990 to 2007 was just as slow as the period 1978 – 1989.

Remember that this slow growth would have been even slower if the BLS had not changed their methodology for measuring inflation. To recap, the 30 year real growth rate of GDP after WW2 was 3.7%. The following 30 year growth rate was 2.3%. But that later 30 period is marked by a sharp rise in consumer borrowing. Without that escalation in borrowing, growth would have been meager.

Families with two incomes borrowed against their homes, drove up the balances on their credit cards and still GDP growth was slow. Let’s construct a fairy tale, what economists call a counterfactual. What if the BLS had not changed to this new methodology in 1990? What would be the growth rate of GDP using an alternate measure of inflation?

The resulting growth pattern is 0% for the 18 year period and is more consistent with the experiences of many workers and families in this economy. The change in the measurement of inflation has greatly helped mid-size and large size companies. An understated inflation rate reduces labor costs by reducing cost of living adjustments to salaries and wages. In addition, companies can borrow at lower rates since many corporate bonds are tied to the inflation rate. American companies did not engineer this revised methodology of measuring inflation but they have been the largest beneficiaries of the new policy.

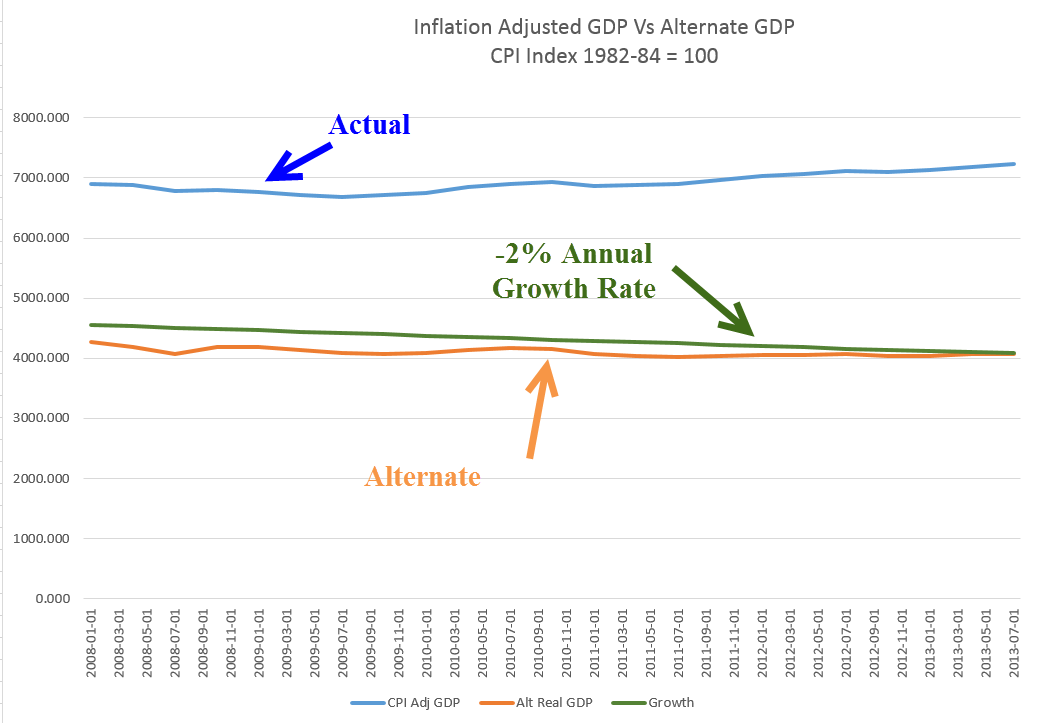

In 2008, the financial poop in the popcorn popper began to pop. In the past 5+ years, we have experienced less than 1% real growth, not enough to keep up with population growth. Of course, most people are wondering “what growth? It sure doesn’t feel like growth!”

The story may be told more accurately by looking once again at a comparison of inflation adjusted GDP with an alternate version of GDP, one that more realistically reflects inflationary pressures. This chart shows a decrease of 2% per year.

Did the BLS adopt this methodology under political pressure? Perhaps. More likely, it was an alignment of econometric theory with political and corporate interests. The reduction in published inflation rates did slow the growth of payments to Social Security recipients and reduced Medicare payouts to physicians and hospitals, thus shrinking budget deficits. The government saves money, corporations make extra money, but – quietly and slowly – families lose money.

Annual cost of living adjustments to Social Security checks have been reduced but the decreased income has forced more seniors to seek assistance through the food stamp program, now called SNAP. A politically neutral change in the measurement of inflation thus becomes a way for politicians to introduce a means testing component to Social Security income. Instead of reducing payments based on income, payments are reduced to all recipients and poor seniors are targeted for additional benefits. Congress has increased eligibility for the food stamp program so that seniors who are dependent on that extra income can receive it in the form of food stamps. If the BLS had not changed their methodology, seniors would receive appoximately 60% more each month and many wouldn’t need the food stamps in the first place.

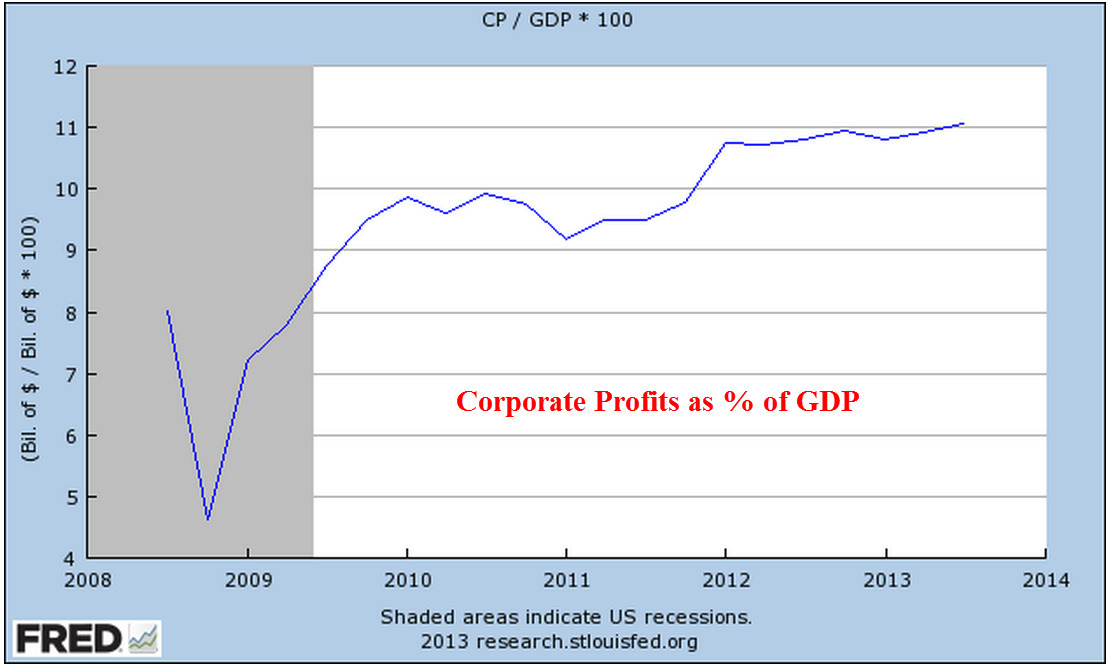

With this history in mind, let’s turn to this week’s revisions of GDP and corporate profits for the third quarter ending in September. The real, or inflation-adjusted, growth of 3rd quarter GDP was raised to a 4.1% annualized growth rate in the third quarter, largely on upward revisions of consumer spending. Contributing to stronger GDP growth has been a worrisome increase in company inventories, which probably influenced the Federal Reserve’s decision this week to keep any tapering of their QE bond purchases to a minimum.

Corporate profits for the third quarter were revised higher as well. As a share of GDP, corporate profits continue to reach all time highs.

How likely is it that economists at the BLS will change their methodology to reflect inflationary pressures before we make choices in response to rising prices? The subject is not easily encapsulated in a sound bite or a short slogan on a placard. In the 1992 presidential race, independent candidate Ross Pierot was able to use charts to make a point with many voters but few politicians are very good at the easel and unlikely to bring up the subject in the public forum. Families and workers will continue to suffer and politicians will create more social benefit programs to help those hurt by problems that politicians themselves have either created or failed to address. Large and mid sized businesses will continue to enjoy the additional slice of pie.