April 2nd, 2017

The Conference Board’s survey of Consumer Confidence shot up to 125, a 16 year high. Unfortunately, that previous high was set as the dot-com frenzy was nearing its end and just before the start of the 2001 recession. History could not possibly repeat itself, could it?

There have been other frenzies in the past decades: the dot-com boom of the late ’90s, the housing and consumer debt boom of the ’00s, the run up in gold prices in the ’10s, the spike in interest rates in the late ’70s – eary ’80s. In the rear view mirror, the correction seems predictable.

From 1995 – 2000, the SP500 index tripled on the giddy expectations of a new global internet economy. Here was the plan: global supply chains spread among developing countries would assemble products which would be shipped to markets around the world. The U.S. and other developed countries could steer the global economy to new heights, and rid themselves of the nasty pollution that comes from manufacturing stuff.

Then, the new global digital economy went oops…

After falling back about 40%, the index then doubled from early 2003 through 2007. During that five year period, the house price index grew 40%, more than double its annual growth rate for the past century. In the old mortgage model, a lender would take a risk on the fortunes and reliability of a single family to repay a mortgage. Now, through the power of computerized algorithms, that risk could be sliced and diced so thin and spread among so many synthetic mortgages that the risk virtually disappeared. The smart people in the financial industry had finally figured out the secret to securitized debt. Every family could now build wealth by owning a home. Oh, happy days!

Then, housing went oops….

As the financial crisis gripped most of the developed world, central banks took on vast quantities of debt and expanded the money supply to counteract a slide into a global depression. Expanding the money supply usually brings an increase in inflation, and to protect against that coming inflation, investors around the world turned to gold. From the depths of the financial crisis in early 2009 toward the latter part of 2011, a period of less than 3 years, the price of gold doubled. But inflation did not rise as expected. The central banks had simply been fighting a strong undercurrent of deflation, stronger than even they had realized.

As inflation remained low, gold went oops….

The trick is to figure out beforehand what will go oops next. The pattern is this: an increasing number of people become convinced of “X” idea and begin to take it for granted. Then some series of events undermines a belief in “X” and the stampede begins. The massive increase in sovereign debt looks like a prime candidate for default and debacle but the central banks of developed countries have many legal and financial tools at their disposal to stem any panics.

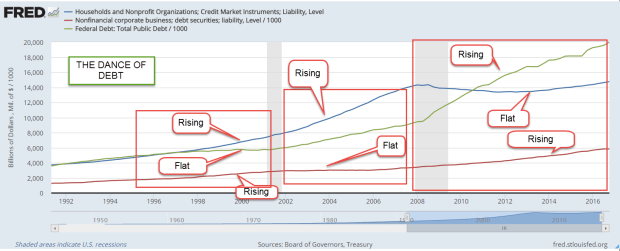

For a dominant economic power like the U.S., the “X” has traditionally been based on private debt whose value can not be easily controlled by government dictate. In the late 90s, it was technology. Most of us associate that period with wildly inflated stock prices and IPOs that jumped in price on opening day. What may have escaped our attention is that corporate debt increased by almost 60% from the beginning of 1995 to the end of 2000. When the towers came down on 9-11, corporate debt had grown 75%. From early 2002 through 2005, there was no growth in corporate debt.

As corporate debt grew in the late 90s, government debt decreased. As corporate debt growth stopped in the early ’00s, household debt and government debt surged upwards. So let’s keep our eyes on this dance of corporate, household and government debt.

Since the financial and housing crisis that began in 2008, federal govt debt has doubled, while household debt declined. It has taken eight years for household debt to finally surpass its 2008 high water mark, and is now approaching $15 trillion.

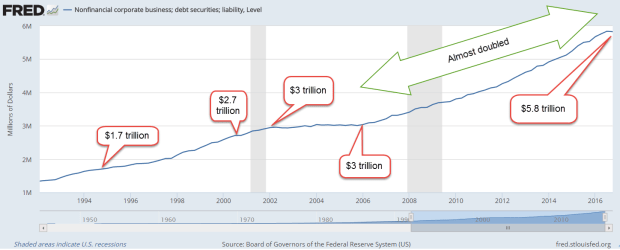

Since 2006, corporate debt has almost doubled. It is my guess that this is where the next crisis lies.

After the next crisis, we will look back and see that there was such an obvious over-confidence in that “X.” Analysts will help us understand the details and unfolding of the crisis till we think that we can avoid it next time. Like whack-a-mole, the next crisis will pop up from another hidey hole. The trick is to have several smaller hammers instead of one big hammer.