January 1, 2017

Happy New Year! How many days will it take before we remember to write the year correctly as 2017, not 2016? It is going to be an interesting year, I bet. But let’s do a year end review.

Homeownership

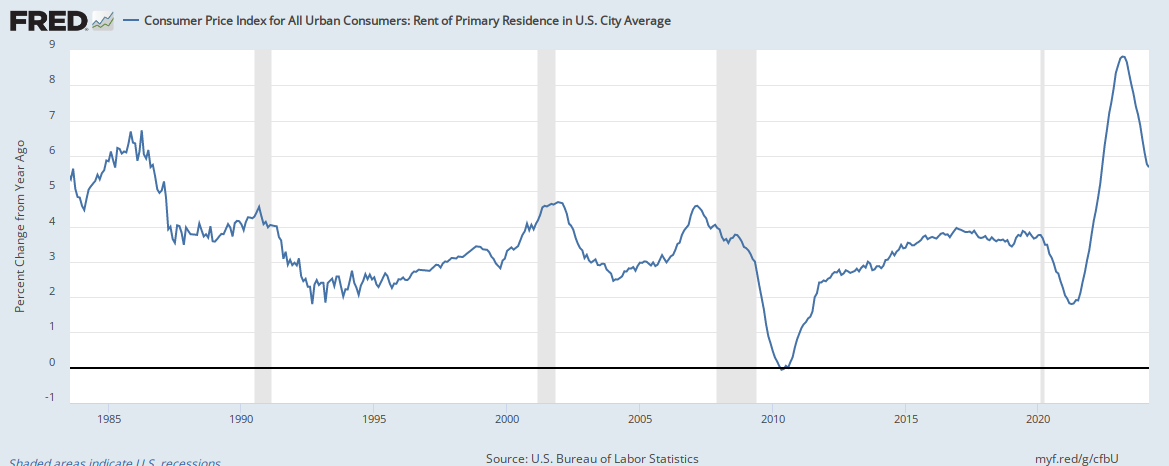

The home ownership rate has fallen near the lows set in 1985 and the mid-1960s at about less than 64%. (Graph) In 2004, the rate hit a high of 69%. For the U.S., the sweet spot is probably around 2/3 or 66%. Most other countries have higher rates of home ownership, including Cuba with a rate of 90%. (Wikipedia article) Rents in some cities have been growing rapidly. In the country as a whole, rents have increased almost 4%, about twice the growth in the CPI, the general rate of inflation for all goods and services. (Graph)

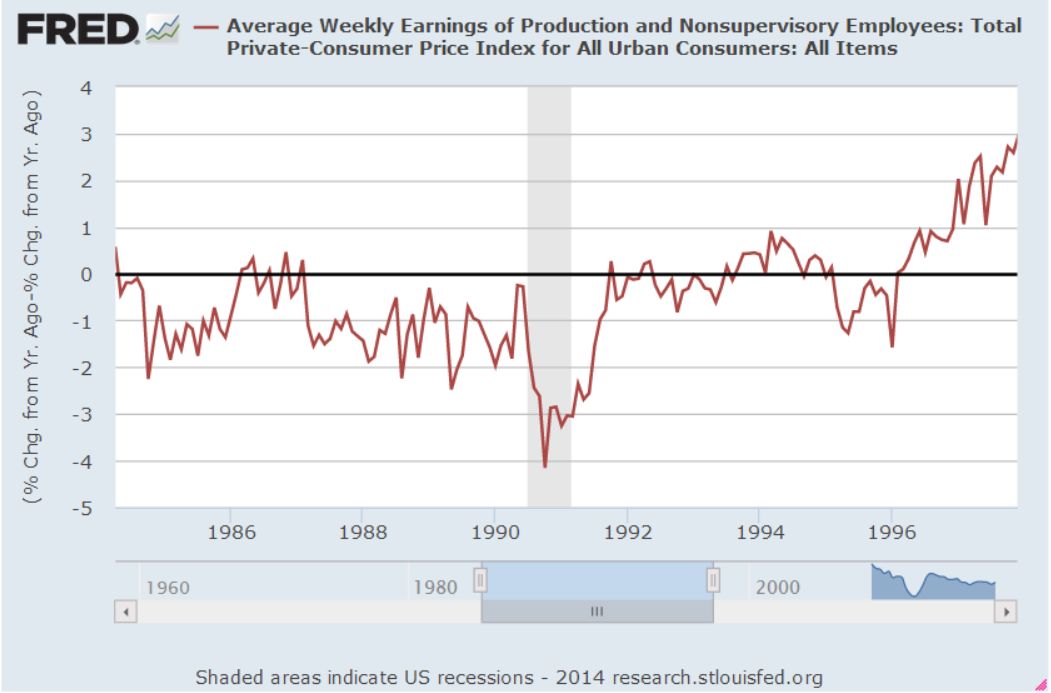

Earnings

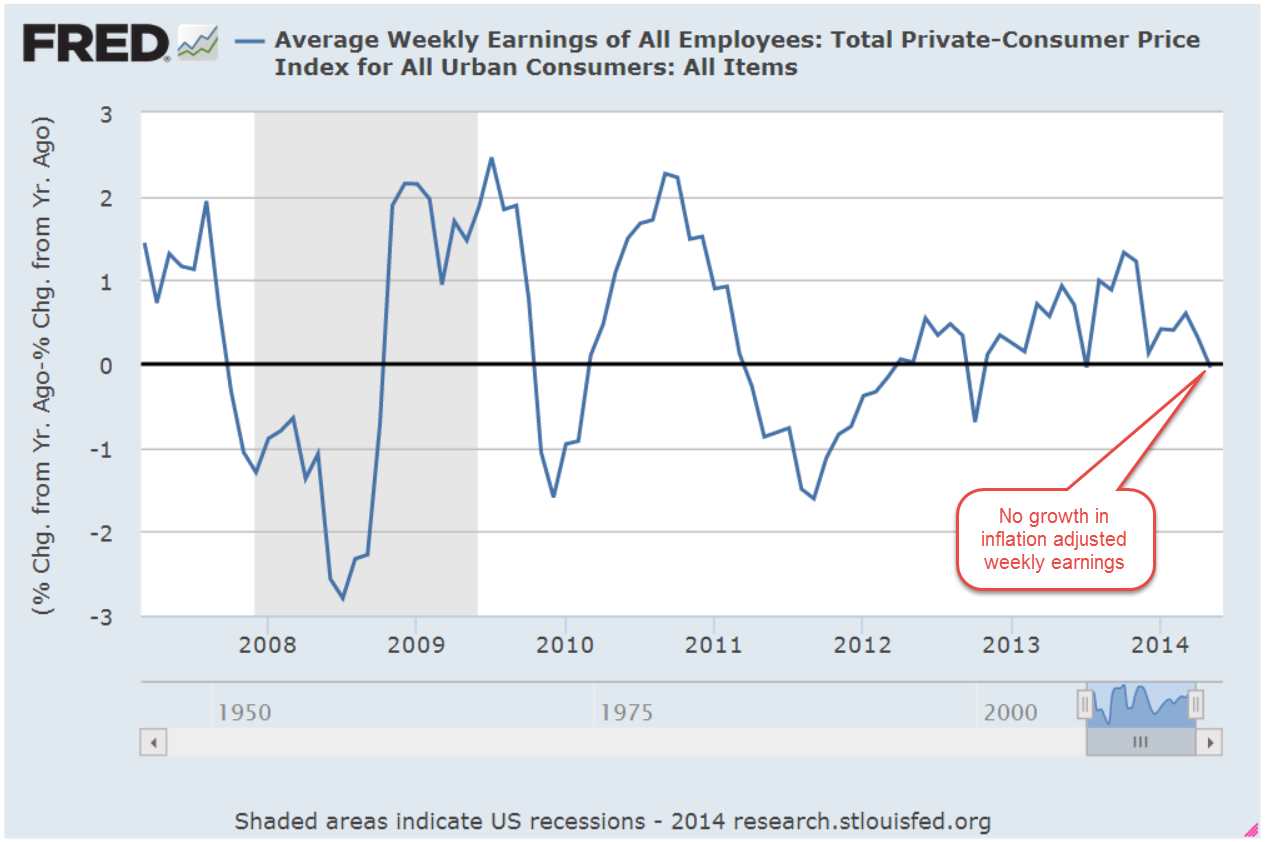

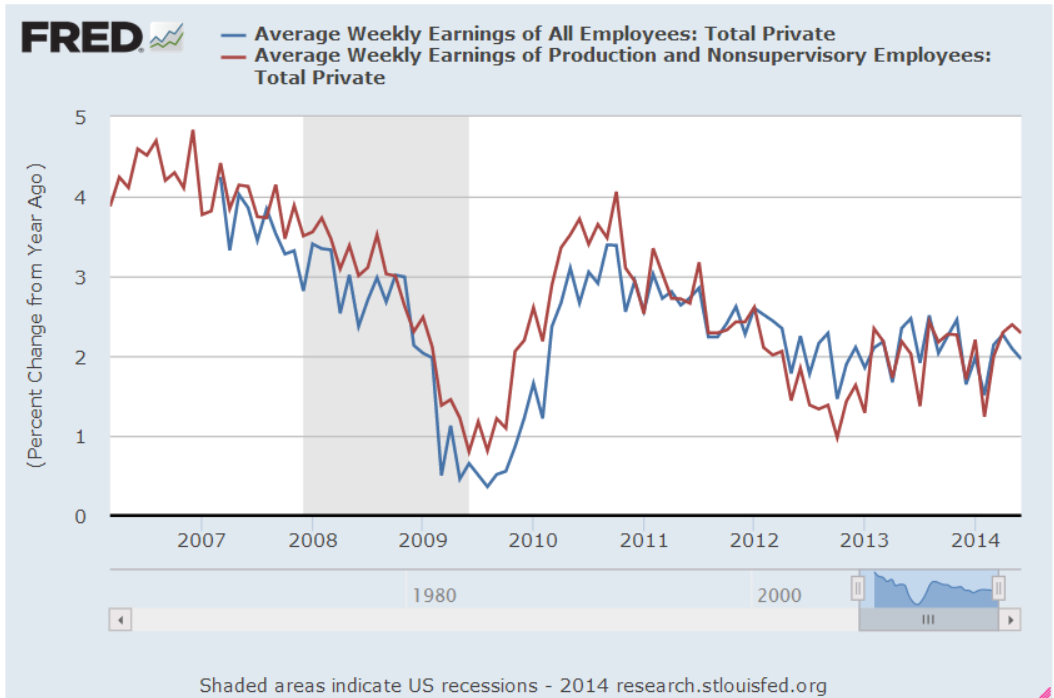

Real, or inflation-adjusted, weekly earnings of full time workers spiked up during the recession as employers laid off lower paid and less productive workers. By late 2013, weekly earnings had fallen to 2006 levels and have risen since, finally surpassing that 2009 peak this year.

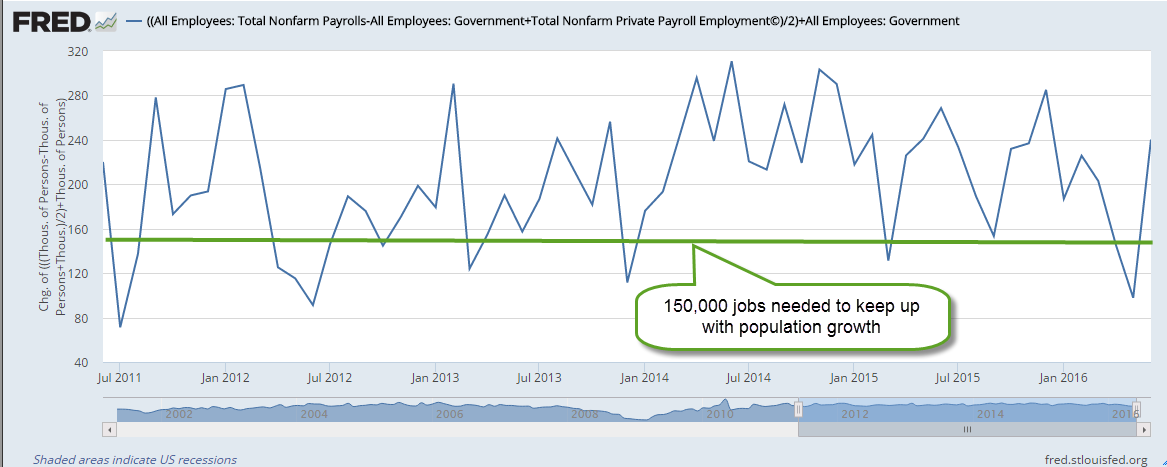

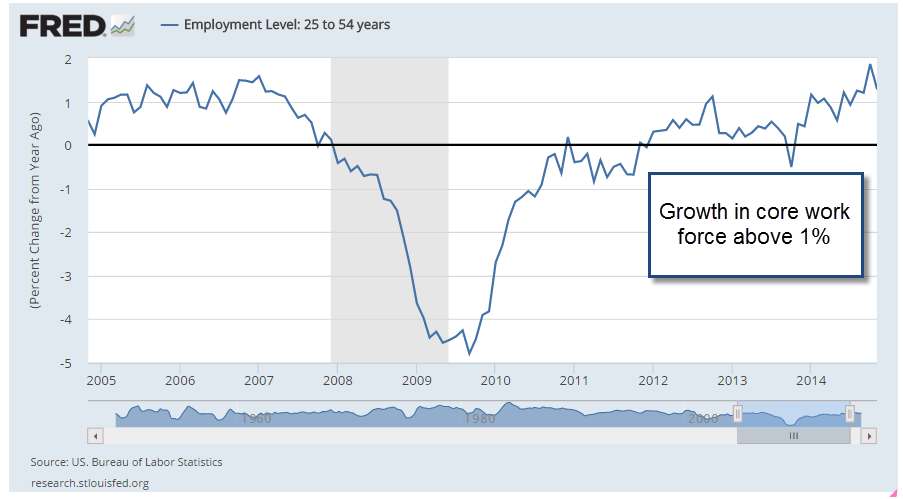

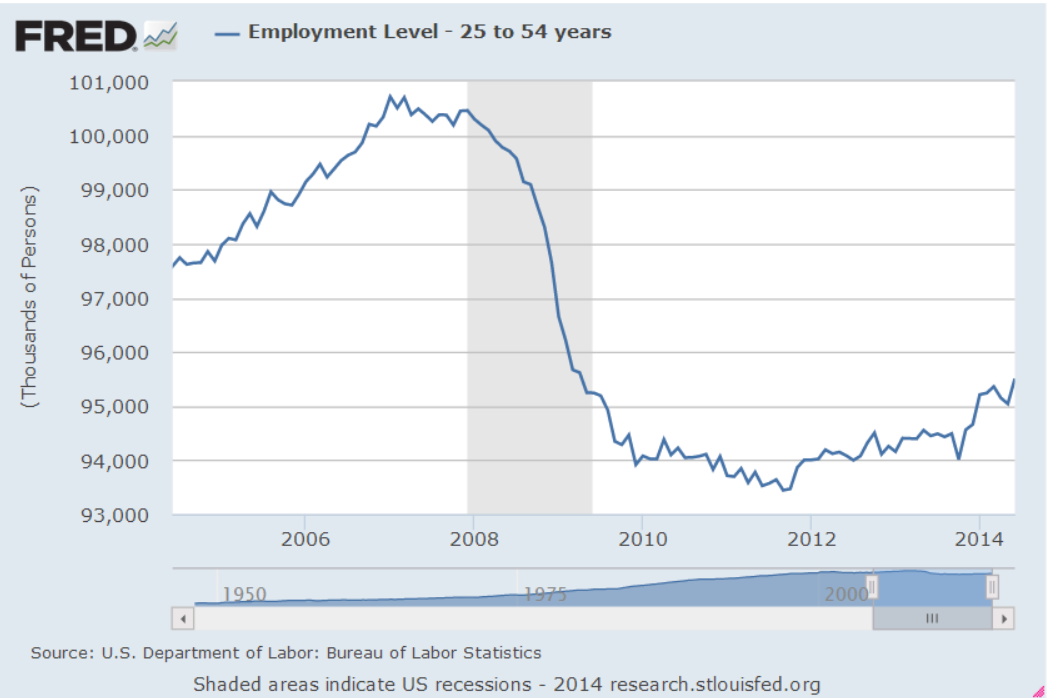

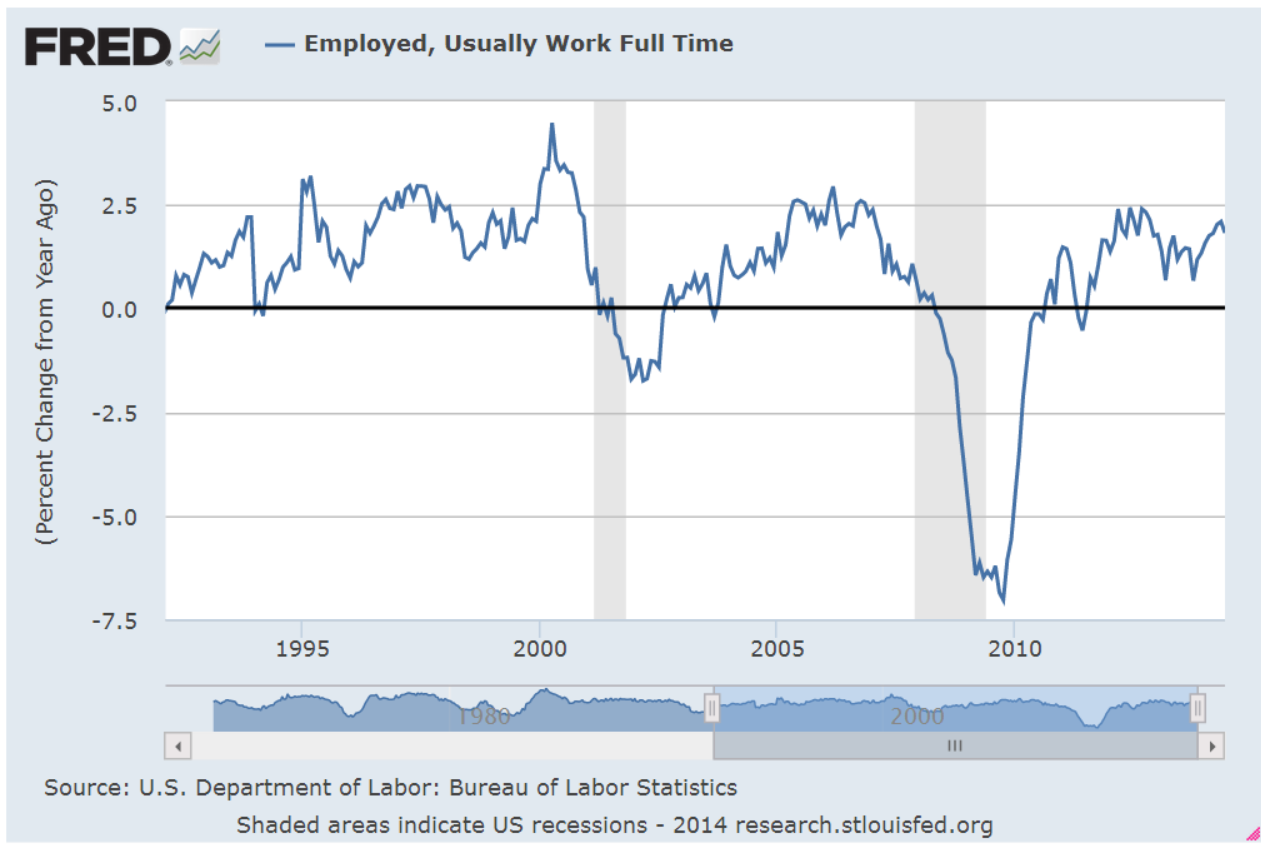

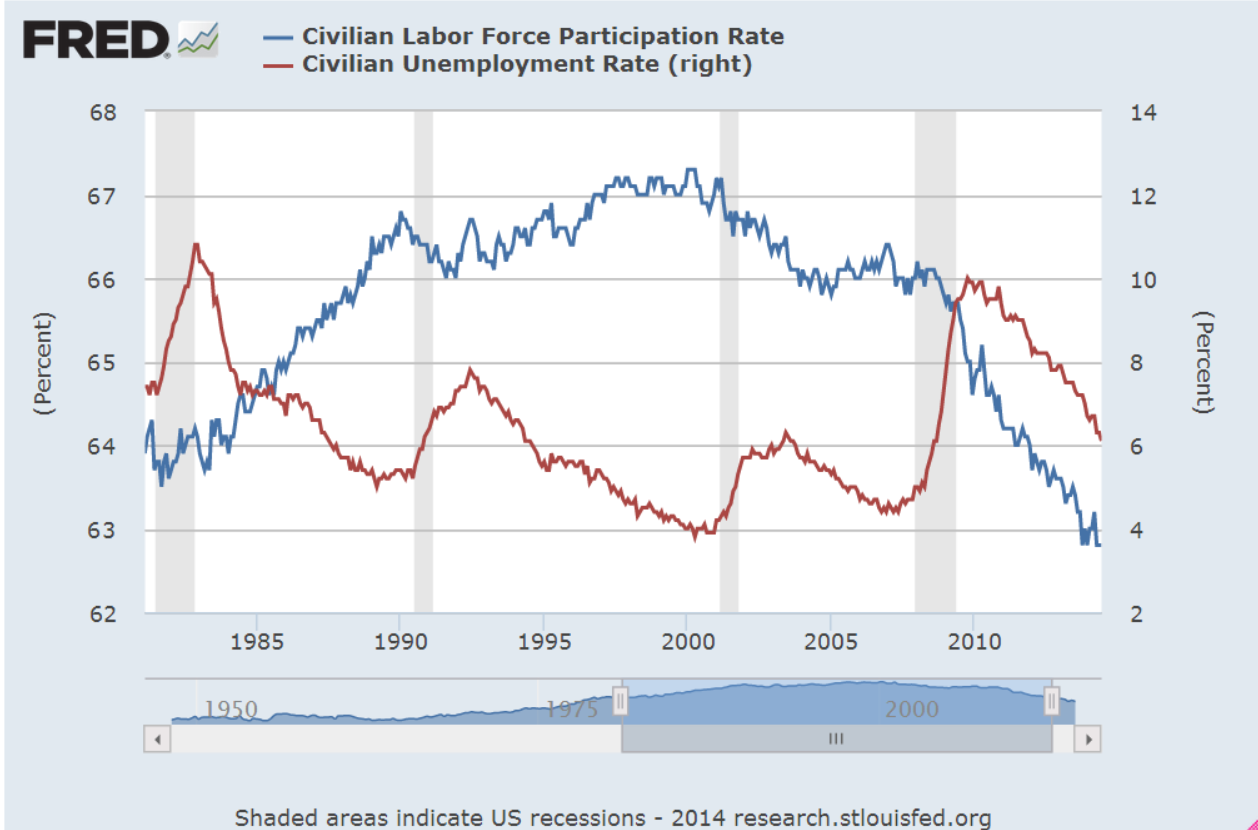

Core Work Force

Almost every month I look at the changes in the core work force of those aged 25-54 who are in their prime working years, who buy homes for the first time and have families. These are the formative years when people build their careers, and form product preferences, making them a prime target for advertisers. The economy depends on this age group. They fund the benefit systems of Social Security and Medicare by paying taxes without collecting a benefit. In short, an economy dependent on intergenerational transfers of money needs this core work force to be employed.

For two decades, from 1988 to 2008, the labor participation rate of this age group remained steady at 82% – 83%. (BLS graph) By the summer of 2015, it had fallen to 80%. A few percent might not seem like much but each percent is about a million workers. For the past year it has climbed up from that trough, regaining about half of what was lost since the Great Recession.

Consumer Confidence

A post-election bounce in consumer confidence has put it near the levels of 2001, near the end of the dot-com boom and just before 9-11. (Conference Board) In 2012, the confidence index was almost half what it is today.

Business Sentiment

Small business sentiment has improved significantly since the November election (NFIB Survey). Almost a quarter of businesses surveyed expect to add more employees, a jump of 2-1/2 times the 9% of businesses who responded positively in the October survey. In October, 4% of companies expected sales growth in the coming year. After the election, 20% responded positively. This jump in sentiment indicates the degree of hope – and expectation – that business owners have built on the election of Donald Trump.

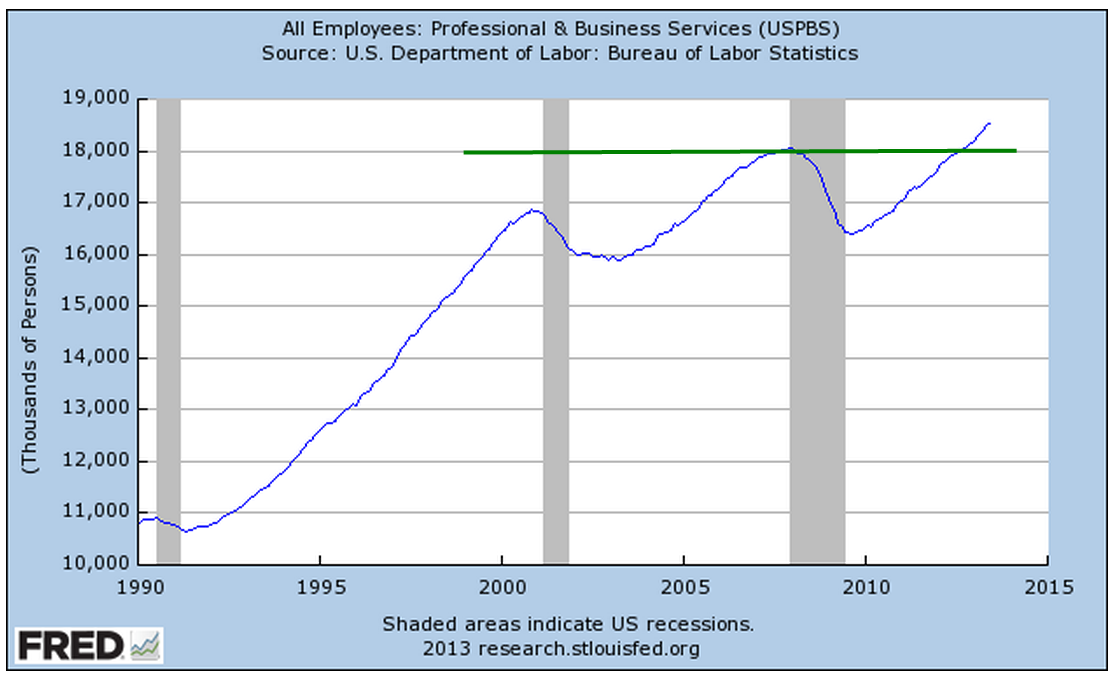

Hope leads to investment and business investment growth has turned negative (Graph). Recession often, but not always, accompanies negative growth. Since 1960, investment growth has turned negative eleven times. Eight downturns preceded or accompanied recessions. Let’s hope this renewed hope and some policy changes reverses sentiment.

On the other hand, those expectations may present a challenge to the incoming administration, which has promised some tax reform and regulatory relief. Small business owners will lobby for different reforms than the executives of large businesses. Regulations of all types hamper small business but large businesses may welcome some regulation which acts as a barrier to entry into a particular market by smaller firms.

Publicly held firms will continue to lobby for repeal or reform of Sarbane Oxley reporting provisions. For six years, the Obama administration has wanted to roll back these regulations but has been unable to come up with a compromise between the SEC, which regulates publicly traded companies, and Congress. A Trump administration may finally reform a law that was rushed into place by George Bush and a Republican Congress in response to the Enron scandal. That scandal grew in part from the Bush administration’s push to deregulate the energy market.

Voters Veer From Side To Side

We have stumbled from an all Republican government in 2002 to an all Democratic government in 2008 and now come full circle again to an all Republican government. Once in power, neither party can resist using economic policy to pick winners and losers. Every few years the voters throw out the guys in charge and bring the other guys in, hoping that the party that has been out of power will be chastened somewhat. Within a few months of taking power, each party digs up their old bones and begins to gnaw on them again. Tax reform, prison reform, justice and fairness for all, climate change, more regulation, less regulation – these bones are well chewed.

Still we keep trying. The priests and prophets of long ago kingdoms could not govern. Neither could the kings and queens of empires. So we have tried government of the people, by the people and for the people and it has been the bloodiest two centuries in human history. Still we keep hoping.

The Presidential Test

Most presidents are tested in their first year in office. Kennedy had to grapple with the Soviet threat and Cuba almost as soon as he took office. Johnson struggled with urban violence, social upheaval and the war in Vietnam.

Nixon confronted a newly resurgent Viet Cong army when he first took office. His second term began with the Arab oil embargo. Ford dealt with the aftermath of Watergate and Nixon’s resignation under the threat of impeachment.

Jimmy Carter began his term with the challenges of high inflation and unemployment, and an energy crisis to boot. Ronald Reagan wrestled with sky-high interest rates and a back to back recession in his early years. His successor, H.W. Bush, met a Soviet Union near the end of its 70 year history as Gorbachev loosened the reins of Soviet control of eastern European countries and the Berlin Wall collapsed.

After an unsuccessful attempt to reform health care in his first year of office, Clinton suffered in the off year election of 1994. G. W. Bush had perhaps the worst first year of any modern President – the tragedy of 9-11. Obama entered office under a full blown global financial crisis.

Despite Putin’s bargaining rhetoric regarding President-elect Donald Trump, every President has to learn the lesson anew – Russia is not our friend. Trump will have to learn the same lesson. China’s territorial claims in the South China sea may prompt an international incident. N. Korea could launch a missle at S. Korea and start a small war. Iran, Afghanistan, Iraq and Syria, Israel’s settlements, Palestinian independence – the crises may come from any of these tinderboxes. We wish the new President well as he hops into the fire.

{kind=link}

{kind=link}

{kind=link}

{kind=link}