September 6, 2015

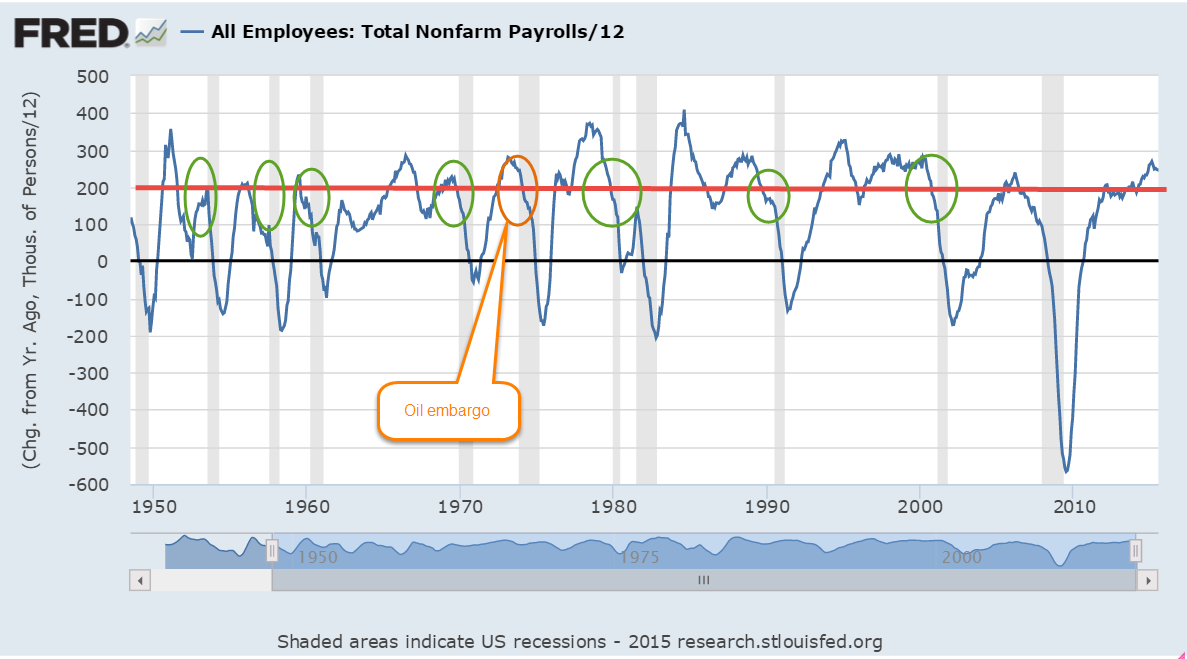

I am not going to say a lot about the August employment numbers, reported at 173,000, since August’s numbers are routinely revised. The BLS survey was 20,000 less than the ADP survey of private payrolls. The revised figure will probably be closer to 210,000 jobs gained in August. We can see the more important trends when we look at the annual job gains averaged over 12 months.

The slowdown in China and other markets and the selloff in markets around the world inevitably prompts talk of recession. Since WW2 there has been only one recession – the one that followed the 1973 oil embargo – that occurred when monthly job gains were above 200,000. There have been 12 recessions since WW2. The work force was very much smaller fifty years ago. There has been only one exception to this “rule” and when we look at this exception in closer detail we see that it was very much like the prelude to other recessions. Averaged monthly job gains were declining sharply as they do before every recession. Job gains are NOT declining sharply today.

******************************

Resource Countries On Sale

Monday came the news that the Canadian economy was officially in recession. California, the most populous of fifty U.S. states, has two million more people than all of Canada, whose economic vitality relies on its vast stores of timber, oil, gas and minerals. Australia, Russia, Norway and New Zealand also ride the roller coaster of commodity prices. (WSJ article ) An ETF that captures a composite of Canadian stocks, EWC, is down almost 30% from its high of August 2014. The 50 week (not day, but week) average is about to cross below the 200 week average.

These long term downward crossings are often bullish, indicating that prices are near a low point in the multi-year cycle. An ETF composite of Australian stocks, EWA, is down a bit more than 30% and its 50 week average just crossed below the 200 week average.

A Vanguard ETF composite of energy stocks is near the lows of 2011.

********************

Subprime Mortgages

Conventional wisdom: subprime mortgages started the recent financial crisis in 2008. A recent National Bureau of Economic Research (NBER) analysis (A short summary ) of home foreclosures overturns that misconception. The authors found that twice as many prime borrowers lost their homes to foreclosure as subprime borrowers.

********************

Inflation

In 2007, the Social Security Administration estimated that prices would be 20% higher in 2015. Then came the severe recession of 2008-09 and persistently low inflation. Prices this year are only 15% higher than those in 2007. Social Security payments will total almost $900 billion this fiscal year (FRED series), more than 20% of Federal spending, and are indexed to inflation. Low inflation “saves” the Federal government about $40 billion each year when compared with earlier projections. Sounds good? Life is a trade-off. The 60 million (SSA) people who receive social security spend most of it. That savings of $40 billion is money not spent. In addition, low interest rates have reduced income for many retirees, who depend on safer investments for an income stream. These safer accounts, which include savings, CDs, short and mid-term bond funds, have paid historically low interest rates since the Federal Reserve lowered its target interest rate to near-zero (ZIRP) in 2008.