November 15, 2015

Gone Fishin’ Portfolio

I found this portfolio in a pile of old paperwork. The idea is to allocate investment dollars in a number of buckets, then more or less forget about it, rebalancing once a year. The portfolio is 60% stocks, 30% bonds, 10% other

I compared this broadly balanced portfolio #1 with a simpler version #2: 60% stocks, 40% bonds. Because the Vanguard mutual fund VTSMX is weighted toward U.S. large cap stocks, I split the stock portion of the portfolio with an index of small cap value stocks VISVX. The 40% bond component is an index of intermediate-term corporate grade bonds VFICX. I also included a very simple portfolio #3 without the split in the stock portfolio. The 60% stocks is represented by one fund VTSMX. The results from Portfolio Visualizer include dividends.

Note that there is little difference between Portfolios #2 and #3 over this time period. Although the Gone Fishin’ portfolio lagged the other two during this time period, it did do better during the period 2000 – 2006.

*****************************

Market timing

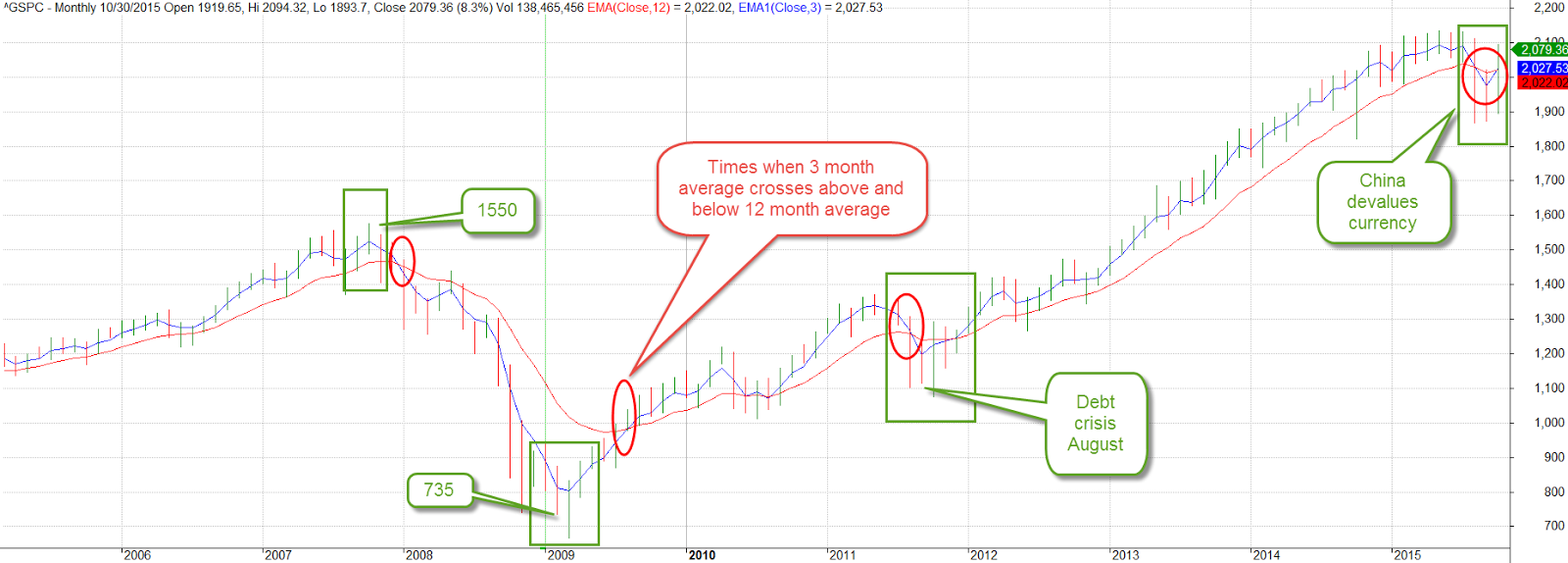

Another approach is a fairly simple market timing technique as shown in this paper “A Quantative Approach to Tactical Asset Allocation” There is no heavy math in the paper. The timing rule is simple: buy the SP500 when the monthly close is above the 10 month moving average; sell when the monthly close is below the 10 month average. Using this system, an investor would have sold an ETF like SPY on the first trading day of September this year because August’s close was below the ten month average. After the index rebounded in October and closed above the 10 month average, an investor would have bought back in on the first trading day in November. The average “turnaround,” a buy and a sell signal, is less than one a year. These short term swings are sometimes called “whipsaws,” where an investor loses several percent by selling after a quick downturn then buying in after prices recover quickly. The payoff is that an investor avoids the severe 50% drawdowns of 2008 and 2000.

The author of the paper performed a 112 year backtest on this system. He excluded taxes, commissions and slippage in the calculations and used the closing price on the final day of the month as his buy and sell price points. He notes some reasons for these omissions later in the paper which I found inadequate. I recommend using the opening price (ETF) or end of the day price (mutual fund) of the day following the end of the month as a practical real world backtesting strategy. Very few individual investors can buy or sell at the closing price and there can be a lot of price movement, or slippage, in the final trading minutes before the close.

Commissions can be estimated at some small percentage. To exclude commissions is to estimate them at 0% and present an investor with unrealistic returns, a common backtesting fault of many trading or allocation systems. The same can be said for taxes. Even if the guesstimate is a mere 1%, it is better than the 0% effective estimate of tax costs when excluded from the backtest.

The difference in annual real, or inflation-adjusted, return between this timing model and “buy and hold” is 4/100ths of 1% per year (p. 23) Because the timing model avoids the severe portfolio drawdowns of a buy and hold stratgegy (p. 28), that tiny difference translates into a difference in compounded return that is less than 1% which produces a huge 250%+ difference in portfolio balances at the end of the 112 year testing period. None of us will be investing for that long a period but it does illustrate the effect of small incremental differences.

The author then combines an allocation model with the timing model using five global asset classes: US stocks, foreign stocks, bonds, real estate and commodities, assigning 20% of the portfolio to each class. He backtested this allocation with the same timing strategy vs a buy and hold strategy (p. 30-31). The advantages of the timing strategy are apparent during severe downturns as in 1973, 2000 and 2008. A buy and hold strategy took eight years after 1973 to recover and catch up to the timing strategy. The buy and hold strategy never caught up to the timing strategy after the 2000-2003 downturn in the market. In 2008, it fell even further behind, highlighting the superiority of the timing strategy.

Returns are important, of course, but volatility and drawdown are especially critical for older investors who do not have as many years to recover. From 1973 – 2012, the timing model has only one losing year – 2008 – and the loss for the entire portfolio was a mere 6/10ths of a percent (p. 32).

*****************************

October jobs report

A few weeks ago I linked to an article on Reagan’s former budget director David Stockman. On his web site, he presented a sobering and thorough analysis of the October jobs report.

Stockman breaks down the numbers into “breadwinner” higher paying jobs and the relatively lower paying leisure and hospitality jobs that account for too much of the jub creation in the past fifteen years. Goods producing jobs – those in manufacturing, construction, mining and timber – are still far below 2000 levels.

“massive money printing and 83 months running of ZIRP [zero interest rate policy of the Federal Reserve] have done nothing for the goods producing economy or breadwinner jobs generally.”

*****************************

Obama’s numbers

A president has far less effect on the economy than the political rhetoric would have one believe. Despite that fact, each President is judged on his “numbers” as though he were a dictator, a one man show. With one year to go in his second term, here are the latest numbahs from the reputable FactCheck.