July 30, 2017

Gresham’s law states that an overvalued form of money will drive out an undervalued form of money. Let’s say that both gold and silver are accepted as money and the government fixes a ratio of 1:20 between the two metals. One ounce of gold thus equals twenty ounces of silver. Let’s say that people and businesses hold ten times as much silver as gold. The exchange ratio that the government has set is higher than the ratio of the stores of the two metals. Gold is overvalued. Gresham’s law states that people will start using gold as an exchange medium to the extent that eventually silver will be driven out of circulation.

I wanted to explore this concept and substitute two things that are not currencies or commodities: liquidity and debt. Liquidity is today’s money. Debt is tomorrow’s money. Today’s money is stable and available. Tomorrow’s money is not. As soon as money is loaned, it can’t be readily converted to cash. It’s future money.

Gresham’s law is about people’s preferences and the value of money. When millions of individual circumstances are added up, a preference for liquidity or debt emerges. When tomorrow’s money is overvalued, people use it, and drive down the use of present money. “Don’t save up to buy what you want. Buy it now with future money. Here I’ve got some,” say businesses and banks.

Let’s look at two representations of present and future money. M2 is a broad measure of the money supply that includes cash, checking and savings accounts, as well as money market accounts and CDs that can be quickly converted to cash. Future money is the amount of business and household debt.

During recessions (gray areas in the chart below), M2, the numerator in the ratio, goes up and debt goes down. Economists call this a greater preference for liquidity. Banks are more reluctant to lend money, which tightens credit and restrains the growth of debt. People charge less and stick more money in checking and savings. Businesses don’t borrow to expand their operations and keep more cash on hand to pay present obligations.

In the chart below, I chart the ratio of the yearly change in today’s money, or what the Federal Reserve calls M2 money, and tomorrow’s money, the amount of business and consumer debt.

In the recessions of the 1970s and 1980s, the graph shows what I would expect. There was a greater preference for liquidity and the ratio of present to future money rose above 1, a clear sign that people and businesses were worried about the future. As the recessions ended, the ratio declined as debt, the denominator in the fraction, grew at a faster rate than M2 money, the numerator. The recessions of the early 1990s and early 2000s were fairly mild in comparison and the uptick in a preference for liquidity was mild.

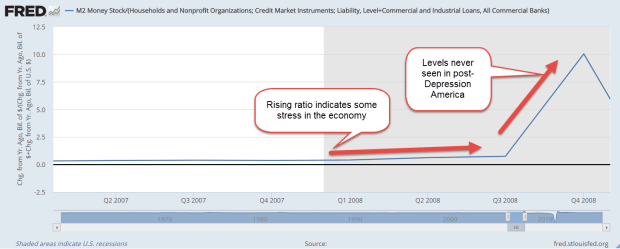

The chart ends in 2007, just before the recession and financial crisis. Let’s now turn to that period. During the early part of 2008, the ratio began to climb to 1, indicating that people and businesses were preferring liquidity over debt. During the first six months of 2008, 700,000 jobs had been lost but this was only 1/2% of the workforce. Almost 300,000 of those lost jobs were in construction, which had become overheated by the building of so many homes. Retail sales growth had gone flat but was probably just a pause in the normal course of the business and credit cycle. Not to worry.

Then a funny thing happened to the economic engine of the country, something that had never happened before in post-WW2 America. The ratio spiked upward, registering nosebleed readings.

The preference for present money continued upward but the change in debt, the bottom number in the ratio, plunged downward and this drove the ratio higher. The Federal Reserve began buying some of this debt until it held about $2 trillion.

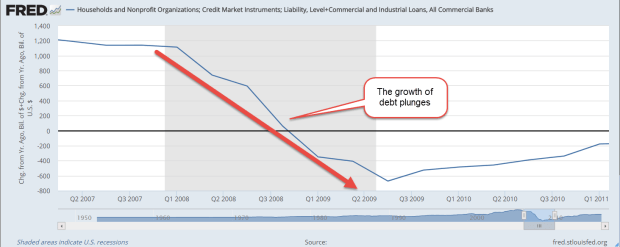

As the change in debt turned negative, the ratio turned negative, a post Depression first. Month after month, old debts soured. People and businesses shunned new debt. People who were saving more of today’s money were being offset by those who had to tap their savings accounts to make up for lost income. Toward the end of 2008, the economy lost as many jobs each month as it lost in total for the first six months of 2008. Retail sales dropped a few percent each month.

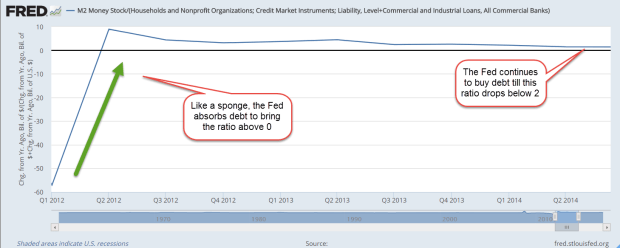

Like a car whose brakes have failed, the ratio continued its downward slide. In a program called Quantitative Easing (QE_, the Federal Reserve began buying more debt in an effort to get this ratio into the positive zone.

By the middle of 2012, the ratio broke into the positive zone as debt stopped contracting. The preference for liquidity was strikingly high, going up above 8, more than three times higher than the 2.5 level of the 1980s recession.

The Federal Reserve continued to buy debt as the economy staggered to its feet. In 2013, the stock market finally surpassed its inflation adjusted value at the start of the recession. In the early part of 2014, the ratio of liquidity to debt, of present money to future money, finally fell below 2. At mid-2014, the Fed had accumulated $4.5 trillion in debt, $3.7 trillion of which had been added during the financial crisis. After 6-1/2 years, the number of people employed finally rose above its pre-recession level. The Fed ended its debt buying program.

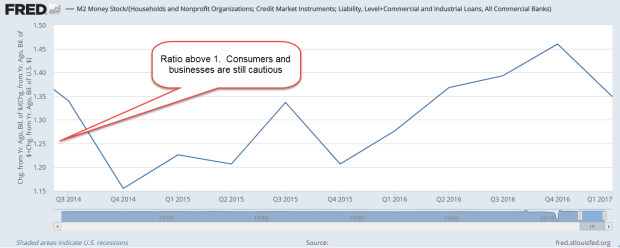

So where do we stand today? The stock market and house prices continue to make new highs but the current reading of this ratio show that people continue to prefer today’s money over tomorrow’s money.

In short, the economy is still healing. During the expanding economy of the 1960s, the ratio was a bit over 1 for half the decade. People who had grown up during the Depression were understandably a bit cautious. However, both present and future money grew at a steady rate during the 1960s. Today’s households and businesses have been scarred by the financial crisis and are cautious. Into this cautious confidence, the Fed has a lot of debt to unload. It must maintain a balance between money preferences as it feeds the debt it bought during the crisis back into the economy.